Digital assets now extend far beyond Bitcoin. For U.S. investors in 2026, the category includes cryptocurrencies, stablecoins, tokenized securities, digital funds, and blockchain-based real estate interests. Regulation, institutional adoption, and improved custody standards have reshaped risk and access. Understanding how each asset functions—legally, structurally, and economically—is essential before allocating capital in this evolving market.

The Expanding Definition of “Digital Assets”

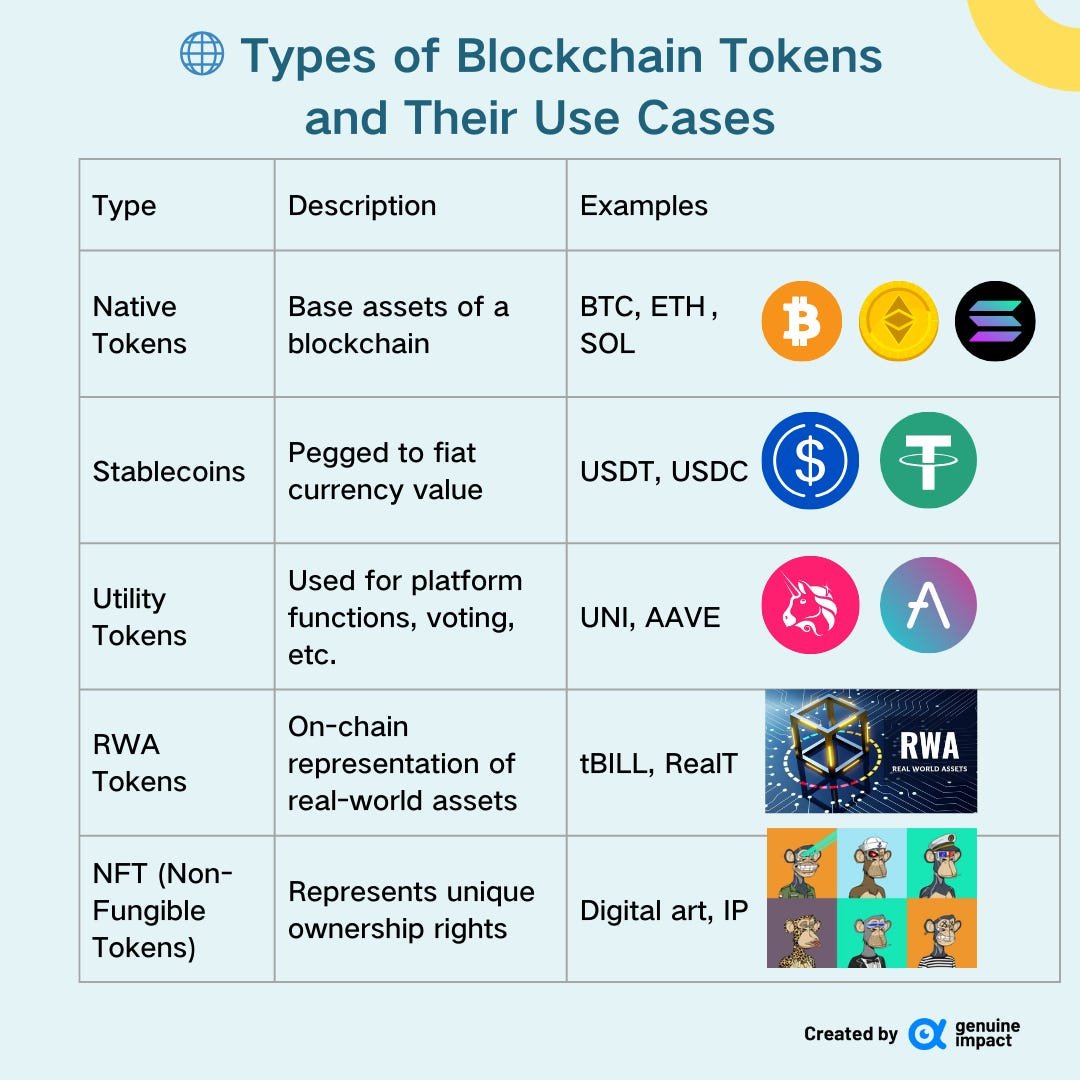

A decade ago, most Americans equated digital assets with Bitcoin. Today, the term encompasses a far broader ecosystem that includes tokenized real estate, blockchain-based private credit, digital securities, stablecoins, and regulated exchange-traded products.

At its core, a digital asset is any asset issued, transferred, or recorded using blockchain or distributed ledger technology. But from an investor’s perspective, that definition is too abstract. What matters more is how these assets behave—how they generate returns, how they are regulated, how they are taxed, and how they fit into a diversified portfolio.

In 2026, digital assets sit at the intersection of finance and technology. Institutional infrastructure has matured. Custody solutions have improved. Oversight from agencies like the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission has clarified many compliance questions. But complexity remains.

How Americans Are Actually Investing in Digital Assets

Search data shows Americans asking practical questions:

- “Is crypto still worth investing in?”

- “What is tokenized real estate?”

- “Are digital assets safe?”

- “Can I put crypto in my IRA?”

The answers depend heavily on the type of digital asset involved.

Broadly, today’s digital asset categories include:

- Cryptocurrencies (e.g., Bitcoin, Ethereum)

- Stablecoins pegged to the U.S. dollar

- Tokenized securities (stocks, bonds, funds)

- Tokenized real estate

- Blockchain-based private credit or venture funds

- Digital asset ETFs

Each carries distinct risk characteristics and regulatory treatment.

Bitcoin and Public Cryptocurrencies: Volatility with Institutional Structure

Bitcoin remains the anchor of the digital asset market. With a fixed supply and decentralized design, it is often compared to digital gold. However, investors should understand that its price volatility remains significantly higher than traditional equities.

The key shift between 2022 and 2026 is not volatility reduction—but structural integration.

The approval and growth of spot Bitcoin ETFs have allowed investors to gain exposure without directly holding private keys. Institutional custodians now provide insured storage. Major asset managers offer Bitcoin allocations within diversified funds.

Still, Bitcoin does not produce cash flow. Its return profile depends on supply-demand dynamics and market adoption. For investors evaluating allocation, it behaves more like a speculative commodity than a traditional income-producing asset.

Stablecoins: Digital Dollars with Oversight

Stablecoins aim to maintain a 1:1 value with the U.S. dollar. By 2026, regulatory requirements mandate higher reserve transparency and periodic attestations for major issuers.

For investors, stablecoins are less about appreciation and more about utility:

- Settlement between exchanges

- On-chain yield products

- Cross-border transfers

- Treasury management for fintech firms

They are not bank deposits. Most are not FDIC-insured. However, oversight has improved operational transparency compared to earlier years.

Tokenized Securities: Traditional Assets on Blockchain Rails

Tokenization refers to issuing ownership interests in assets as blockchain-based tokens. These can represent shares in private companies, investment funds, or debt instruments.

Why does this matter?

Because tokenization can streamline settlement, enable fractional ownership, and reduce administrative friction. However, tokenized securities are still subject to U.S. securities law.

For example, a tokenized private equity fund must comply with offering exemptions, investor accreditation rules, and transfer restrictions. The technology changes how ownership is recorded—but not the legal obligations.

Investors should evaluate these products the same way they evaluate traditional private placements:

- Who is the issuer?

- What are the audited financials?

- What are the liquidity constraints?

- What are the fees?

Blockchain does not remove due diligence requirements.

Tokenized Real Estate: Access Meets Illiquidity

Tokenized real estate has attracted attention because it promises fractional access to property markets. Instead of purchasing an entire rental property, investors can buy digital tokens representing a percentage of ownership.

In theory, this lowers entry barriers. In practice, liquidity depends on secondary markets.

Consider a U.S.-based investor purchasing tokenized shares in a multifamily property in Texas. The investment may provide rental income distributions and potential appreciation. However:

- Tokens may only trade on limited platforms.

- Transfer restrictions may apply.

- Valuation updates may occur quarterly rather than daily.

Tokenized real estate is not equivalent to publicly traded REITs. Liquidity and pricing transparency differ substantially.

That said, it offers a new channel for portfolio diversification—especially for investors comfortable with private-market exposure.

Digital Asset ETFs and Retirement Accounts

One of the most common questions Americans ask is whether digital assets can be held in retirement accounts.

In 2026, exposure is possible through:

- Spot Bitcoin ETFs

- Blockchain-focused equity funds

- Self-directed IRAs holding digital assets through approved custodians

However, retirement account investors must consider:

- Custody fees

- Volatility tolerance

- Regulatory risk

- Required minimum distribution implications

Financial advisors increasingly treat digital assets as a satellite allocation rather than a core retirement holding.

Risk Considerations: What Investors Must Evaluate

Digital assets introduce unique risks beyond price fluctuation.

Operational Risk

Exchange solvency, cybersecurity breaches, and custodial failures remain relevant.

Regulatory Risk

Court decisions and legislative updates can impact classification and trading access.

Liquidity Risk

Many tokenized assets trade on limited platforms.

Technology Risk

Smart contract bugs or blockchain congestion can affect execution.

Tax Complexity

The Internal Revenue Service treats digital assets as property for tax purposes, meaning capital gains rules apply to most transactions.

Investors should not assume uniform treatment across asset categories.

Real-World Portfolio Example

Consider a hypothetical $500,000 diversified portfolio in 2026.

An investor might allocate:

- 60% U.S. equities

- 25% fixed income

- 10% international equities

- 5% digital assets

Within the 5% digital allocation:

- 3% Bitcoin ETF

- 1% tokenized real estate fund

- 1% blockchain infrastructure ETF

This structure reflects measured exposure rather than concentrated speculation. It also acknowledges that digital assets behave differently across economic cycles.

Are Digital Assets Now Mainstream?

Institutional participation suggests integration, not dominance.

Large asset managers offer digital products. Banks provide custody services. Corporate treasuries hold limited crypto reserves. Yet total digital asset market capitalization remains small relative to global equities and bond markets.

Mainstream does not mean low-risk. It means regulated access.

Investors should approach digital assets the way they approach emerging markets or alternative investments: with research, allocation discipline, and realistic expectations.

Frequently Asked Questions

1. What qualifies as a digital asset in 2026?

Cryptocurrencies, stablecoins, tokenized securities, tokenized real estate, and blockchain-based investment funds.

2. Is Bitcoin still the most important digital asset?

Yes. It remains the largest by market capitalization and the most institutionally integrated.

3. Is tokenized real estate safer than crypto?

Not necessarily. It may offer income potential but carries liquidity and operational risks.

4. Are digital assets regulated in the U.S.?

Yes, under frameworks involving the SEC, CFTC, banking regulators, and state authorities.

5. Do digital assets generate income?

Some do. Tokenized real estate and private credit may generate cash flow; Bitcoin does not.

6. Can I hold digital assets in my 401(k)?

Direct access varies by plan, but ETFs may be available in certain retirement accounts.

7. How are digital assets taxed?

Generally as property, triggering capital gains upon sale or exchange.

8. What percentage of a portfolio should be digital assets?

Many advisors suggest a small allocation—often 1–5%—depending on risk tolerance.

9. Are tokenized assets liquid?

Liquidity varies widely and depends on platform access and regulatory constraints.

The Investor’s New Due Diligence Checklist

Digital assets have evolved from niche speculation to a regulated segment of the broader financial system. Yet complexity demands scrutiny.

Before investing, Americans should evaluate:

- Legal classification

- Custody structure

- Fee transparency

- Liquidity constraints

- Tax implications

- Issuer credibility

Blockchain technology changes how ownership is recorded. It does not eliminate investment fundamentals.

The Reality Behind the Digital Asset Label

“Digital asset” is not a single investment—it is a delivery mechanism. Bitcoin, tokenized real estate, and blockchain funds differ as much as gold, rental property, and venture capital differ in traditional finance.

In 2026, the opportunity lies not in chasing headlines but in understanding structure. Investors who differentiate between utility, speculation, income, and infrastructure will be better positioned than those treating digital assets as a monolithic trend.

The market is maturing. The responsibility to evaluate it remains unchanged.

A Clear-Eyed Perspective for Modern Portfolios

- Digital assets include far more than cryptocurrencies.

- Regulation has improved transparency but not eliminated risk.

- Tokenized real estate offers access but limited liquidity.

- Bitcoin remains volatile and non-income producing.

- Tax treatment requires careful reporting.

- Small, diversified allocations are common among advisors.