Summary

Six-figure earners face unique tax challenges as income rises and deductions begin to phase out. Strategic tax planning can reduce liabilities, increase long-term wealth, and avoid costly mistakes. This guide explores practical tax strategies used by high-income professionals in the U.S., including retirement optimization, tax-efficient investing, income timing, and advanced deductions.

Why Tax Planning Becomes Critical After Crossing Six Figures

Reaching a six-figure income is a major milestone for many professionals in the United States. However, the financial benefits of higher earnings are often partially offset by rising tax obligations.

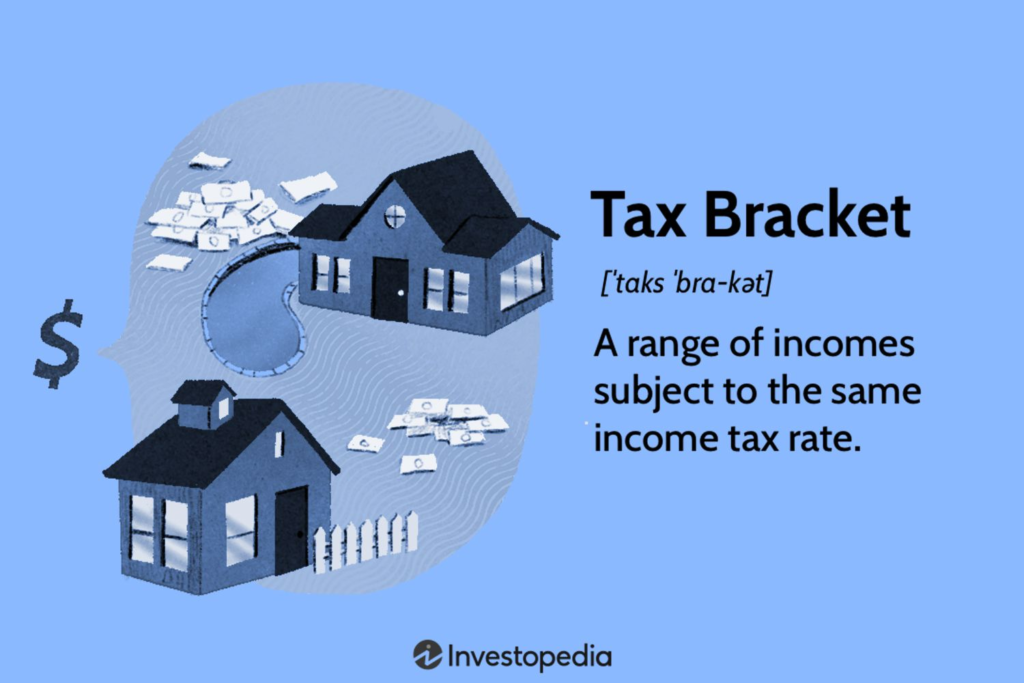

In 2024, federal income tax brackets range from 10% to 37%. Many six-figure earners fall into the 24%, 32%, or even 35% marginal brackets, depending on filing status and deductions. According to the Internal Revenue Service, taxpayers earning above $100,000 often see a noticeable jump in both marginal tax rates and phase-outs for certain credits and deductions.

Without deliberate planning, it’s easy to lose thousands of dollars annually in unnecessary taxes.

Effective tax planning for high earners focuses on three goals:

- Reducing taxable income

- Deferring taxes to future years

- Structuring investments in tax-efficient ways

Importantly, tax planning is not about aggressive loopholes or questionable schemes. Instead, it involves legally optimizing how income, deductions, and investments are structured throughout the year.

Understanding the Tax Challenges Facing Six-Figure Earners

As income rises, taxpayers encounter several structural tax limitations.

One of the biggest surprises for new high earners is the gradual disappearance of certain tax breaks.

For example, higher income can affect:

- Eligibility for direct contributions to a Roth IRA

- Certain education tax credits

- Child tax credit eligibility

- Deduction limits for itemized expenses

Additionally, high earners may face extra taxes such as the Net Investment Income Tax (NIIT) or the Additional Medicare Tax, which applies to wages exceeding $200,000 for single filers.

These thresholds mean that tax planning becomes more proactive. Instead of preparing taxes once a year, successful professionals often evaluate their tax strategy quarterly or even monthly.

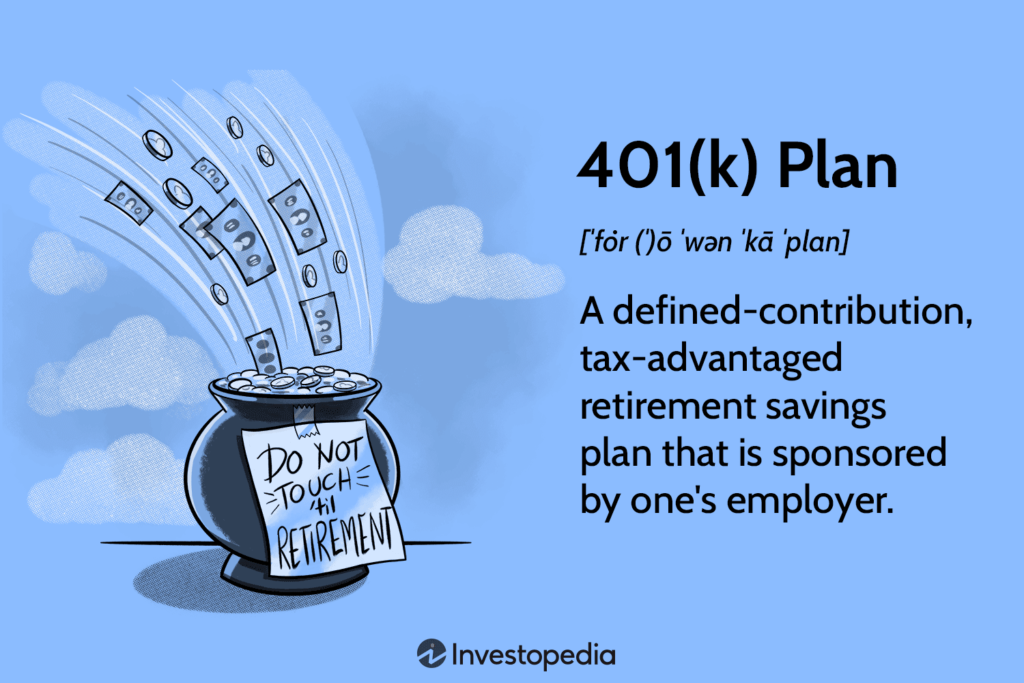

Maximizing Retirement Contributions to Lower Taxable Income

One of the most powerful tax strategies available to six-figure earners is maximizing tax-advantaged retirement accounts.

Contributions to many retirement plans reduce taxable income in the year they are made.

For example:

- Contributions to a 401(k) retirement plan are typically pre-tax, reducing adjusted gross income.

- Contributions to a Traditional IRA may be tax deductible depending on income and employer plan participation.

For 2024, the IRS allows:

- Up to $23,000 in employee contributions to a 401(k)

- An additional $7,500 catch-up contribution for individuals over age 50

For someone earning $150,000 annually, maxing out a 401(k) could reduce taxable income by more than $20,000 per year.

That reduction can potentially save $5,000–$7,000 in federal taxes, depending on the individual’s tax bracket.

Some high earners also use the “backdoor Roth” strategy, which allows indirect funding of a Roth IRA when income exceeds normal eligibility thresholds.

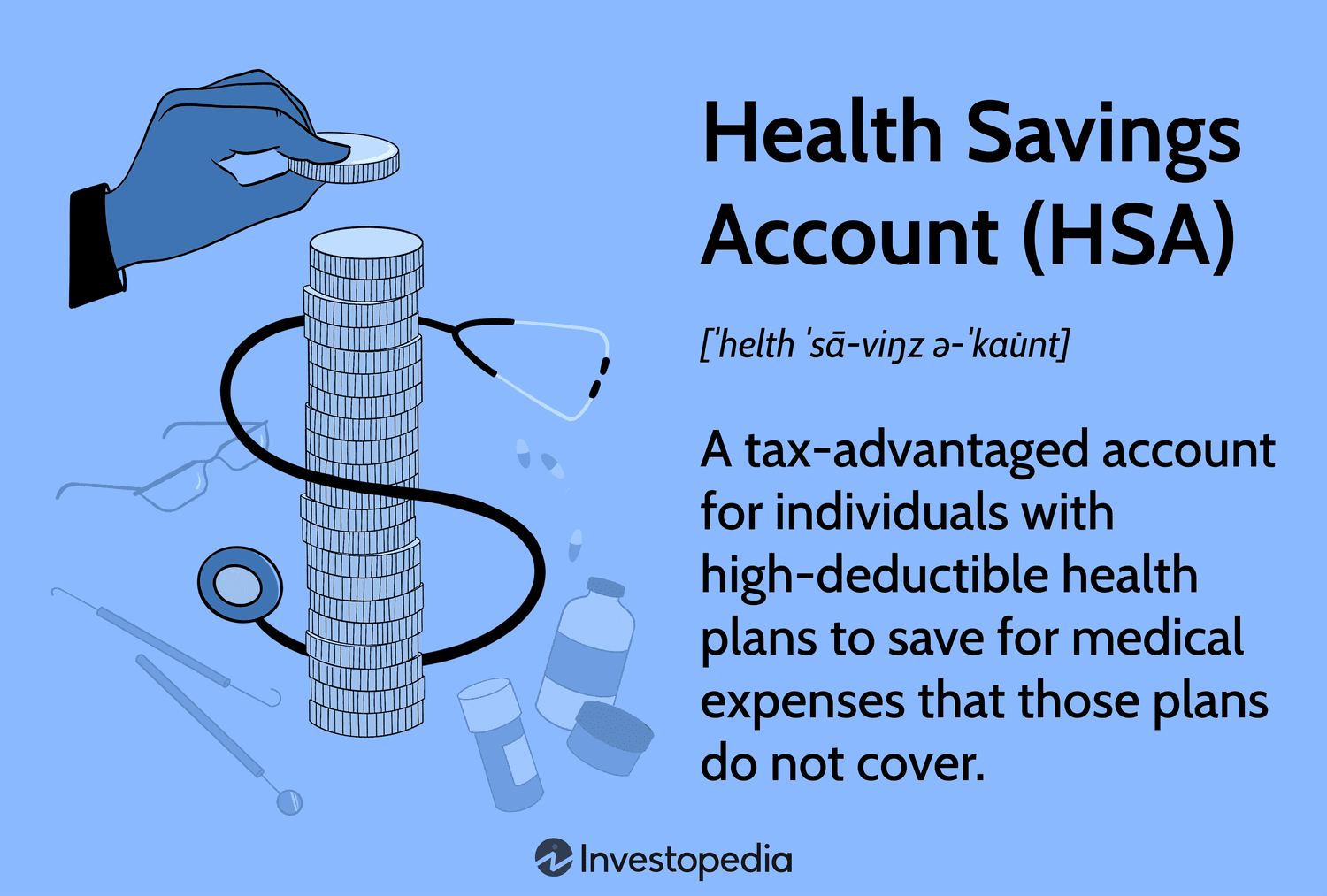

Using Health Savings Accounts for Triple Tax Benefits

Many six-figure earners overlook one of the most tax-efficient accounts available: the Health Savings Account (HSA).

HSAs offer three major tax advantages:

- Contributions are tax deductible

- Investments grow tax free

- Withdrawals for qualified medical expenses are tax free

For 2024, HSA contribution limits are:

- $4,150 for individuals

- $8,300 for families

Financial planners often describe HSAs as “stealth retirement accounts.”

Some high-income households choose to pay medical expenses out of pocket and allow their HSA balance to grow invested for decades. Later, funds can be withdrawn tax-free to reimburse earlier medical expenses or pay healthcare costs in retirement.

Strategic Timing of Income and Bonuses

Income timing can significantly influence a high earner’s tax bill.

Many professionals—especially executives, consultants, and business owners—have some flexibility in when income is received.

Consider this scenario:

A consultant expects a $40,000 bonus in December. If their total income for the year is already pushing them into a higher tax bracket, deferring the bonus until January could move that income into the following tax year.

Common income-timing strategies include:

- Deferring year-end bonuses

- Delaying invoice payments until the following year

- Accelerating deductible expenses before year-end

- Utilizing deferred compensation plans when available

These strategies must be executed carefully and in compliance with IRS rules, but when done correctly they can smooth taxable income across years.

Leveraging Tax-Efficient Investment Strategies

As income rises, investments often become a larger component of financial planning. However, poorly structured portfolios can create unnecessary tax burdens.

Tax-efficient investing focuses on minimizing taxable events.

Key approaches include:

- Holding long-term investments for capital gains treatment

- Prioritizing tax-efficient index funds

- Locating tax-inefficient assets inside retirement accounts

- Using tax-loss harvesting to offset gains

For example, selling investments held longer than one year qualifies for long-term capital gains rates, which range from 0% to 20%, often significantly lower than ordinary income tax rates.

According to the U.S. Securities and Exchange Commission, holding investments long term not only improves tax efficiency but also reduces transaction costs and market timing risks.

Understanding the Value of Itemized Deductions

While many taxpayers take the standard deduction, six-figure earners are more likely to benefit from itemizing.

Key itemized deductions may include:

- Mortgage interest

- State and local taxes (subject to the $10,000 SALT cap)

- Charitable contributions

- Certain medical expenses

Charitable giving can be especially valuable for tax planning.

Donating appreciated assets instead of cash allows taxpayers to avoid capital gains taxes while still receiving a deduction for the full market value of the donation.

Some households also utilize donor-advised funds, which allow contributions to be bundled into a single tax year while distributing donations gradually over time.

Advanced Strategies for High-Income Professionals

For individuals earning well into six figures—especially business owners or self-employed professionals—additional tax strategies may be available.

These include:

- Establishing a defined benefit plan

- Creating a cash balance pension plan

- Utilizing pass-through business deductions

- Structuring income through an S-corporation when appropriate

For example, physicians or consultants earning $300,000 or more may contribute six-figure amounts annually into defined benefit plans, dramatically lowering current taxable income.

However, these strategies require professional oversight from experienced tax advisors.

When It Makes Sense to Work With a Tax Professional

At higher income levels, tax planning becomes more complex.

Mistakes can be costly, especially when dealing with investment income, business deductions, or retirement structures.

Many six-figure earners benefit from working with professionals such as:

- Certified Public Accountants (CPAs)

- Enrolled Agents

- Fee-only financial planners

- Tax attorneys for complex situations

Rather than focusing solely on tax preparation, these professionals help create multi-year tax strategies aligned with long-term financial goals.

According to research from the National Association of Tax Professionals, proactive tax planning can significantly improve after-tax wealth outcomes for high-income households.

Frequently Asked Questions

What qualifies as a six-figure income for tax planning purposes?

Generally, a six-figure income refers to annual earnings between $100,000 and $999,999. Most tax planning strategies discussed here become relevant once income exceeds $100,000 and tax brackets increase.

Do six-figure earners pay significantly higher tax rates?

They often do. Federal marginal tax brackets increase as income rises, meaning additional income may be taxed at 24%, 32%, or higher depending on filing status.

Can high earners still contribute to a Roth IRA?

Direct contributions may be limited due to income thresholds, but many individuals use the backdoor Roth strategy to legally fund a Roth IRA.

Is maxing out a 401(k) really worth it?

Yes. Contributions reduce taxable income and grow tax-deferred. Over decades, this can significantly increase retirement savings while lowering current tax obligations.

What tax mistakes do high earners commonly make?

Common mistakes include:

- Not maximizing retirement contributions

- Poor tax-efficient investing

- Ignoring HSA opportunities

- Failing to plan income timing

Do six-figure earners need a CPA?

Not always, but many benefit from professional guidance, especially when investments, business income, or complex deductions are involved.

Are tax deductions disappearing for higher incomes?

Some deductions phase out or are limited at higher income levels, making proactive tax planning even more important.

Is tax-loss harvesting useful for high earners?

Yes. Tax-loss harvesting allows investors to offset gains and potentially reduce taxable investment income.

How often should tax planning be reviewed?

Most financial professionals recommend reviewing tax strategies at least once per year, and more frequently when income fluctuates.

Can tax planning really make a big difference?

For high earners, strategic planning can save thousands to tens of thousands of dollars annually while improving long-term financial outcomes.

Building a Tax Strategy That Supports Long-Term Wealth

Crossing the six-figure threshold is an important financial milestone, but it also introduces new tax complexities.

Rather than reacting to taxes each April, successful professionals take a proactive approach. By combining retirement optimization, tax-efficient investing, strategic deductions, and professional guidance, six-figure earners can significantly improve after-tax wealth over time.

Tax planning is ultimately about alignment—ensuring that income, investments, and long-term financial goals work together within the tax system rather than against it.

Key Planning Insights for High-Income Households

- Higher income introduces new tax brackets and deduction limits

- Retirement accounts remain one of the most powerful tax-reduction tools

- HSAs offer unmatched triple tax benefits

- Investment structure matters just as much as investment selection

- Income timing strategies can smooth tax liability

- Charitable giving can enhance both tax efficiency and impact

- Professional tax advice becomes more valuable as income rises