Summary

Portfolio decisions—such as when to sell assets, how investments are allocated, and how long securities are held—can significantly influence capital gains taxes. Understanding how tax rates apply to short-term and long-term gains, along with strategies like tax-loss harvesting and asset location, helps investors manage tax exposure while maintaining portfolio objectives. Thoughtful planning can improve after-tax returns over time.

Why Capital Gains Taxes Matter to Investors

Capital gains taxes are often overlooked during investment planning, yet they can meaningfully affect net returns. When you sell an asset such as a stock, ETF, mutual fund, or real estate investment for more than you paid, the difference is considered a capital gain. In the United States, those gains may be taxed depending on how long the asset was held and your income level.

According to the Internal Revenue Service (IRS), capital gains are generally categorized into short-term gains and long-term gains. Short-term gains apply to assets held for one year or less and are taxed as ordinary income. Long-term gains apply to assets held for more than one year and benefit from preferential tax rates.

As of recent IRS guidance, long-term capital gains tax rates typically fall into 0%, 15%, or 20%, depending on taxable income. Short-term gains, however, can be taxed at federal income tax rates that reach up to 37% for high earners.

Because of this difference, portfolio decisions—especially around holding periods, rebalancing, and asset selection—can significantly influence how much investors ultimately pay in taxes.

Understanding the Mechanics of Capital Gains

To see how portfolio decisions affect taxes, it helps to understand how capital gains are calculated.

A capital gain is the difference between:

- The purchase price (cost basis) of an asset

- The sale price when the investment is sold

For example, if an investor buys shares of an index fund for $20,000 and sells them later for $28,000, the capital gain is $8,000.

Whether that gain is taxed lightly or heavily depends on factors such as:

- How long the asset was held

- The investor’s income bracket

- Whether the investment is in a taxable or tax-advantaged account

Over time, these factors can materially influence investment outcomes. For instance, a difference of 20 percentage points in tax rate could change the net profit significantly on large gains.

Holding Period Decisions and Their Tax Impact

One of the simplest portfolio decisions with tax implications is how long to hold an investment.

If an investor sells an asset before holding it for one year, any gains are treated as short-term gains, taxed at ordinary income rates.

Holding the same asset slightly longer—just past the one-year mark—can convert those gains into long-term gains, often reducing the tax burden.

Example

Consider two investors who each earn a $10,000 gain:

- Investor A sells after 11 months

- Investor B sells after 13 months

If both are in the 32% income bracket:

- Investor A may pay about $3,200 in taxes

- Investor B may pay about $1,500 in taxes (assuming a 15% long-term capital gains rate)

A small difference in timing can therefore significantly affect the after-tax return.

This is why many financial advisors encourage investors to consider tax consequences before selling appreciated assets, particularly near the one-year threshold.

Portfolio Turnover and Tax Efficiency

Another portfolio decision that influences taxes is turnover—how frequently investments are bought and sold.

High portfolio turnover often leads to more taxable events. Active trading strategies, while potentially beneficial for some investors, may produce many short-term gains.

In contrast, lower-turnover strategies—such as long-term investing in diversified index funds—tend to produce fewer taxable sales.

For example, broad market index funds tracking benchmarks like the S&P 500 often have lower turnover compared to actively managed funds. Lower turnover generally leads to fewer realized gains distributed to investors.

This tax efficiency is one reason index funds and ETFs have become popular among long-term investors.

Tax-Loss Harvesting and Portfolio Management

Tax-loss harvesting is another portfolio decision that can influence capital gains taxes.

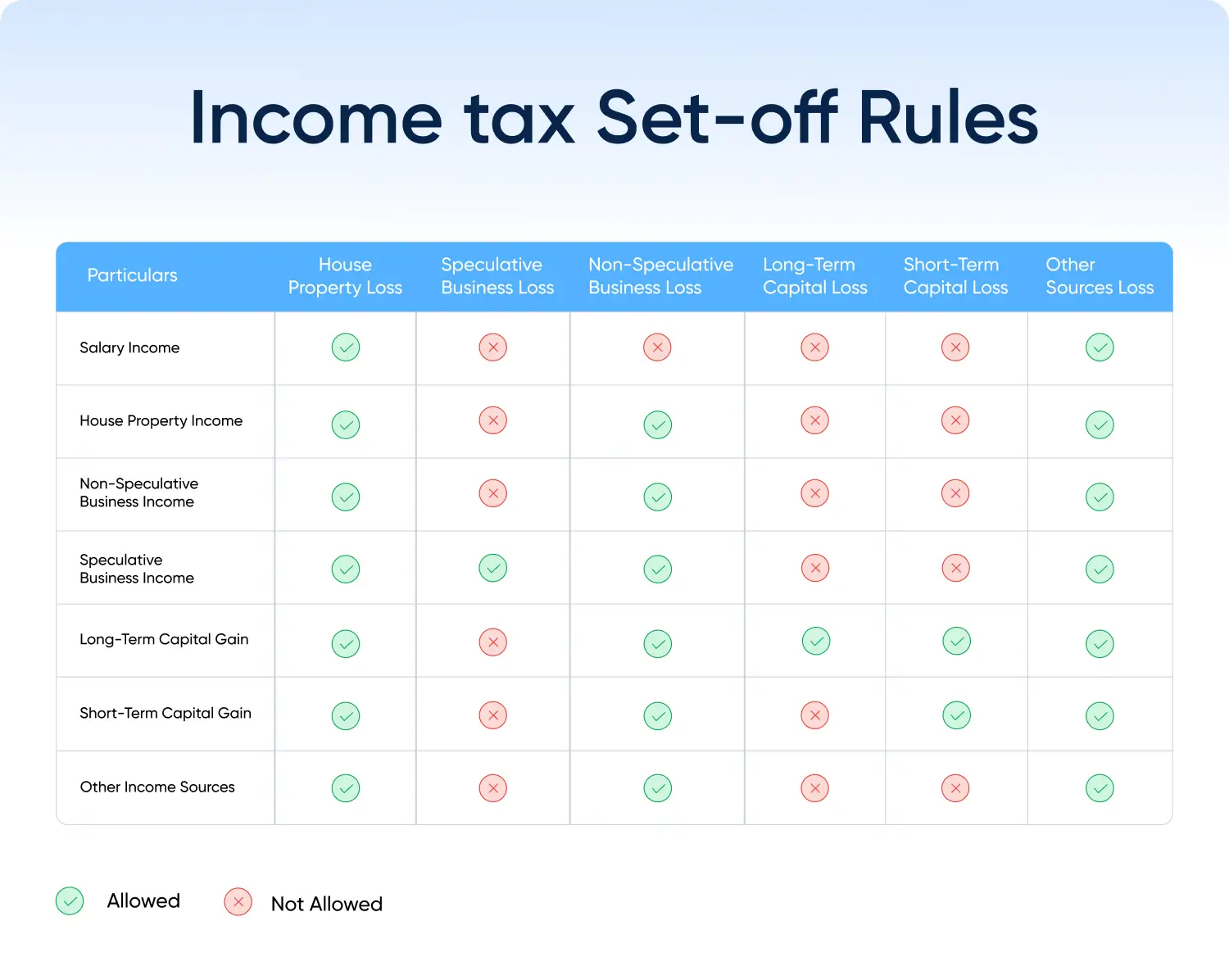

This strategy involves selling investments that have declined in value to realize a capital loss. Those losses can then be used to offset capital gains elsewhere in the portfolio.

If losses exceed gains, investors may also use up to $3,000 per year to offset ordinary income, according to IRS rules.

Practical Example

Suppose an investor sells one stock for a $10,000 gain but also sells another investment for a $6,000 loss.

The net taxable gain becomes $4,000, reducing the total tax owed.

However, tax-loss harvesting must follow certain IRS rules, including the wash-sale rule, which prevents investors from repurchasing the same or substantially identical security within 30 days of selling it at a loss.

Asset Location and Tax Efficiency

Another important portfolio decision involves where investments are held.

Investors often maintain multiple account types, such as:

- Taxable brokerage accounts

- Traditional IRAs

- Roth IRAs

- Employer-sponsored retirement plans like 401(k) plan

Strategically placing investments across these accounts can influence tax outcomes.

For instance:

- Tax-efficient investments (such as index funds or ETFs) may be suitable for taxable accounts.

- Income-generating investments (such as bonds or REITs) may be better placed in tax-advantaged accounts.

This approach is known as asset location, and it can help reduce the tax drag on a portfolio.

Rebalancing and Tax Consequences

Portfolio rebalancing—adjusting allocations back to target levels—is an important discipline in long-term investing. However, in taxable accounts, selling appreciated assets during rebalancing may trigger capital gains.

Investors often manage this issue by:

- Rebalancing with new contributions instead of selling assets

- Rebalancing inside tax-advantaged accounts where possible

- Prioritizing sales of positions with smaller gains

This approach helps maintain portfolio alignment while minimizing unnecessary tax costs.

The Role of Investment Vehicles

Different investment vehicles can affect capital gains exposure.

For example:

- Mutual funds may distribute capital gains to shareholders annually when the fund manager sells underlying securities.

- Exchange-traded funds (ETFs) often use a structure that can reduce capital gains distributions.

Because of this structure, ETFs are frequently considered more tax-efficient than many actively managed mutual funds.

That said, tax efficiency varies depending on fund management practices and investment strategy.

When Capital Gains Planning Matters Most

Capital gains planning becomes especially important during major financial events, including:

- Selling a large investment position

- Retiring and shifting from accumulation to withdrawals

- Selling a business or real estate investment

- Rebalancing a long-standing portfolio

In these situations, taxes may represent one of the largest costs investors face.

Working with a tax professional or financial advisor can help investors coordinate investment decisions with tax planning, particularly for high-value portfolios.

Frequently Asked Questions

What triggers capital gains taxes?

Capital gains taxes are triggered when an investor sells an asset for more than its purchase price in a taxable account.

Are capital gains taxes different for short-term and long-term investments?

Yes. Assets held for one year or less are taxed as ordinary income, while assets held longer than one year receive preferential long-term capital gains rates.

Do I pay capital gains taxes if I don’t sell my investments?

No. Taxes typically apply only when gains are realized, meaning the asset is sold.

Can capital losses reduce capital gains taxes?

Yes. Capital losses can offset capital gains, reducing the taxable amount.

What is tax-loss harvesting?

Tax-loss harvesting involves selling investments at a loss to offset gains elsewhere in a portfolio.

Are retirement accounts subject to capital gains taxes?

Generally no. Accounts like IRAs and 401(k)s allow investments to grow tax-deferred or tax-free depending on the account type.

How does portfolio turnover affect taxes?

Higher turnover usually creates more taxable events, potentially increasing capital gains taxes.

Are ETFs more tax efficient than mutual funds?

Often yes, because of their structure, which can reduce capital gains distributions.

What is the wash-sale rule?

The wash-sale rule disallows a loss deduction if the same or a substantially identical security is purchased within 30 days of selling it at a loss.

Should taxes drive investment decisions?

Taxes are important, but they should be considered alongside broader goals such as diversification, risk tolerance, and long-term strategy.

A Tax-Aware Approach to Portfolio Management

Portfolio decisions and tax planning are closely connected. While investment performance often receives the most attention, after-tax returns ultimately determine how much wealth investors keep.

Thoughtful decisions around holding periods, portfolio turnover, asset location, and tax-loss harvesting can help reduce unnecessary tax exposure. At the same time, tax considerations should complement—not replace—a well-diversified investment strategy aligned with long-term goals.

By understanding how capital gains taxes work and incorporating tax awareness into portfolio decisions, investors can approach financial planning with greater clarity and confidence.

Key Insights to Remember

- Capital gains taxes depend heavily on holding periods and income levels

- Long-term gains typically receive lower tax rates than short-term gains

- Portfolio turnover can increase the number of taxable events

- Strategies like tax-loss harvesting may help offset gains

- Asset location across account types can improve tax efficiency

- Rebalancing decisions should consider potential tax consequences

- ETFs often produce fewer taxable capital gains distributions than some mutual funds