Asset tokenization—the process of representing ownership rights on blockchain networks—is reshaping segments of traditional finance. From tokenized U.S. Treasuries to fractional real estate and private credit, financial institutions are integrating distributed ledger technology into settlement, custody, and issuance processes. While regulatory, liquidity, and operational risks remain, tokenization is increasingly viewed as infrastructure—not speculation.

What Is Asset Tokenization, and Why Does It Matter?

Asset tokenization refers to the digital representation of real-world financial assets—such as stocks, bonds, real estate, or private funds—on blockchain networks. Instead of recording ownership through traditional centralized ledgers, tokenized assets are issued and transferred using distributed ledger technology.

In practical terms, tokenization does not change the underlying asset. A tokenized Treasury bill is still a Treasury bill. A tokenized share of a building still represents ownership interest in that building. What changes is the mechanism for recording, transferring, and potentially settling ownership.

The significance lies in infrastructure efficiency. Traditional financial systems rely on layers of intermediaries—clearinghouses, custodians, transfer agents. Blockchain-based systems promise faster settlement, programmable compliance, and fractional ownership structures.

Importantly, tokenization is not occurring outside regulatory oversight. Institutions engaging in this space operate within frameworks established by agencies such as the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission.

Why Traditional Finance Is Paying Attention

Tokenization has moved beyond fintech startups. Major asset managers and banks are now experimenting with blockchain-based issuance and settlement.

Several factors are driving this shift:

- Rising settlement costs in traditional markets

- Demand for near-instant transaction finality

- Interest in 24/7 trading capabilities

- Growth of digital-native investors

- Competitive pressure from global markets

In recent years, firms like BlackRock have launched tokenized fund initiatives, while global banks including JPMorgan Chase have tested blockchain settlement platforms.

According to industry research from firms such as Boston Consulting Group, tokenized assets could represent trillions of dollars in value over the next decade. While forecasts vary, the strategic direction is clear: blockchain is being treated as financial plumbing rather than a speculative experiment.

What Types of Assets Are Being Tokenized?

Tokenization spans multiple asset classes. Each carries different implications for investors.

1. Tokenized U.S. Treasuries

Short-term Treasury products have emerged as early candidates for tokenization because they are relatively simple, liquid, and standardized.

Benefits include:

- Faster settlement

- Automated coupon payments

- Fractional investment access

For corporate treasurers, tokenized Treasuries can integrate into blockchain-based liquidity management systems.

2. Tokenized Real Estate

Real estate tokenization enables fractional ownership in commercial or residential properties. Instead of purchasing a full property, investors buy digital shares representing economic rights.

However, these tokens are often structured as securities and subject to transfer restrictions. Liquidity may depend on secondary marketplaces with limited volume.

Tokenized real estate is not equivalent to publicly traded REITs; it more closely resembles private placements with blockchain-based recordkeeping.

3. Tokenized Private Credit and Funds

Private credit funds and alternative investment vehicles increasingly use tokenization to streamline capital calls and distributions.

Smart contracts can automate:

- Dividend payments

- Voting rights

- Compliance restrictions

- Transfer limitations

The asset itself remains subject to securities law, but operational efficiency improves.

How Blockchain Infrastructure Changes Settlement

Traditional equity trades in the U.S. historically settled on a T+2 basis (two business days after trade execution), recently shortened to T+1. Blockchain systems offer the potential for near-instant settlement.

Why does this matter?

Settlement risk—also called counterparty risk—exists in the gap between trade execution and final settlement. By reducing that window, tokenization may lower capital requirements tied to clearing and collateral.

However, real-world adoption requires coordination among exchanges, custodians, regulators, and clearing entities. Instant settlement is not automatically superior; liquidity management and operational readiness must align.

Regulatory Considerations in the United States

Many Americans ask: “Is tokenization legal?”

Yes—but context matters.

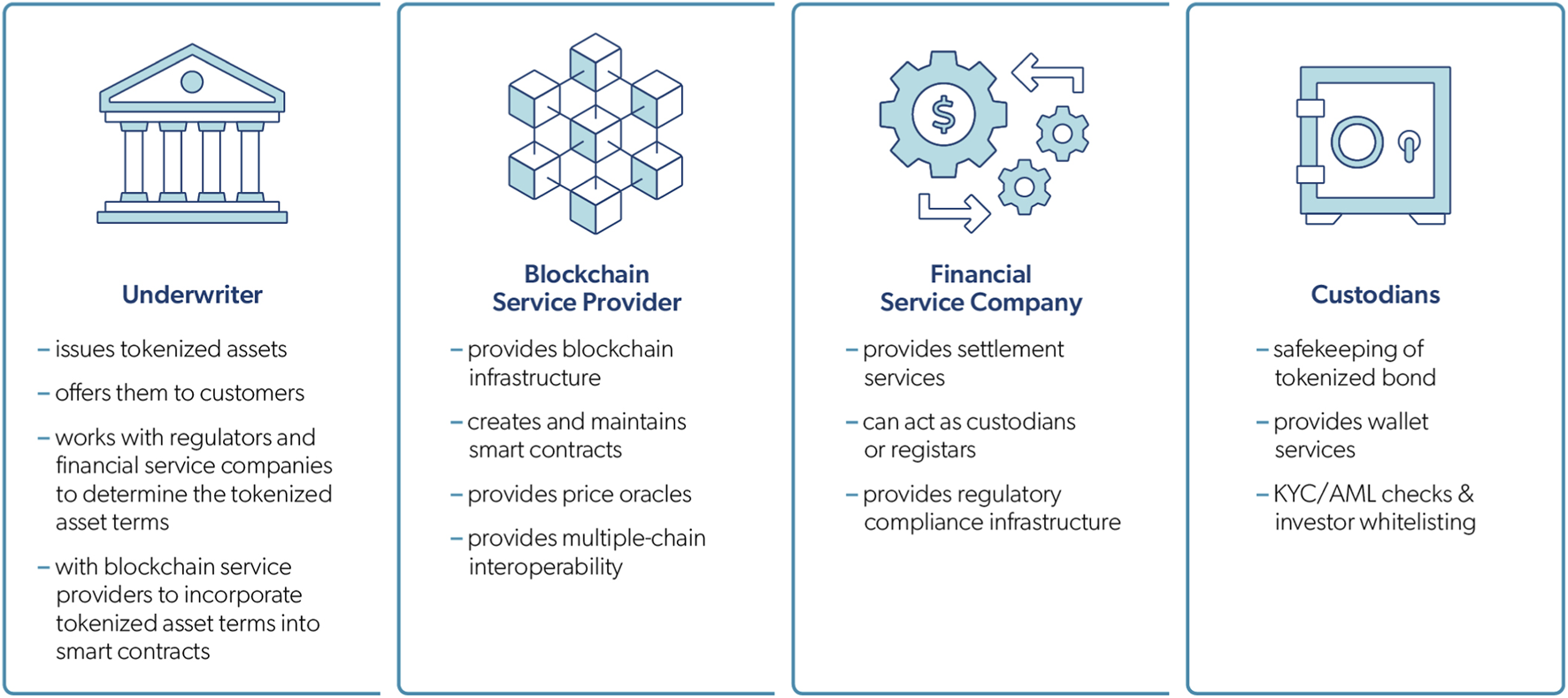

Tokenized securities remain securities under U.S. law. Issuers must comply with registration requirements or exemptions. Transfer agents must follow regulatory standards. Custodians must safeguard assets according to SEC guidance.

Tax treatment also follows traditional rules. The Internal Revenue Service treats digital assets as property for tax purposes, meaning gains and losses are taxable upon sale or exchange.

Additionally, banking regulators and the Federal Reserve evaluate how blockchain-based systems integrate with existing payment and settlement infrastructure.

Tokenization changes technology layers—not legal obligations.

Real-World Example: A Tokenized Real Estate Offering

Consider a U.S.-based commercial property developer issuing tokenized shares in a mixed-use building.

The developer structures the offering as a Regulation D private placement. Accredited investors purchase blockchain-based tokens representing limited partnership interests.

Behind the scenes:

- A smart contract tracks ownership

- Rental income distributions are automated

- Transfer restrictions are coded into the token

- Secondary trading is limited to approved platforms

From the investor’s perspective, the economic exposure resembles traditional private real estate. The difference lies in administrative efficiency and fractional accessibility.

Liquidity, however, remains limited compared to public markets.

Institutional Motivations: Cost, Access, and Automation

Traditional financial institutions approach tokenization pragmatically. Their motivations include:

Operational Efficiency

Reducing manual reconciliation processes.

Capital Optimization

Lowering collateral needs through faster settlement.

Market Expansion

Reaching global investors via digital platforms.

Programmability

Embedding compliance directly into asset transfers.

For example, programmable compliance can restrict token transfers to verified investors, reducing regulatory breach risk.

Risks and Limitations Investors Should Understand

Tokenization is infrastructure innovation, not risk elimination.

Key considerations include:

- Liquidity Constraints – Many tokenized assets trade on limited venues.

- Smart Contract Risk – Coding errors can disrupt functionality.

- Regulatory Uncertainty – Ongoing rulemaking may affect structures.

- Custody Complexity – Digital wallets introduce operational risks.

- Market Fragmentation – Competing blockchain standards may reduce interoperability.

Investors should evaluate tokenized products with the same scrutiny applied to traditional private investments.

How Financial Advisors Are Approaching Tokenized Assets

Advisors increasingly treat tokenized assets as alternative investments rather than core holdings.

Portfolio integration often follows principles such as:

- Limiting allocation percentages

- Assessing liquidity needs

- Evaluating sponsor credibility

- Reviewing fee transparency

For retirement-focused investors, liquidity and regulatory clarity remain primary considerations.

Frequently Asked Questions

1. What does tokenization mean in finance?

It means representing ownership of real-world assets on blockchain networks.

2. Is tokenized real estate safer than traditional real estate?

No. It carries similar economic risks, plus additional technological considerations.

3. Can retail investors access tokenized assets?

Some offerings are limited to accredited investors, though access varies by structure.

4. Are tokenized assets insured?

Insurance depends on custody arrangements, not tokenization itself.

5. How are tokenized assets taxed?

Generally under standard capital gains rules.

6. Is tokenization the same as cryptocurrency?

No. Tokenization often represents traditional assets, not native cryptocurrencies.

7. Do tokenized assets trade 24/7?

Some platforms allow extended trading, but liquidity may be limited.

8. Are banks involved in tokenization?

Yes. Major financial institutions are experimenting with blockchain settlement systems.

9. Does tokenization eliminate intermediaries?

It may reduce certain administrative layers but does not remove regulatory oversight.

The Broader Infrastructure Shift

Asset tokenization represents a structural adaptation by traditional finance. Instead of resisting blockchain technology, institutions are integrating it into existing regulatory and operational frameworks.

The transition is incremental. It involves pilots, limited rollouts, and regulatory coordination. It does not imply wholesale replacement of legacy systems.

What it does signal is a long-term infrastructure evolution.

Where Tokenization Fits in Modern Portfolios

For investors, tokenized assets are best viewed as a delivery mechanism rather than a new asset class.

A tokenized bond behaves like a bond. A tokenized fund behaves like a fund. The underlying economics remain central.

The opportunity lies in operational improvement—not speculative novelty.

Finance at an Infrastructure Crossroads

Traditional finance is not abandoning its foundations. It is modernizing them.

Blockchain technology is being tested not as a parallel financial system, but as a back-end upgrade. The institutions driving this shift are not fringe innovators—they are established asset managers, banks, and regulators.

Tokenization’s future depends less on enthusiasm and more on execution: compliance integration, liquidity development, and operational resilience.

The rise of asset tokenization is not about disruption for its own sake. It is about infrastructure alignment with a digital economy.

Structural Shifts Worth Watching

- Expansion of tokenized Treasury markets

- SEC rule updates on digital custody

- Increased participation from major banks

- Standardization of blockchain settlement protocols

- Growth in secondary trading platforms

Signals from the Blockchain Integration Era

- Tokenization modernizes settlement infrastructure rather than replacing assets.

- Regulatory compliance remains central to adoption.

- Liquidity and interoperability will determine scalability.

- Institutional participation is accelerating cautiously.