Are Millennials finally buying homes in 2025 or still renting? Discover surprising data, real-life stories, affordability challenges, FAQs, and expert advice on Millennial homeownership in the U.S.

Millennials, born between 1981 and 1996, are now between 26 and 44 years old. This is the life stage when earlier generations typically bought their first homes, settled down, or at least left behind long-term renting. But for Millennials, the path has been anything but typical.

So, the big question: Are Millennials finally buying homes, or are they still stuck renting?

The truth is complicated. Millions of Millennials are entering the housing market, often later than previous generations, but millions more are still renting because of affordability barriers, student debt, and lifestyle choices. In this blog, we’ll explore the data, the emotional reality, and the strategies Millennials are using to turn renting into ownership.

This isn’t just numbers. It’s about real lives, hard choices, and the American Dream redefined.

Why This Question Matters in 2025

Housing is the single largest financial decision most people make. For Millennials, it has become a generational identity marker. Articles, social media memes, and TikToks often joke about Millennials being “permanent renters.” But behind the jokes is a serious debate about affordability, inequality, and what it means to build wealth in today’s America.

The decision to rent or buy isn’t just financial—it’s emotional, cultural, and deeply tied to how people envision their futures.

The Data: Are Millennials Buying or Renting?

Before diving into the “why,” let’s look at the key statistics that reveal where things stand.

| Statistic | Insight (2024–2025) | Source |

|---|---|---|

| Millennial share of buyers | 29% of all U.S. homebuyers are Millennials | Fool.com |

| Younger Millennials buying for first time | 71% of Millennials aged 26–34 are first-time buyers | NAR |

| Older Millennials (35–44) as first-timers | 36% are buying for the first time | NAR |

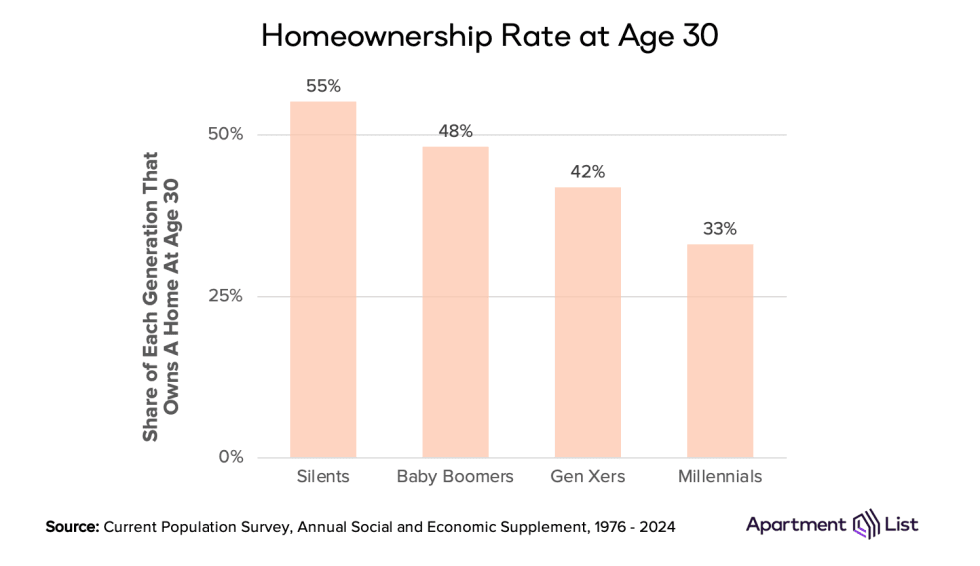

| Overall Millennial homeownership rate | ≈ 55% (still below previous generations at same age) | Investopedia |

| Millennial sentiment | 80% say homeownership is not affordable for the average American, yet 89% still see it as part of the “American Dream” | Clever Offers |

| Best metro for Millennial buyers | Raleigh-Cary, NC where 4.5% of Millennials bought with conventional mortgages in 2024 | SmartAsset |

Takeaway: Millennials are buying, but later and less than Boomers or Gen X did at the same ages. Renting is still the majority experience, especially in expensive metros.

Why Many Millennials Are Still Renting

If homeownership is so desirable, why are millions of Millennials still renting?

1. High Housing Prices and Rising Mortgage Rates

Millennials are entering the market at one of the most expensive times in U.S. housing history. Even though home prices cooled slightly in 2023–24, they remain historically high compared to income growth. Mortgage rates hovering near 6–7% in 2025 make monthly payments even harder to manage.

2. Down Payment Challenges

A 20% down payment on a $400,000 home is $80,000—an almost impossible savings target for many Millennials balancing rent, debt, and living costs. While FHA loans and first-time buyer programs lower the bar, upfront costs remain a massive hurdle.

3. Student Loan and Consumer Debt

Student loan debt affects both savings and mortgage qualification. A $400 monthly student loan payment can drastically lower the mortgage amount a Millennial qualifies for. Many lenders use debt-to-income ratios that disqualify buyers carrying large loan burdens.

4. Limited Housing Supply

Even motivated buyers struggle because there simply aren’t enough homes available. Baby Boomers and Gen X homeowners, who locked in ultra-low mortgage rates in 2020–21, are reluctant to sell, keeping supply tight.

5. Lifestyle and Flexibility

Not all renting is forced. Many Millennials appreciate the flexibility of renting—proximity to downtowns, shorter leases, access to amenities, and freedom to relocate for jobs.

Bottom line: Renting isn’t just about affordability—it’s also about life choices.

Real-Life Stories of Millennial Homebuyers

To make this real, let’s look at three Millennial journeys:

- Aisha, 32, Austin, TX

Aisha delayed buying for years due to $45,000 in student loans. By cutting costs, living with a roommate, and receiving a small family gift, she finally bought a modest fixer-upper in East Austin in 2024. It wasn’t her “dream house,” but it was a first step toward equity. - David & Maria, 38, San Jose, CA

Tech professionals with strong incomes but frustrated by Silicon Valley prices, they purchased a home in Tracy, California—doubling their commute but reducing costs by 40%. For them, ownership was worth the sacrifice in location. - Jamal, 29, Detroit Metro

Jamal used Michigan’s first-time buyer program for down payment assistance. With stable employment and minimal debt, he bought a $180,000 starter home in 2023. For him, homeownership became achievable through state programs.

Where Millennials Are Buying: Metro Trends

Some regions stand out as Millennial buying hubs:

- Raleigh-Cary, NC: Highest concentration of Millennial buyers at 4.5% of the local Millennial population.

- Houston, TX: Over 60,000 Millennial mortgages issued in 2024—the most in raw numbers.

- Midwestern & Southern cities: Affordable prices and job growth attract Millennial buyers seeking value.

Meanwhile, metros like San Francisco, Los Angeles, and New York City remain out of reach for most Millennials.

Top 10 FAQs About Millennial Homeownership

Structured for FAQ Schema in WordPress (Rank Math).

1. How many Millennials own homes in 2025?

Less than 55% of Millennials own homes as of 2025, compared to 70%+ of Boomers at the same age. Progress has been slow due to affordability issues.

2. Why are Millennials buying homes later?

Debt, high housing prices, career instability during the Great Recession, and lifestyle preferences delayed ownership. Many Millennials are now buying in their 30s and 40s.

3. What percent of Millennials are first-time buyers?

Around 71% of younger Millennials (26–34) are first-time buyers. For older Millennials (35–44), it drops to 36%.

4. Is renting smarter than buying in 2025?

In some markets, yes. Renting can cost less monthly, provide flexibility, and reduce financial risk. Buying makes sense for long-term stability, equity, and protection against rent hikes.

5. How does student debt impact Millennial homeownership?

Student loans reduce savings and harm debt-to-income ratios, making mortgages harder to qualify for. Many Millennials delay buying until loans are paid down.

6. Which U.S. cities are best for Millennial buyers in 2025?

- Raleigh-Cary, NC

- Houston, TX

- Midwestern metros like Columbus, OH and Indianapolis, IN

Affordable metros with job growth tend to attract Millennial buyers.

7. Are Millennials giving up on homeownership?

No. Surveys show nearly 89% of Millennials still see homeownership as part of the American Dream, even if they feel it’s unaffordable today.

8. How are Millennials saving for down payments?

- Living with parents longer

- Side hustles and gig work

- State assistance programs

- Delaying family formation to save more

9. Do Millennials prefer city apartments or suburban homes?

Preferences are split. Many younger Millennials prefer renting in cities for lifestyle, while older Millennials with children lean toward suburban homes.

10. Will Millennials ever reach Boomer-level ownership rates?

Unlikely, due to systemic affordability challenges. However, ownership rates are expected to rise slowly as Millennials age and incomes grow.

Strategies Millennials Use to Buy Despite Challenges

- Moving to affordable metros

- Buying smaller homes or fixer-uppers

- Leveraging first-time buyer programs (FHA, USDA, VA loans)

- Partnering with family for down payments

- Taking on roommates after purchase to offset mortgage costs

Policy & Market Shifts That Could Help

- Zoning reform: Allowing more duplexes, townhomes, and accessory dwelling units.

- Down payment assistance: Expanding federal and state programs.

- Mortgage innovation: Flexible terms, lower down payment requirements.

- Housing supply growth: Incentives for builders to create affordable housing.

Future Outlook: What’s Next for Millennials

Looking ahead, several factors will shape Millennial homeownership:

- Mortgage rates: If they drop back to 4–5%, affordability will improve.

- Remote work: May continue to shift Millennials toward affordable regions.

- Wealth transfer: As Boomers age, inheritances may help Millennials buy.

- Rental inflation: Rising rents could push more Millennials into buying despite high prices.

Conclusion

So—are Millennials finally buying homes or still renting?

The answer is both. Millions of Millennials are becoming homeowners, especially in affordable metros and with the help of first-time buyer programs. But millions more are still renting—some by choice, many by necessity.

Homeownership is not dead for Millennials—it’s just delayed, redefined, and more complex than ever before.