Many first-time entrepreneurs focus heavily on revenue, growth, and product development, yet overlook the operational realities of cash flow. Even profitable businesses can fail if cash arrives too late or expenses rise too quickly. Understanding cash flow timing, financial forecasting, payment cycles, and working capital is essential for building a resilient business in the early stages.

Why Cash Flow Is the Lifeline of Every New Business

For many first-time entrepreneurs, success initially feels tied to sales numbers. When orders increase or customers start signing contracts, it appears that the business is on the right track.

However, experienced operators know that revenue and cash flow are not the same thing.

A company may report strong sales yet struggle to pay employees, suppliers, or operating costs if incoming payments arrive slowly. According to the U.S. Small Business Administration, poor cash flow management is one of the most common reasons young businesses fail.

Cash flow simply refers to the movement of money in and out of the business. Positive cash flow means more cash is entering the business than leaving it. Negative cash flow means the opposite.

For early-stage companies, managing this movement carefully often matters more than profit margins during the first few years.

The Revenue vs. Cash Flow Misunderstanding

One of the most common financial misconceptions among new entrepreneurs is assuming that revenue equals available money.

In reality, many businesses operate with delayed payment cycles. For example, a consulting firm may send a $50,000 invoice to a client but receive payment 30 or 60 days later.

Meanwhile, the company must still cover:

- Employee salaries

- Software subscriptions

- Marketing expenses

- Office rent or operating costs

This gap between earning revenue and receiving payment can quickly create financial stress.

The National Federation of Independent Business has reported that delayed customer payments remain one of the top financial challenges for small companies in the United States.

Understanding this timing difference early can prevent costly surprises.

Why Fast Growth Can Create Cash Problems

It may sound counterintuitive, but rapid growth can sometimes create more cash flow pressure than slow growth.

Imagine a small product company that suddenly lands a large retail contract. While the deal looks promising, fulfilling the order may require upfront spending on manufacturing, inventory, packaging, and shipping.

If the retailer pays 60 or 90 days later, the company must finance production before receiving revenue.

Many founders underestimate how much working capital growth requires.

Common growth-related cash pressures include:

- Purchasing inventory before sales are completed

- Hiring staff ahead of demand

- Increasing marketing budgets

- Expanding infrastructure or technology

Without careful planning, growth can temporarily strain finances even in successful companies.

The Importance of Understanding Payment Cycles

Cash flow depends heavily on how quickly money moves through the business.

Payment cycles influence how long it takes to convert work or sales into usable cash.

For example:

- Retail businesses often receive immediate payments from customers

- Consulting firms may operate with 30–90 day invoices

- Manufacturing companies may wait even longer depending on supply chains

Entrepreneurs who understand these cycles can plan expenses accordingly.

A key step is mapping the full cash timeline—from paying suppliers to receiving payment from customers.

When founders visualize this cycle, they gain a clearer picture of how much capital the business needs to operate smoothly.

Expense Timing Often Surprises New Founders

While revenue may arrive slowly, expenses often occur immediately.

Operational costs tend to appear early and consistently, including:

- Payroll obligations

- Insurance payments

- Equipment purchases

- Software subscriptions

- Taxes and regulatory fees

New entrepreneurs sometimes underestimate how quickly these obligations accumulate.

Data from U.S. Bureau of Labor Statistics shows that many young businesses close within their first five years, often due to financial management challenges rather than lack of demand.

Careful budgeting and financial forecasting help prevent this imbalance between income and expenses.

Forecasting Cash Flow: A Habit Experienced Founders Develop

Successful entrepreneurs rarely wait until financial problems appear before reviewing cash flow.

Instead, they build forecasts that estimate how cash will move through the business over time.

A basic cash flow forecast typically tracks:

- Expected incoming payments

- Upcoming operating expenses

- Payroll obligations

- Loan payments or financing costs

Forecasts are usually updated monthly or even weekly for young companies.

This habit allows leaders to anticipate financial gaps before they become emergencies.

For example, if a forecast shows a shortfall two months ahead, the company has time to adjust spending or accelerate customer payments.

Customer Payment Policies Can Shape Financial Stability

Many founders assume payment terms are fixed. In reality, payment policies can significantly influence cash flow.

Businesses sometimes improve financial stability by adjusting how and when customers pay.

Common approaches include:

- Requesting partial payments upfront

- Offering small discounts for early payments

- Using milestone billing for large projects

- Requiring deposits before beginning work

For instance, a marketing agency might collect 40% of a project fee before starting work and the remainder upon completion.

These practices reduce financial risk while keeping relationships professional and transparent.

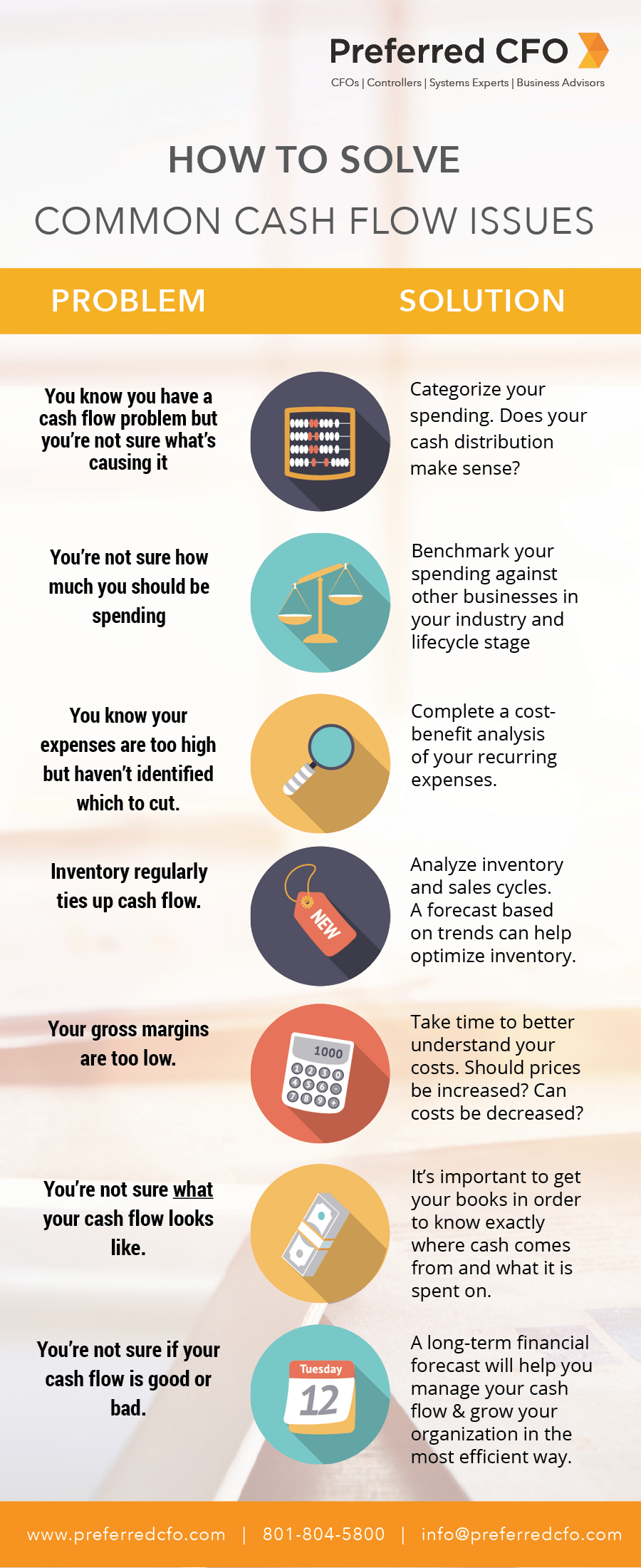

Inventory Management and Cash Flow

Inventory-heavy businesses face unique cash flow challenges.

Retailers, manufacturers, and product-based startups often must pay suppliers well before selling goods to customers.

If inventory moves slowly, money becomes tied up in unsold products.

Effective inventory management helps prevent this situation.

Key strategies include:

- Tracking product turnover rates

- Avoiding excessive stock levels

- Negotiating better supplier payment terms

- Using smaller, more frequent orders when possible

These adjustments help keep cash circulating rather than sitting idle in warehouses or storage.

The Role of Financial Visibility

Another issue that new entrepreneurs overlook is how difficult it can be to track finances without proper systems.

In the early stages, some founders manage finances informally through spreadsheets or personal accounts.

As the business grows, clearer financial visibility becomes essential.

Many companies adopt accounting platforms or financial dashboards that track:

- Real-time cash balances

- Incoming invoices

- Upcoming expenses

- Profit and loss trends

This visibility allows founders to make decisions based on current data rather than assumptions.

Why Experienced Entrepreneurs Protect Cash Reserves

Seasoned business leaders rarely rely entirely on predictable revenue. Instead, they build financial cushions that allow the company to withstand unexpected challenges.

Cash reserves help businesses manage:

- Economic downturns

- Unexpected expenses

- Delayed customer payments

- Seasonal fluctuations in demand

Financial advisors often recommend maintaining several months of operating expenses as a reserve when possible.

While early startups may not always achieve this immediately, building reserves over time strengthens stability.

Frequently Asked Questions

1. What is cash flow in simple terms?

Cash flow refers to the movement of money into and out of a business during a specific period.

2. Why do profitable businesses sometimes fail?

A business may be profitable on paper but still run out of cash if payments arrive too slowly while expenses continue.

3. How often should entrepreneurs review cash flow?

Many small businesses review cash flow weekly or monthly to stay aware of financial trends.

4. What is a cash flow forecast?

A forecast estimates future cash inflows and outflows based on expected revenue and expenses.

5. How can small businesses improve cash flow?

Common methods include adjusting payment terms, reducing unnecessary expenses, and improving inventory management.

6. What are payment terms?

Payment terms define when customers must pay invoices, such as 30 or 60 days after receiving a bill.

7. Do all businesses face cash flow challenges?

Nearly every growing business experiences cash flow pressures at some point, especially in early stages.

8. How much cash reserve should a business have?

Many advisors suggest maintaining three to six months of operating expenses when possible.

9. Is revenue growth enough to ensure financial stability?

No. Growth must be matched with careful cash flow management to sustain operations.

10. What tools help track cash flow?

Accounting software, financial dashboards, and regular financial reporting can all improve visibility.

Building Financial Awareness Early Makes Entrepreneurship More Sustainable

For first-time entrepreneurs, cash flow can seem like a technical accounting concept rather than a daily operational reality. Yet experienced founders often view it as the most important financial indicator in the early years of a business.

Understanding payment timing, expense cycles, and working capital needs allows entrepreneurs to make informed decisions about hiring, marketing, and expansion.

Companies that build strong financial habits early gain flexibility, stability, and the confidence to pursue growth without unnecessary financial stress.

In many ways, managing cash flow effectively is less about complex financial models and more about awareness, discipline, and consistent monitoring.

Essential Cash Flow Lessons for First-Time Entrepreneurs

- Revenue does not always translate into immediate cash

- Payment cycles determine when money actually arrives

- Fast growth can temporarily increase financial pressure

- Forecasting helps anticipate financial gaps early

- Payment policies influence cash stability

- Inventory management affects working capital

- Financial visibility improves decision-making

- Cash reserves provide protection during uncertainty