Digital assets—such as cryptocurrencies, tokenized securities, and stablecoins—are increasingly influencing how Americans plan and manage their finances. As institutions adopt blockchain technologies and regulators clarify frameworks, investors are exploring how these assets may complement traditional portfolios. Understanding their potential role, risks, and long-term implications is becoming an important component of modern financial planning.

Introduction: A New Category in Personal Finance

For decades, financial planning in the United States centered on a familiar mix of investments: stocks, bonds, real estate, and cash equivalents. Today, a new category is steadily entering the conversation—digital assets.

Digital assets broadly include blockchain-based financial instruments such as cryptocurrencies, stablecoins, tokenized securities, and digital collectibles. These assets are created and exchanged on blockchain networks, allowing transparent, verifiable ownership and transactions.

While early conversations often focused on speculation, the discussion has shifted. Financial advisors, institutions, and policymakers are increasingly asking a different question: how might digital assets fit into responsible financial planning?

For many Americans, the answer is no longer theoretical. Retirement accounts, investment platforms, and large financial institutions are exploring ways to integrate digital assets into mainstream finance. As a result, individuals planning for long-term financial stability are beginning to evaluate how this evolving asset class fits alongside traditional investments.

What Exactly Are Digital Assets?

The term “digital assets” refers to a wide range of blockchain-based financial instruments.

Common categories include:

- Cryptocurrencies such as Bitcoin and Ethereum

- Stablecoins, which are designed to maintain a stable value relative to currencies like the U.S. dollar

- Tokenized assets, including digital representations of stocks, bonds, or real estate

- Non-fungible tokens (NFTs) representing unique digital ownership

Unlike traditional assets, these instruments operate on decentralized or distributed ledger systems. Blockchain networks record ownership and transactions in a transparent, tamper-resistant way.

Because of this structure, digital assets can support faster transactions, automated financial contracts, and new forms of ownership that were difficult to implement through conventional financial infrastructure.

Why Financial Planners Are Paying Attention

Digital assets have moved from experimental technology to a growing part of the global financial system.

Major financial institutions—including Goldman Sachs, BlackRock, and Fidelity Investments—have launched initiatives exploring tokenized funds and digital asset services. Institutional adoption has accelerated in recent years as firms explore blockchain-based financial infrastructure and new investment products.

At the same time, U.S. regulators have begun establishing frameworks around digital assets. For example, legislation supporting regulated stablecoin issuance has increased interest in blockchain-based dollar systems.

For financial planners, these developments signal something important: digital assets are becoming part of the broader financial ecosystem, not just a niche market.

Portfolio Diversification in a Changing Investment Landscape

One reason digital assets are entering financial planning discussions is diversification.

Diversification aims to reduce risk by spreading investments across asset classes that may behave differently during economic cycles.

Digital assets offer characteristics that can complement traditional investments:

- Exposure to emerging technology sectors

- Potential independence from traditional market cycles

- Global accessibility and liquidity

- Programmable financial structures through smart contracts

For example, some investors allocate a small portion of their portfolios to digital assets as a satellite allocation, while maintaining core holdings in stocks, bonds, and retirement accounts.

Financial planners often emphasize moderation. Rather than replacing traditional investments, digital assets are typically considered one component of a broader strategy.

Institutional Adoption Is Changing the Narrative

The early cryptocurrency market was largely retail-driven. Today, institutional participation is expanding rapidly.

Banks and financial firms are building blockchain infrastructure designed for regulated financial markets. One example is the Canton Network, a blockchain platform supported by organizations including Microsoft and BNP Paribas that aims to enable secure financial transactions across institutions.

In addition, blockchain-based lenders and fintech companies are attracting significant investment from major banks and asset managers.

Institutional interest matters for financial planning because it often leads to:

- Greater regulatory clarity

- Improved infrastructure and security

- More investment products available to everyday investors

As these systems mature, digital assets become easier for individuals to access through traditional financial channels.

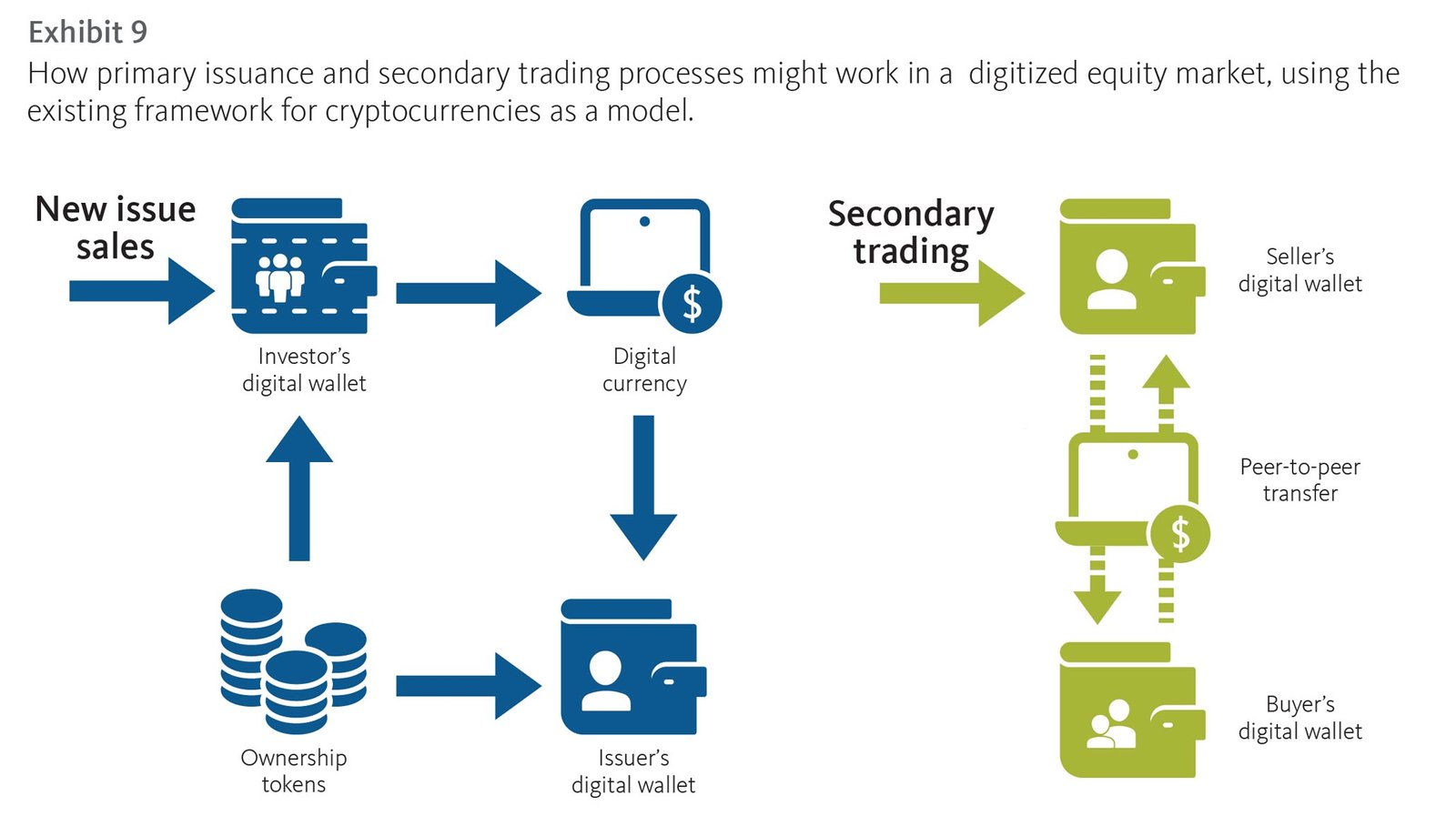

The Rise of Tokenized Assets

One of the most significant developments in digital finance is tokenization.

Tokenization converts real-world financial assets into blockchain-based digital tokens. These tokens represent ownership of underlying assets such as government bonds, money market funds, or real estate.

Several large financial institutions are already experimenting with tokenized financial products. For instance, blockchain-based tokenized Treasury funds and money market instruments are being developed to provide institutional investors with digital access to traditional assets.

Tokenization may eventually improve financial markets by:

- Increasing settlement speed

- Reducing transaction costs

- Allowing fractional ownership of large assets

- Improving transparency and auditability

For financial planners, tokenization represents a bridge between traditional finance and blockchain-based systems.

How Digital Assets Fit Into Real Financial Plans

In practice, digital assets often appear in financial plans in specific ways.

Common Approaches

Many advisors consider digital assets through strategies such as:

- Small portfolio allocations (often 1–5% depending on risk tolerance)

- Long-term holding strategies similar to venture-style investments

- Exposure through regulated funds or ETFs

- Participation in blockchain-based financial infrastructure

These approaches vary depending on an individual’s goals, age, and risk tolerance.

A Practical Example

Consider a hypothetical investor in their mid-30s planning for retirement:

- 60% diversified stock index funds

- 25% bonds and fixed income

- 10% real estate exposure

- 5% digital assets

In this scenario, digital assets represent a small but potentially high-growth component of a diversified portfolio.

Financial planners often emphasize that such allocations should be evaluated within the context of a broader financial plan.

Risks Every Investor Should Understand

Digital assets can offer opportunities, but they also introduce new risks that must be carefully considered.

Key risk factors include:

- Market volatility

- Regulatory uncertainty

- Security risks related to digital wallets and custody

- Rapid technological change

Financial professionals also emphasize the importance of secure custody solutions. Companies such as Fireblocks provide institutional-grade infrastructure designed to protect digital assets from theft and operational risk.

For individuals, the most important step is education—understanding how digital assets work before allocating capital.

Digital Assets and the Future of Financial Infrastructure

Beyond individual investments, digital assets are influencing the broader financial system.

Blockchain technology is increasingly used to modernize payments, trading, and settlement systems. Financial experts note that distributed ledger technology can improve efficiency, transparency, and global financial connectivity.

Banks are already exploring blockchain-based payment systems that allow near-instant transfers and continuous settlement.

These developments suggest that digital assets may play a role not just in investment portfolios, but in how money itself moves through the global economy.

Questions Americans Are Asking About Digital Assets

Financial planning conversations increasingly include digital assets because Americans are searching for practical answers to questions such as:

- Should digital assets be part of retirement planning?

- How much cryptocurrency exposure is considered reasonable?

- Are tokenized assets the future of investing?

- What regulations apply to digital asset investments in the U.S.?

As the financial system evolves, these questions are becoming part of mainstream financial literacy.

Frequently Asked Questions

1. Are digital assets considered investments?

Yes. Many digital assets function similarly to investment instruments, although they often operate on blockchain networks rather than traditional financial systems.

2. How much of a portfolio should include digital assets?

Financial professionals often suggest small allocations, typically a few percent of a portfolio, depending on an investor’s risk tolerance.

3. Are digital assets regulated in the United States?

Regulation is evolving. Agencies such as the U.S. Securities and Exchange Commission and Commodity Futures Trading Commission oversee aspects of digital asset markets.

4. Are cryptocurrencies the same as digital assets?

Cryptocurrencies are a subset of digital assets. The category also includes tokenized securities, stablecoins, and other blockchain-based financial instruments.

5. Can digital assets be part of retirement planning?

Some retirement accounts and investment funds now offer limited exposure to digital assets, though careful planning is recommended.

6. What is tokenization in finance?

Tokenization converts traditional financial assets into blockchain-based digital tokens representing ownership.

7. Are digital assets risky?

Yes. Like any emerging technology sector, digital assets can experience significant price volatility and regulatory uncertainty.

8. How do investors store digital assets?

They are typically stored in digital wallets or through custodial services offered by financial institutions.

9. Are stablecoins safer than cryptocurrencies?

Stablecoins aim to maintain a stable value, often tied to the U.S. dollar, but they still carry regulatory and operational risks.

10. Why are banks exploring digital assets?

Banks see potential benefits in faster settlement, reduced costs, and improved transparency in financial transactions.

The Strategic Role of Digital Assets in Tomorrow’s Financial Plans

Digital assets are no longer confined to technology forums or niche investment communities. They are increasingly part of serious conversations among financial advisors, banks, and policymakers.

For individuals building long-term financial strategies, the most important approach is thoughtful integration. Digital assets may offer diversification and exposure to emerging financial technologies, but they work best when incorporated into a well-balanced plan grounded in traditional financial principles.

As the infrastructure surrounding blockchain finance matures, digital assets are likely to become one of several tools investors use to build resilient, forward-looking financial portfolios.

Key Insights at a Glance

- Digital assets include cryptocurrencies, stablecoins, and tokenized financial instruments.

- Institutional adoption is accelerating across banks and asset managers.

- Tokenization may reshape how traditional assets are issued and traded.

- Digital assets are typically considered a small allocation within diversified portfolios.

- Regulatory frameworks in the U.S. are evolving to support responsible innovation.

- Financial education remains essential before investing in blockchain-based assets.