Digital assets are increasingly entering mainstream investment discussions in the United States. Once limited to early cryptocurrency enthusiasts, these assets—ranging from cryptocurrencies to tokenized securities—are now being evaluated by financial advisors, institutions, and individual investors. This article explores whether digital assets are evolving into a standard portfolio component, examining adoption trends, risks, regulation, and practical considerations for long-term investors.

The Shift Toward Digital Assets in Modern Investing

Over the past decade, digital assets have evolved from a niche technological concept into a growing component of global financial markets. Initially, the conversation centered on cryptocurrencies like Bitcoin and Ethereum. Today, however, digital assets encompass a much broader category, including tokenized securities, stablecoins, and blockchain-based ownership systems.

For U.S. investors, this shift raises an important question: are digital assets becoming a routine part of diversified portfolios, similar to stocks, bonds, and real estate?

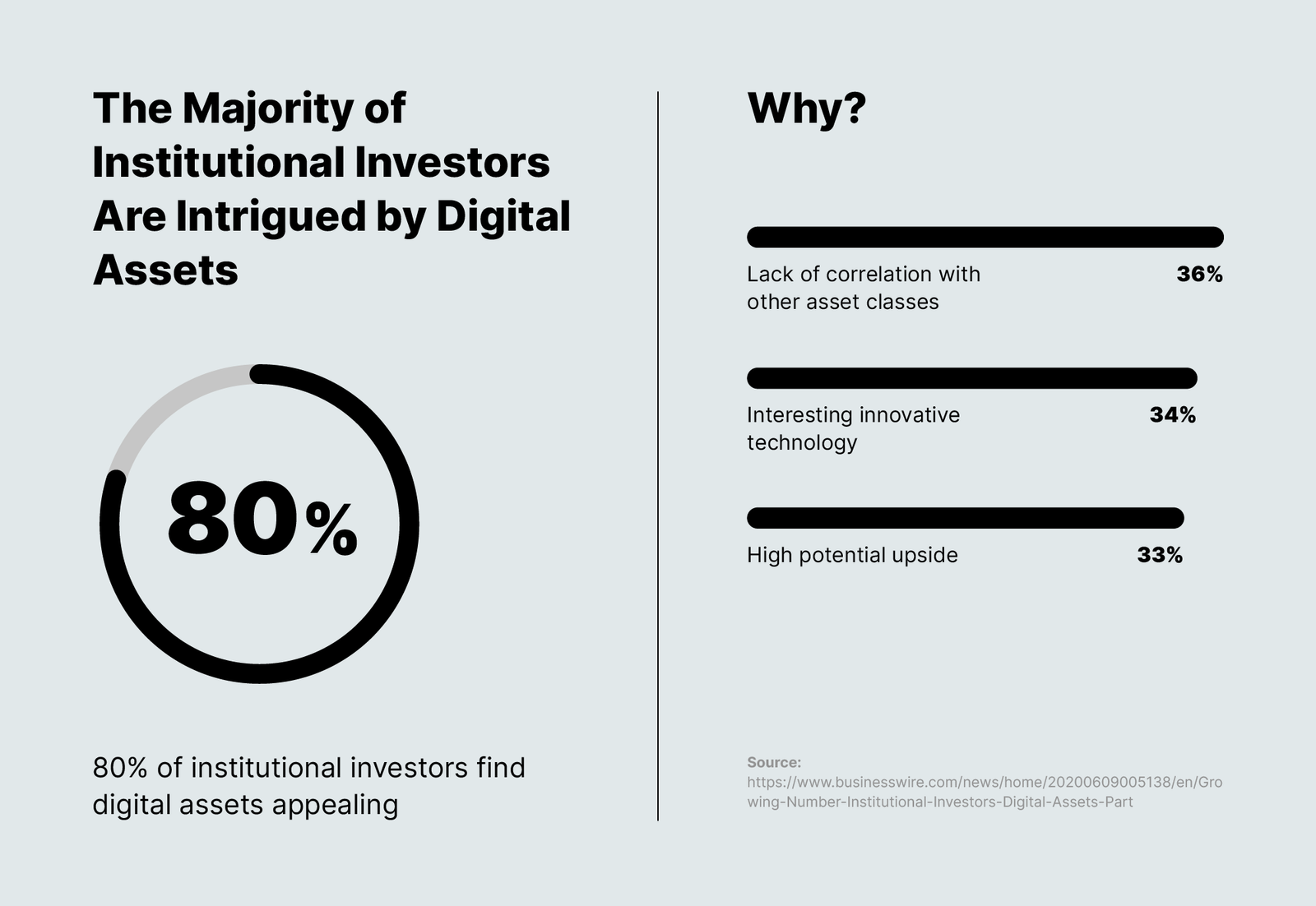

Evidence suggests that institutional participation and regulatory developments are gradually bringing digital assets closer to the mainstream. According to reports from the Pew Research Center, roughly 17% of U.S. adults reported having invested in, traded, or used cryptocurrency in recent years. Meanwhile, institutional investment firms are increasingly studying digital assets as part of broader portfolio strategies.

This growing interest is not driven solely by speculation. Instead, investors are beginning to evaluate digital assets through the same lens applied to other asset classes: diversification, long-term growth potential, and technological innovation.

Understanding What Counts as a Digital Asset

Many investors still associate digital assets exclusively with cryptocurrency. In reality, the term describes a wider range of blockchain-based assets that represent value or ownership.

Common examples include:

- Cryptocurrencies such as Bitcoin and Ethereum

- Stablecoins designed to track the value of traditional currencies

- Tokenized financial assets, including digital shares of funds or bonds

- Non-fungible tokens (NFTs) representing ownership of digital items

- Tokenized real estate and infrastructure investments

The technology underlying these assets—blockchain—creates a distributed ledger that records ownership securely and transparently.

For investors, this opens new possibilities for ownership structures that previously required complex intermediaries.

Why Investors Are Paying Attention

The rising interest in digital assets among portfolio managers and financial advisors stems from several structural factors.

1. Diversification Potential

Traditional investment portfolios often rely on asset classes such as equities, fixed income, and commodities. Digital assets may offer diversification benefits because their price movements sometimes differ from traditional markets.

Research from the CFA Institute has explored whether cryptocurrencies can improve portfolio diversification under certain conditions, particularly when used in small allocations.

However, diversification benefits can vary significantly depending on market cycles.

2. Growing Institutional Adoption

Large financial institutions are gradually entering the digital asset ecosystem. Firms like BlackRock and Fidelity Investments have launched digital asset products or custody services in recent years.

Institutional involvement often signals that an asset class is transitioning from experimental to established.

For individual investors, this institutional infrastructure can provide:

- Regulated investment products

- Improved security and custody solutions

- Greater market transparency

These developments make digital assets more accessible to investors who prefer regulated financial environments.

3. Technological Innovation in Financial Markets

Digital assets are closely tied to advances in blockchain technology. These innovations are changing how ownership records, contracts, and financial transactions are handled.

For example, smart contracts—self-executing agreements stored on blockchains—enable automated transactions without intermediaries. This concept has gained traction in areas such as decentralized finance (DeFi) and tokenized securities.

The technology itself is one reason analysts believe digital assets may remain relevant in long-term financial infrastructure.

How Advisors Are Integrating Digital Assets

Financial advisors are increasingly discussing digital assets with clients, though often cautiously.

Most advisors emphasize that digital assets should be considered only a small portion of a diversified portfolio.

Common portfolio strategies include:

- Allocating 1% to 5% of portfolio value to digital assets

- Using regulated funds or ETFs rather than direct crypto holdings

- Treating digital assets as high-risk growth investments

According to research from the Morningstar, professional advisors typically frame digital assets as satellite investments, meaning they supplement traditional core holdings rather than replace them.

Real-World Portfolio Example

Consider a hypothetical long-term investor with a diversified portfolio:

- 60% U.S. and global stocks

- 25% bonds

- 10% real estate or REITs

- 5% alternative investments

In recent years, some investors have shifted part of that “alternatives” allocation toward digital assets.

For instance, a small allocation to Bitcoin may serve as a speculative growth component, while the rest of the portfolio remains anchored in traditional investments.

The key idea is balance, not replacement.

Key Risks Investors Should Understand

Despite increasing acceptance, digital assets still carry significant risks that investors must evaluate carefully.

Market Volatility

Cryptocurrencies remain highly volatile compared with traditional assets.

Price swings of 10–20% in a single day are not unusual. This volatility makes digital assets unsuitable for investors seeking stable income or short-term financial certainty.

Regulatory Uncertainty

Digital asset regulation in the United States continues to evolve.

Government agencies such as the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission are actively developing regulatory frameworks.

Future policy decisions could affect market access, taxation, and compliance requirements.

Security and Custody Risks

Unlike traditional brokerage accounts, digital assets can involve additional security considerations.

Risks may include:

- Exchange platform failures

- Wallet security vulnerabilities

- Lost private keys

Many investors mitigate these risks by using established financial institutions that offer regulated custody solutions.

Tax Considerations for U.S. Investors

Digital assets are treated as property for tax purposes by the Internal Revenue Service.

This means:

- Capital gains taxes apply when digital assets are sold

- Crypto-to-crypto trades may trigger taxable events

- Detailed transaction records are essential

Investors should maintain accurate documentation of transactions to simplify tax reporting.

Tax treatment can vary depending on the nature of the transaction, making professional tax advice important for active traders.

Are Digital Assets Truly Becoming Mainstream?

Whether digital assets will become a permanent fixture in investment portfolios remains an open question.

However, several trends suggest growing normalization:

- Institutional investment products are expanding

- Regulatory clarity is gradually improving

- Financial advisors are increasingly discussing digital assets with clients

- Major financial firms are building blockchain infrastructure

The path toward mainstream adoption will likely be gradual rather than sudden.

Just as exchange-traded funds took decades to become common portfolio tools, digital assets may evolve slowly as markets mature and regulations stabilize.

Frequently Asked Questions

1. Are digital assets the same as cryptocurrencies?

No. Cryptocurrencies are one type of digital asset, but the category also includes tokenized securities, stablecoins, NFTs, and other blockchain-based ownership systems.

2. How much of a portfolio should be allocated to digital assets?

Many financial advisors suggest 1–5% allocations for investors who wish to include digital assets while maintaining diversification.

3. Are digital assets regulated in the United States?

Yes, though regulation is still evolving. Agencies such as the U.S. Securities and Exchange Commission oversee certain aspects of digital asset markets.

4. Can digital assets improve portfolio diversification?

Some studies suggest limited diversification benefits, but outcomes vary depending on market conditions and allocation size.

5. What are the biggest risks of investing in digital assets?

Key risks include volatility, regulatory uncertainty, cybersecurity concerns, and evolving market infrastructure.

6. Do financial advisors recommend cryptocurrency?

Some advisors discuss cryptocurrency as a small alternative investment, though recommendations depend on individual risk tolerance and financial goals.

7. Are digital assets suitable for retirement accounts?

Some retirement platforms allow digital asset exposure, but investors should carefully review fees, custody arrangements, and regulatory considerations.

8. Is blockchain technology useful beyond cryptocurrency?

Yes. Blockchain technology is being explored for supply chains, identity verification, financial settlements, and asset tokenization.

9. What is tokenization in investing?

Tokenization converts ownership rights of assets—such as real estate or securities—into blockchain-based digital tokens.

10. How can beginners start learning about digital assets?

Investors can begin by studying blockchain fundamentals, reviewing educational resources from financial institutions, and consulting financial advisors.

The Portfolio Evolution Investors Are Watching

Digital assets represent one of the most significant financial innovations of the past two decades. While they remain relatively new compared with traditional investments, their influence on financial markets is expanding.

For many investors, the key question is not whether digital assets will replace traditional investments, but how they might complement them.

As regulatory frameworks mature and institutional infrastructure strengthens, digital assets may gradually shift from experimental holdings to a recognized—though still cautious—component of diversified portfolios.

Investors who approach the space with education, discipline, and realistic expectations will be better positioned to evaluate whether digital assets belong in their long-term financial strategy.

Key Insights at a Glance

- Digital assets include cryptocurrencies, tokenized securities, NFTs, and other blockchain-based ownership systems

- Institutional firms like BlackRock and Fidelity Investments are expanding digital asset offerings

- Many advisors recommend small allocations of 1–5% for diversification

- Volatility and regulatory changes remain major considerations

- Digital assets are taxed as property by the Internal Revenue Service

- Blockchain technology may influence financial infrastructure beyond cryptocurrency