Explore why central bank digital currencies (CBDCs) may reduce—but not fully replace—cash in the next five years. Learn the drivers, risks, global examples, and what it means for the future of money in the U.S.

Will central bank digital currencies (CBDCs) replace physical cash in the next five years? This is one of the most urgent questions in finance, technology, and public policy today. As governments around the world race to modernize their payment systems, citizens worry about privacy, banks fear disruption, and businesses prepare for massive shifts in how money works.

While CBDCs promise efficiency, inclusion, and innovation, they also raise deep concerns about surveillance, stability, and adoption. Looking at global experiments, U.S. policy, and human behavior, the evidence suggests one conclusion: CBDCs will reduce cash usage significantly, but they will not replace it entirely in the next five years.

This article dives into the core issues, global lessons, scenarios, and real-life examples that show why the future is hybrid, not cashless.

What Exactly Are CBDCs, and How Are They Different from Cash?

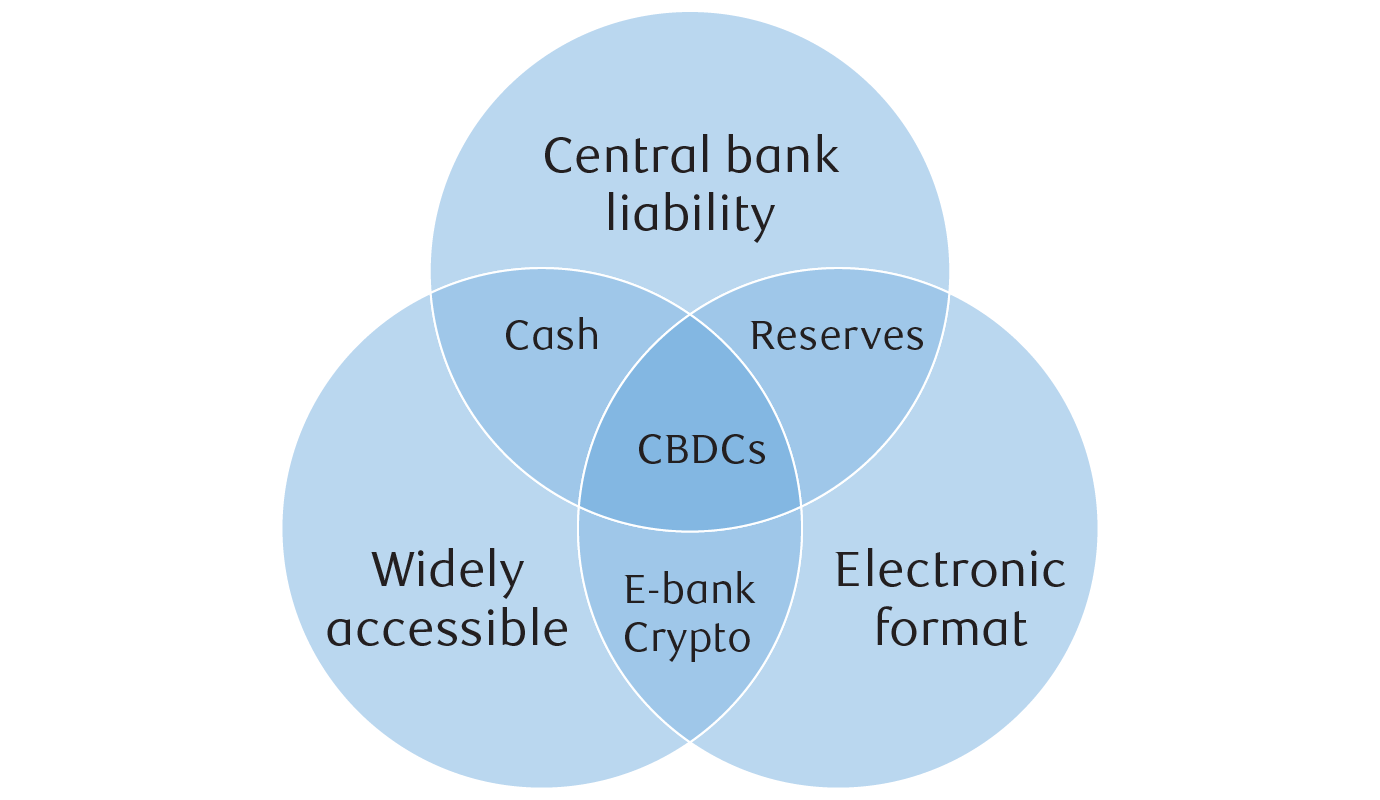

To understand the debate, it’s important to distinguish between traditional cash and a central bank digital currency.

- Cash is physical money—coins and notes—issued by a central authority (like the Federal Reserve in the U.S.) and accepted as legal tender. It works offline, provides anonymity, and requires little infrastructure.

- CBDCs are digital versions of money issued directly by central banks. They exist in electronic wallets, can be programmed with rules, and may be either retail (for the public) or wholesale (for banks and large institutions).

The differences matter:

| Feature | Cash | CBDC |

|---|---|---|

| Tangibility | Physical | Digital |

| Privacy | High (anonymous use possible) | Varies; often low |

| Infrastructure | Minimal | Requires internet + devices |

| Traceability | Hard to trace | Fully trackable |

| Resilience | Works offline | Needs power + connectivity |

| Cost | Printing, distribution | Cybersecurity, systems, ID checks |

This contrast explains why many governments push CBDCs (modernization, efficiency) while citizens defend cash (privacy, resilience).

Global Trends: Where Are CBDCs Already Happening?

The world is not waiting. According to the Bank for International Settlements, 94% of central banks are researching CBDCs, and 34% expect to issue one in 3–5 years (BIS report).

Some examples:

- China: Piloting the digital yuan in dozens of cities, testing consumer payments, government subsidies, and transport systems. Adoption is growing but cash still dominates in many places.

- Bahamas: Issued the Sand Dollar, one of the first fully launched retail CBDCs. Adoption faced hurdles in merchant readiness and public awareness.

- Nigeria: Launched the eNaira, but uptake was initially slow due to mistrust and lack of clear advantages over existing mobile money.

- Europe: The European Central Bank is exploring a digital euro, with public consultations focused on privacy.

- United States: The Federal Reserve has published discussion papers but has not committed to issuing a digital dollar. Political opposition and privacy concerns make progress cautious.

These experiments reveal an important truth: launching a CBDC is easier than achieving mass adoption. Cultural habits, trust, and infrastructure matter as much as technology.

Why Governments Are Pushing CBDCs

Governments and central banks are not exploring CBDCs for fun—they see real needs and strategic goals.

- Faster, cheaper payments: Cross-border transfers are slow and costly. Domestic real-time payments often depend on private companies. CBDCs could streamline both.

- Financial inclusion: Millions remain unbanked or underbanked. A CBDC wallet could give them direct access to central bank money, bypassing costly intermediaries.

- Monetary sovereignty: Private stablecoins (like USDT, USDC) and cryptocurrencies threaten to fragment monetary control. A CBDC keeps the central bank in charge.

- Reduce costs of cash: Printing, distributing, and securing physical cash is expensive. A digital currency can cut costs in the long run.

- Combat illicit activity: With traceability, CBDCs could reduce tax evasion, corruption, and counterfeiting.

- Respond to digital habits: Younger generations already live cashless lives—CBDCs aim to provide a state-backed alternative to Venmo, PayPal, or crypto wallets.

On paper, the case is strong. But the downsides are just as powerful.

The Challenges and Risks of CBDCs

Despite enthusiasm, CBDCs face steep obstacles. These risks explain why total replacement of cash is unrealistic in five years.

- Privacy and surveillance fears: Many Americans reject the idea of government monitoring their purchases. A Cato Institute survey found only 16% support for a U.S. CBDC (Cato survey).

- Bank disintermediation: If citizens hold CBDCs directly, banks lose deposits, weakening lending capacity and financial stability.

- Cybersecurity risks: A hack on a national digital currency could paralyze economies.

- Infrastructure gaps: Rural communities, elderly populations, and people without reliable internet may be excluded.

- Legal and political barriers: In the U.S., legislation and bipartisan consensus would be required—currently a tall order.

- Trust deficit: People still prefer the tangibility and anonymity of cash. Transition requires cultural change, not just new apps.

Without solving these, adoption will stall.

The U.S. Context: Why a Digital Dollar Is Moving Slowly

Unlike some nations racing ahead, the U.S. remains cautious.

- Federal Reserve stance: The Fed is exploring options but insists it won’t move without clear public and congressional support (Fed paper).

- Treasury perspective: The U.S. Treasury’s “Future of Money and Payments” report emphasized research, infrastructure, and regulation before launch (Treasury report).

- Political climate: CBDCs are polarizing. Some politicians frame them as tools of government overreach.

- Consumer behavior: Americans use credit cards, PayPal, Venmo, and Apple Pay daily. Many don’t feel a CBDC would add value compared to existing options.

- Cash culture: While cash use is declining, it remains critical in emergencies, small businesses, and among the unbanked.

In short, the U.S. is not leading the CBDC race.

Will CBDCs Replace or Just Reduce Cash?

The evidence points toward reduction, not elimination.

- Cash will remain important for emergencies, resilience, and privacy-conscious users.

- CBDCs could dominate small everyday transactions in urban, tech-savvy populations.

- Rural, elderly, and low-income groups will lag in adoption.

- Hybrid systems—where cash, CBDCs, bank money, and private stablecoins coexist—are the most likely outcome.

By 2029, cash may account for far fewer point-of-sale transactions, but eliminating it altogether would require mandates and public buy-in that simply do not exist yet.

Possible Scenarios for the Next 5 Years

Scenario 1: Fast Adoption (25–40% chance)

CBDC launched by 2027, designed with privacy tiers and strong merchant incentives. Urban populations go largely cashless; cash usage drops by half.

Scenario 2: Moderate Change (40–60% chance)

CBDC pilots roll out but with caps and restrictions. Adoption grows slowly, coexisting with cash and cards. By 2029, CBDC is common but cash still widely used.

Scenario 3: Minimal Progress (20–30% chance)

Legal hurdles, public resistance, or tech flaws delay CBDC. Cash continues to decline gradually, but no big disruption occurs.

Most analysts favor Scenario 2 as the most realistic.

Practical Advice for Stakeholders

For Policymakers

- Build trust with privacy-friendly designs.

- Launch education campaigns to demystify CBDCs.

- Ensure offline capability and cybersecurity resilience.

- Regulate fairly to avoid excluding vulnerable groups.

For Businesses

- Upgrade payment systems to be CBDC-ready.

- Plan for dual acceptance of cash and digital money.

- Market CBDC acceptance as a sign of innovation and trust.

For Consumers

- Stay informed about your rights and risks.

- Keep some cash for emergencies.

- Strengthen digital literacy and cybersecurity practices.

- Follow public debates—your voice matters in shaping CBDCs.

Frequently Asked Questions (FAQs)

(Use Rank Math’s FAQ schema for maximum SEO visibility.)

Q1: What percentage of Americans support CBDCs?

Only about 16%, according to Cato Institute polling. Support drops further when surveillance is mentioned.

Q2: Could CBDCs fully replace cash by 2029?

No. Cash will still play a role in emergencies, small businesses, and among resistant groups.

Q3: What is the biggest fear around CBDCs?

Loss of privacy and government surveillance top the list.

Q4: How can CBDCs be designed to protect privacy?

Through transaction limits, anonymity tiers, and strong legal protections.

Q5: How would banks be affected?

Banks risk losing deposits if citizens hold CBDCs directly. This could hurt lending capacity.

Q6: What have real-world pilots taught us?

Adoption is slow without clear consumer benefits. China’s digital yuan and Bahamas’ Sand Dollar prove it takes time.

Q7: Will CBDCs eliminate cash for small purchases?

They may dominate in cafes and shops, but total elimination in five years is unlikely.

Q8: Are CBDCs vulnerable to cyberattacks?

Yes—strong cybersecurity and redundancy are essential.

Q9: What are the costs of transition?

High: infrastructure, identity verification, education, and merchant adaptation.

Q10: How should small businesses prepare?

Stay flexible, keep accepting cash, but ensure systems can process CBDCs when they arrive.

Real-Life Examples to Watch

- Bahamas: Early rollout of Sand Dollar shows digital doesn’t kill cash.

- China: Even with government support, the digital yuan hasn’t replaced notes.

- U.S. local level: After hurricanes, people relied on cash when digital systems failed. This reinforces why cash remains critical.

Conclusion

The debate is not about if CBDCs will reshape money, but how far and how fast. Over the next five years, cash will decline further, especially for everyday purchases, but it will not vanish. Privacy concerns, infrastructure gaps, and trust barriers guarantee that cash will survive—at least for another decade. The future is hybrid, where cash, CBDCs, cards, and crypto coexist.