Summary

Strategic withdrawal planning allows retirees to control how much taxable income they generate each year. By coordinating withdrawals from taxable, tax-deferred, and Roth accounts, retirees may keep income within lower tax brackets, reduce lifetime taxes, and avoid costly triggers such as higher Medicare premiums. Thoughtful withdrawal sequencing can turn retirement savings into a more predictable and tax-efficient income strategy.

Retirement planning does not end when paychecks stop. In many ways, the tax strategy that follows retirement can be just as important as the decades spent saving. Many retirees discover that withdrawing money without a plan may push them into higher tax brackets, increase Medicare premiums, and accelerate the taxation of Social Security benefits.

Strategic withdrawals—carefully choosing which accounts to draw from and when—can help retirees manage taxable income year by year. Done well, this approach allows retirees to preserve more of their savings while maintaining financial flexibility throughout retirement.

Understanding how withdrawal strategy interacts with the U.S. tax system is therefore one of the most practical steps retirees can take to improve long-term financial outcomes.

Why Taxes Still Matter After Retirement

Many people assume taxes will decline significantly after they stop working. While income may fall, retirement itself introduces several taxable income sources:

- Traditional IRA withdrawals

- 401(k) distributions

- Pension income

- Social Security benefits (partially taxable)

- Investment income such as dividends and capital gains

According to the Internal Revenue Service, withdrawals from traditional retirement accounts are generally taxed as ordinary income. This means a large withdrawal in a single year may push retirees into a higher tax bracket.

For example, the 2024 federal tax brackets for married couples filing jointly show that taxable income exceeding roughly $94,000 moves into the 22% bracket. If retirees withdraw more than needed in one year, they may unintentionally increase their tax burden.

Strategic withdrawal planning focuses on smoothing income across years rather than allowing taxes to spike unpredictably.

The Three Types of Retirement Accounts

Most retirees hold savings across three tax categories. Each category has different tax consequences when money is withdrawn.

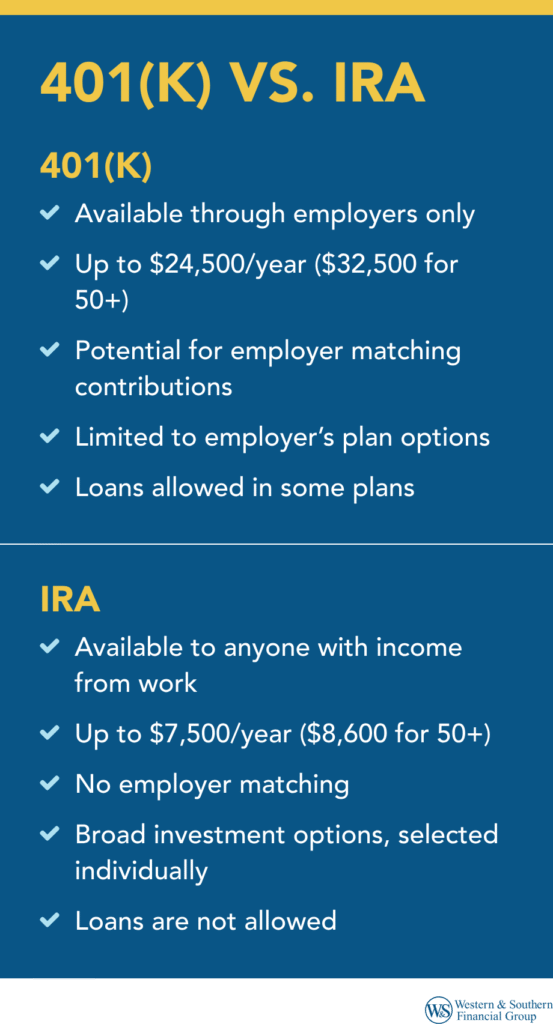

1. Tax-Deferred Accounts

Examples include:

- Traditional IRAs

- 401(k) plans

- 403(b) plans

Contributions were generally made pre-tax, and withdrawals are taxed as ordinary income.

Once retirees reach age 73, Required Minimum Distributions (RMDs) force withdrawals from these accounts, whether the money is needed or not.

2. Taxable Brokerage Accounts

These accounts are funded with after-tax dollars. Taxes apply only to:

- Capital gains when assets are sold

- Dividends or interest earned

Long-term capital gains may be taxed at lower rates than ordinary income.

3. Roth Accounts

Examples include:

- Roth IRAs

- Roth 401(k)s

Qualified withdrawals are generally tax-free. Importantly, Roth IRAs do not require minimum distributions during the owner’s lifetime.

Strategic withdrawals involve coordinating all three account types to manage taxable income each year.

How Withdrawals Can Push Retirees Into Higher Tax Brackets

Consider a retired couple with the following income sources:

- $40,000 in Social Security

- $25,000 from a pension

- $20,000 withdrawn from a traditional IRA

Their taxable income may already approach $85,000 once deductions are applied.

If they withdraw an additional $40,000 for a home renovation from their IRA, their taxable income may jump well into the next tax bracket.

This can trigger several consequences:

- Higher marginal tax rates

- Greater taxation of Social Security benefits

- Increased Medicare premiums through **Medicare IRMAA surcharges

Because these thresholds are based on income, careful withdrawal planning may help retirees avoid crossing them unnecessarily.

The Concept of “Filling the Tax Bracket”

One of the most practical retirement tax strategies is known as tax bracket filling.

Instead of waiting until RMDs force large withdrawals later in life, retirees may choose to withdraw just enough each year to stay within a chosen tax bracket.

For example:

- A retiree may target the top of the 12% tax bracket.

- Withdrawals are adjusted annually to remain within that range.

This strategy spreads taxable income across many years rather than concentrating it later when RMDs begin.

It can also reduce the size of tax-deferred accounts, which may lower required withdrawals in the future.

Strategic Withdrawal Order: A Common Approach

Many financial planners suggest withdrawing assets in a sequence that balances tax efficiency with flexibility.

A common order may look like this:

- Taxable brokerage accounts first

- Tax-deferred retirement accounts next

- Roth accounts last

This order works because taxable accounts often produce lower tax rates on capital gains, while Roth accounts grow tax-free.

However, this is not a universal rule. In some cases, early withdrawals from traditional accounts—especially before RMDs begin—may help manage future taxes.

Real-World Example: Managing Income in Early Retirement

Consider a retiree named Susan who stops working at age 62 but delays Social Security until age 70.

During this eight-year window, Susan has unusually low taxable income. She uses this period to withdraw moderate amounts from her traditional IRA each year.

This accomplishes several goals:

- She fills lower tax brackets while income is minimal

- Her IRA balance shrinks before RMDs begin

- Future taxable withdrawals are reduced

When Social Security begins at age 70, Susan’s tax-deferred balance is smaller, helping her avoid higher tax brackets later.

This type of “gap year” strategy is commonly recommended by retirement tax planners.

Strategic Roth Conversions

Another common approach involves converting portions of a traditional IRA into a Roth IRA.

A Roth conversion means paying tax now in exchange for tax-free withdrawals later.

Retirees sometimes convert funds when they are temporarily in lower tax brackets.

Benefits may include:

- Lower lifetime tax exposure

- Reduced future RMDs

- Tax-free income flexibility later in retirement

However, conversions must be carefully planned because the converted amount is taxable in the year it occurs.

Avoiding Medicare Premium Surprises

Many retirees are surprised to learn that Medicare premiums depend on income levels.

Higher income retirees may pay surcharges known as Income-Related Monthly Adjustment Amounts (IRMAA).

The Social Security Administration determines IRMAA using income from two years prior.

Large withdrawals from tax-deferred accounts can push retirees above these thresholds.

Strategic withdrawals may help retirees stay below key income levels and avoid these additional costs.

Coordinating Social Security and Withdrawals

The timing of **Social Security benefits also affects taxes.

Up to 85% of Social Security benefits may become taxable depending on combined income.

Retirees who delay Social Security often gain a valuable planning window where they can:

- Withdraw from retirement accounts at lower tax rates

- Perform Roth conversions

- Reduce future taxable balances

This coordination is often one of the most impactful tax strategies in retirement planning.

Practical Withdrawal Guidelines Retirees Often Use

Experienced retirement planners frequently emphasize a few practical guidelines:

- Review income annually before taking withdrawals

- Avoid large one-time withdrawals from tax-deferred accounts

- Monitor Medicare IRMAA thresholds

- Consider partial Roth conversions during low-income years

- Use taxable accounts strategically for large purchases

These decisions may appear small year-to-year, but over decades they can significantly influence total taxes paid.

Frequently Asked Questions

1. What is a strategic withdrawal strategy in retirement?

A strategic withdrawal strategy involves choosing which retirement accounts to withdraw from each year to minimize taxes and maintain a predictable income stream.

2. Why are traditional IRA withdrawals taxable?

Traditional IRA contributions are often made with pre-tax dollars, meaning taxes are deferred until the money is withdrawn.

3. What age do required minimum distributions begin?

Under current U.S. law, RMDs generally begin at age 73 for most retirement accounts.

4. Are Roth IRA withdrawals always tax-free?

Qualified withdrawals are typically tax-free if the account has been open at least five years and the owner is over age 59½.

5. Can withdrawals affect Medicare premiums?

Yes. Higher taxable income can trigger IRMAA surcharges, increasing Medicare premiums.

6. Is it better to withdraw from taxable accounts first?

Often yes, but the best strategy depends on the retiree’s income, tax bracket, and future RMD exposure.

7. What are retirement “gap years”?

Gap years are the period between retirement and the start of Social Security or RMDs when income may be temporarily lower.

8. Do strategic withdrawals reduce lifetime taxes?

They may help reduce lifetime taxes by spreading taxable income across multiple years and avoiding higher brackets.

9. How often should retirees review withdrawal strategies?

Many financial planners recommend reviewing withdrawal plans annually because tax laws, income sources, and account balances change.

10. Should retirees work with a tax advisor?

Complex situations—such as large retirement accounts, Roth conversions, or estate planning—often benefit from professional tax guidance.

Designing a Retirement Income Plan That Works Year After Year

Retirement income planning is less about predicting markets and more about managing decisions over time. Strategic withdrawals allow retirees to treat their savings as a coordinated system rather than isolated accounts.

By balancing withdrawals across tax-deferred, taxable, and Roth accounts, retirees can smooth income, avoid sudden tax spikes, and maintain flexibility when financial needs change.

The most effective strategies typically involve regular reviews, attention to tax thresholds, and a willingness to adjust withdrawals as circumstances evolve.

Over a retirement that may last 25 to 30 years, these incremental decisions can play a meaningful role in preserving wealth and maintaining financial stability.

Key Insights for Smarter Retirement Withdrawals

- Retirement taxes often depend on withdrawal timing.

- Strategic withdrawals help control taxable income.

- Filling lower tax brackets may reduce lifetime taxes.

- Early retirement years create valuable planning opportunities.

- Roth conversions can improve long-term flexibility.

- Large withdrawals may trigger higher Medicare premiums.

- Annual income reviews are essential for tax efficiency.