Summary

Tax preparation and tax strategy are often treated as interchangeable, but they serve very different purposes. One focuses on reporting the past; the other shapes future financial outcomes. Understanding how they differ—and how they work together—can help individuals and businesses make better decisions, reduce surprises, and build more tax-efficient financial lives over time.

Why This Distinction Matters More Than Most People Realize

Many Americans only think about taxes when a filing deadline approaches. W-2s are gathered, forms are completed, and a return is submitted. That process—tax preparation—is essential, but it is inherently backward-looking. It reports what already happened.

Tax strategy, by contrast, is forward-looking. It involves planning decisions made throughout the year, and often across multiple years, to influence how much tax you legally owe in the future. Confusing the two can lead to missed opportunities, unnecessary tax bills, and reactive financial decisions that compound over time.

Understanding the difference isn’t about becoming aggressive or exploiting loopholes. It’s about clarity: knowing what each function does, when it matters, and how they fit into a broader financial picture.

What Tax Preparation Actually Does

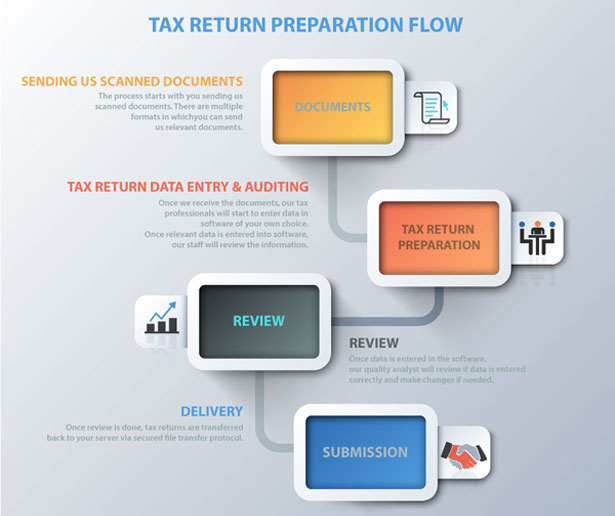

Tax preparation is the process of accurately compiling financial information and submitting required tax forms to federal and state authorities. Its primary goal is compliance.

A tax preparer’s responsibilities typically include:

- Collecting income documentation (W-2s, 1099s, K-1s)

- Applying deductions and credits based on existing records

- Calculating tax owed or refund due

- Filing returns correctly and on time

The value of tax preparation lies in accuracy and adherence to current law. A skilled preparer ensures numbers are correct, deadlines are met, and obvious deductions are not overlooked.

What tax preparation does not do is meaningfully change outcomes after the fact. By the time a return is prepared, nearly all tax-relevant decisions—income timing, retirement contributions, asset sales—have already been made.

What Tax Strategy Is Designed to Do

Tax strategy focuses on intentional decision-making before and during the year, not after it ends. The goal is to structure income, investments, and transactions in ways that are tax-efficient over time while remaining fully compliant with the law.

Unlike preparation, tax strategy is continuous. It evolves as income changes, laws shift, and life circumstances develop.

Effective tax strategy often considers:

- When income is earned or deferred

- How investments are held and sold

- Which accounts are used for savings

- How business or compensation structures are designed

- How current decisions affect future tax brackets

Rather than asking, “What do I owe?” tax strategy asks, “How do today’s decisions affect what I’ll owe next year—and five years from now?”

A Simple Example That Shows the Difference

Consider two professionals who each earn $180,000 per year.

Both hire competent tax preparers. Their returns are accurate, compliant, and filed on time.

One individual contributes irregularly to retirement accounts, sells investments without regard to timing, and accepts year-end bonuses without planning. The other coordinates retirement contributions, manages capital gains timing, and adjusts withholding based on projected income.

At filing time, both returns are prepared correctly. But their outcomes differ meaningfully—not because of preparation quality, but because one engaged in strategy throughout the year and the other did not.

The tax code rewards planning, not hindsight.

Why Tax Preparation Alone Often Falls Short

Tax preparation is constrained by what already happened. Even the most skilled preparer cannot retroactively change:

- Missed retirement contribution windows

- Poorly timed asset sales

- Suboptimal filing status decisions left unaddressed

- Business deductions not properly structured during the year

According to IRS data, a significant percentage of taxpayers either under-withhold or face unexpected balances due each year—often because planning decisions were never revisited as income changed.

Preparation catches errors. Strategy reduces regret.

When Tax Strategy Becomes Especially Important

While everyone benefits from some level of tax awareness, strategy becomes particularly valuable during periods of financial change.

Common trigger points include:

- Income increases or variable compensation

- Starting or selling a business

- Marriage, divorce, or dependents

- Major investment activity

- Approaching retirement

- Relocation between states

These moments introduce complexity that preparation alone cannot address. Strategic guidance helps align decisions across tax years rather than reacting after consequences are locked in.

How Professionals Approach Tax Strategy

Tax strategy is rarely a single tactic. Instead, it is a coordinated approach that balances tax efficiency with broader financial goals.

Experienced advisors typically:

- Project multi-year tax outcomes rather than focusing on one return

- Evaluate tradeoffs between taxes, liquidity, and risk

- Adjust strategies as laws and personal circumstances evolve

- Coordinate tax planning with investment and retirement planning

Importantly, strategy does not mean minimizing taxes at all costs. It means optimizing decisions within legal boundaries while supporting long-term stability.

The Relationship Between Strategy and Preparation

Tax preparation and tax strategy are not competitors. They are complementary.

Preparation provides:

- Compliance

- Accuracy

- Documentation

- Risk management

Strategy provides:

- Direction

- Intentionality

- Predictability

- Long-term efficiency

The most effective outcomes occur when both functions are aligned—when preparation reflects thoughtful planning already in place, rather than scrambling to salvage results after the year ends.

Common Misconceptions That Blur the Line

Many people assume they are “doing tax planning” because:

- Their preparer finds deductions

- They receive a refund

- Their taxes feel straightforward

In reality, deductions found during preparation are often limited and reactive. True strategy happens earlier and influences the data that eventually shows up on a return.

Another misconception is that tax strategy is only for the wealthy. While complexity increases with income, even modest earners benefit from understanding how timing, account choice, and life decisions affect taxes.

How to Know Which You’re Getting

A simple test: look at the timing of the conversation.

If tax discussions only happen after January, the focus is preparation.

If conversations happen throughout the year, especially before decisions are finalized, strategy is likely involved.

Strategic discussions tend to include projections, “what-if” scenarios, and long-term tradeoffs—not just forms and deadlines.

Frequently Asked Questions

Is tax preparation legally required?

Yes. Filing accurate tax returns is mandatory for individuals and businesses that meet filing thresholds.

Is tax strategy legal?

Yes. Tax strategy involves lawful planning within existing tax rules. It is distinct from evasion or improper reporting.

Can one professional handle both?

Sometimes. Some CPAs and advisors provide both services, but many focus primarily on preparation.

How often should tax strategy be reviewed?

At least annually, and whenever major financial or life changes occur.

Does tax strategy guarantee lower taxes?

No guarantees exist, but strategy improves predictability and reduces avoidable inefficiencies.

Is tax software enough for strategy?

Software helps with preparation. It rarely offers personalized, forward-looking planning.

Do refunds mean taxes were optimized?

Not necessarily. Refunds often indicate over-withholding, not strategic efficiency.

When should someone start thinking about tax strategy?

Ideally as soon as income becomes variable or financial complexity increases.

Does tax strategy replace financial planning?

No. It works best as part of a broader financial plan.

Seeing Taxes as a System, Not an Event

The biggest shift many taxpayers make is realizing that taxes are not a once-a-year obligation, but an ongoing system shaped by everyday decisions. Preparation closes the books. Strategy writes the story.

When those roles are clearly understood, tax conversations become less stressful, more proactive, and far more useful.

Key Distinctions at a Glance

- Tax preparation reports what already happened

- Tax strategy influences what will happen next

- Preparation ensures compliance

- Strategy supports long-term efficiency

- Both are necessary, but they serve different purposes