Summary

Structuring owner compensation is one of the most important financial decisions business owners make. Advisors evaluate taxes, business structure, cash flow stability, compliance risks, and long-term financial planning before recommending how owners should pay themselves. The right mix of salary, distributions, bonuses, and equity compensation can help reduce tax exposure, maintain IRS compliance, and support sustainable business growth.

Why Owner Compensation Structure Matters

Owner compensation is not simply about how much money a business owner takes home. It influences taxes, legal compliance, retirement planning, and even how lenders and investors evaluate the company.

Financial advisors and tax professionals spend considerable time helping owners determine the right compensation strategy because different business structures create different rules.

For example, according to the IRS, S-corporation owners who work in the business must pay themselves “reasonable compensation” before taking profit distributions. Failing to do so has been a common trigger for audits.

The way owners compensate themselves can affect:

- Personal income taxes

- Payroll tax exposure

- Business profitability reporting

- Retirement contributions

- Loan eligibility and financial statements

A thoughtful compensation plan balances tax efficiency with regulatory compliance and long-term financial stability.

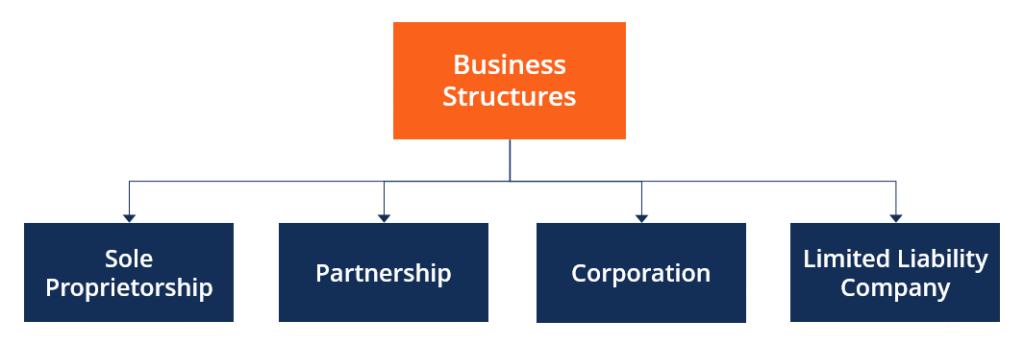

How Business Structure Shapes Compensation Decisions

One of the first questions advisors ask is: What type of entity is the business?

Each structure creates different compensation rules and tax implications.

Sole Proprietorships and Single-Member LLCs

In these structures, owners typically take owner’s draws rather than salaries. The business income flows directly to the owner’s personal tax return.

Advisors focus on managing estimated taxes and cash flow rather than structuring payroll.

However, the entire profit is usually subject to self-employment tax, which is currently 15.3% for Social Security and Medicare up to applicable thresholds.

Partnerships and Multi-Member LLCs

Partners usually receive guaranteed payments or distributions, depending on the partnership agreement.

Advisors help structure compensation so that:

- Profit allocation reflects actual work contributions

- Self-employment taxes are managed appropriately

- Cash distributions match tax liabilities

S Corporations

S corporations are where compensation planning becomes more complex.

Owners often split income between:

- Salary (subject to payroll taxes)

- Profit distributions (not subject to payroll taxes)

Because of this difference, advisors carefully determine what the IRS would consider reasonable compensation.

C Corporations

In C corporations, owner compensation is treated similarly to employee wages.

Advisors may structure compensation through:

- Salary

- Bonuses

- Dividends

- Equity incentives

Each option has different tax consequences for both the business and the owner.

Determining “Reasonable Compensation”

For S-corporation owners, determining reasonable compensation is one of the most important advisory tasks.

The IRS evaluates several factors when determining whether a salary is reasonable.

Advisors typically analyze:

- The owner’s role and responsibilities

- Time devoted to the business

- Industry salary benchmarks

- Business revenue and profitability

- Compensation paid to similar employees

For example, if a consulting firm owner generates $700,000 in revenue but reports only a $20,000 salary while taking large distributions, the IRS may question whether the salary reflects market reality.

Many advisors use compensation data from sources like:

- U.S. Bureau of Labor Statistics

- Industry compensation surveys

- Comparable company salary data

Documenting the methodology used to calculate salary helps protect the business in case of an audit.

Balancing Salary and Distributions

A common question business owners ask advisors is:

“How much should I pay myself versus take as distributions?”

The answer depends on multiple factors.

Salary increases payroll tax exposure but allows for:

- Retirement plan contributions

- Consistent income documentation

- Stronger financial records for loans

Distributions, on the other hand, are often taxed differently and may reduce payroll taxes in S-corporation structures.

Advisors typically model multiple scenarios to determine the most balanced approach.

For example:

A marketing agency owner earning $300,000 in annual profit might structure compensation as:

- $120,000 salary

- $180,000 distributions

The exact split varies depending on the industry and the owner’s role.

Cash Flow Stability and Business Health

Responsible advisors never structure compensation solely around taxes.

Cash flow stability is a critical consideration.

Owners who withdraw too much income during profitable periods may create financial strain later when revenue slows.

Advisors help owners develop compensation policies that align with business performance.

Common approaches include:

- Setting a fixed base salary for the owner

- Paying quarterly or annual profit distributions

- Creating performance-based bonuses

This approach helps keep business operations financially stable while still rewarding the owner.

Retirement Planning and Compensation

Owner compensation has a direct impact on retirement contributions.

For example, contributions to retirement plans such as 401(k)s or SEP-IRAs are often calculated based on earned income.

If an S-corporation owner keeps their salary artificially low, they may unintentionally limit how much they can contribute to retirement accounts.

Advisors frequently evaluate compensation alongside retirement planning.

A higher salary may allow for larger contributions to plans such as:

- Solo 401(k)

- Defined benefit plans

- SEP-IRAs

For many business owners, retirement contributions are a major component of long-term tax planning.

Tax Efficiency vs. Compliance Risk

Some compensation strategies look attractive from a tax perspective but create compliance risks.

Experienced advisors aim for defensible strategies, not aggressive ones.

Common red flags advisors help owners avoid include:

- Extremely low salaries in S-corporations

- Distributions that exceed available profits

- Unstructured owner withdrawals

- Mixing personal and business finances

The goal is to reduce taxes while staying clearly within regulatory guidelines.

A strategy that saves money but increases audit risk is rarely recommended.

Compensation Planning During Business Growth

Owner compensation strategies often evolve as businesses grow.

In early stages, owners may take minimal income to reinvest in the company.

As revenue increases, advisors often adjust compensation to reflect a more formal structure.

Growth stages may include:

- Transitioning from owner draws to formal payroll

- Introducing performance bonuses

- Implementing equity compensation

- Adjusting distribution strategies

Businesses seeking outside investors often formalize compensation policies to maintain transparency and governance.

Real-World Example: Compensation Strategy in Practice

Consider a technology consulting firm generating $1.2 million in annual revenue with one owner.

The advisor evaluates:

- Market salary for a technology consulting executive

- Company profitability

- Retirement planning goals

- Payroll tax exposure

The final compensation structure may look like this:

- $180,000 salary

- $300,000 profit distributions

- Annual retirement contribution through a Solo 401(k)

This approach provides:

- Reasonable IRS-defensible salary

- Tax-efficient distribution income

- Strong retirement savings

Each element supports both tax efficiency and financial planning goals.

Frequently Asked Questions

What is considered reasonable compensation for business owners?

Reasonable compensation reflects what someone would earn for performing the same role in the open market. Advisors typically use industry salary benchmarks, business profitability, and the owner’s responsibilities to determine a defensible amount.

Why do S-corporation owners take both salary and distributions?

Salary is subject to payroll taxes, while distributions are generally not. A balanced mix allows owners to meet IRS requirements while potentially improving tax efficiency.

Can an owner take only distributions and no salary?

For active S-corporation owners, the IRS generally requires reasonable compensation before taking distributions.

How often should owner compensation be reviewed?

Most advisors recommend reviewing compensation annually or whenever the business experiences significant revenue changes.

Does higher salary increase retirement contributions?

Yes. Many retirement plan contributions are based on earned income, so higher salary levels may allow larger contributions.

Are dividends a good option for business owners?

Dividends may be used in C-corporations, but they are taxed differently and do not reduce corporate taxable income.

Do lenders look at owner compensation?

Yes. Lenders often review owner salary when evaluating loan applications because it reflects consistent income.

What happens if compensation is too low?

If the IRS determines that compensation is unreasonably low, it may reclassify distributions as wages and assess back payroll taxes.

Can bonuses be used in owner compensation?

Yes. Bonuses can help align owner income with business performance while maintaining a stable base salary.

Should compensation planning involve both tax and financial advisors?

Ideally, yes. Tax professionals, financial planners, and accountants often collaborate to design balanced compensation strategies.

Crafting a Sustainable Owner Pay Strategy

Structuring owner compensation is not a one-time decision. It evolves as the business grows, tax laws change, and financial goals shift.

Experienced advisors focus on building compensation strategies that are:

- Tax-aware but compliant

- Sustainable for business cash flow

- Supportive of retirement planning

- Documented and defensible

Owners who regularly revisit compensation planning often gain greater clarity around both their personal finances and their company’s long-term financial health.

Key Insights at a Glance

- Owner compensation affects taxes, retirement planning, and compliance.

- Business structure determines how owners can legally pay themselves.

- S-corporation owners must pay reasonable salaries before distributions.

- Compensation planning should balance tax efficiency with audit risk.

- Cash flow stability is as important as tax savings.

- Retirement contributions often depend on salary levels.

- Compensation strategies should evolve as the business grows.