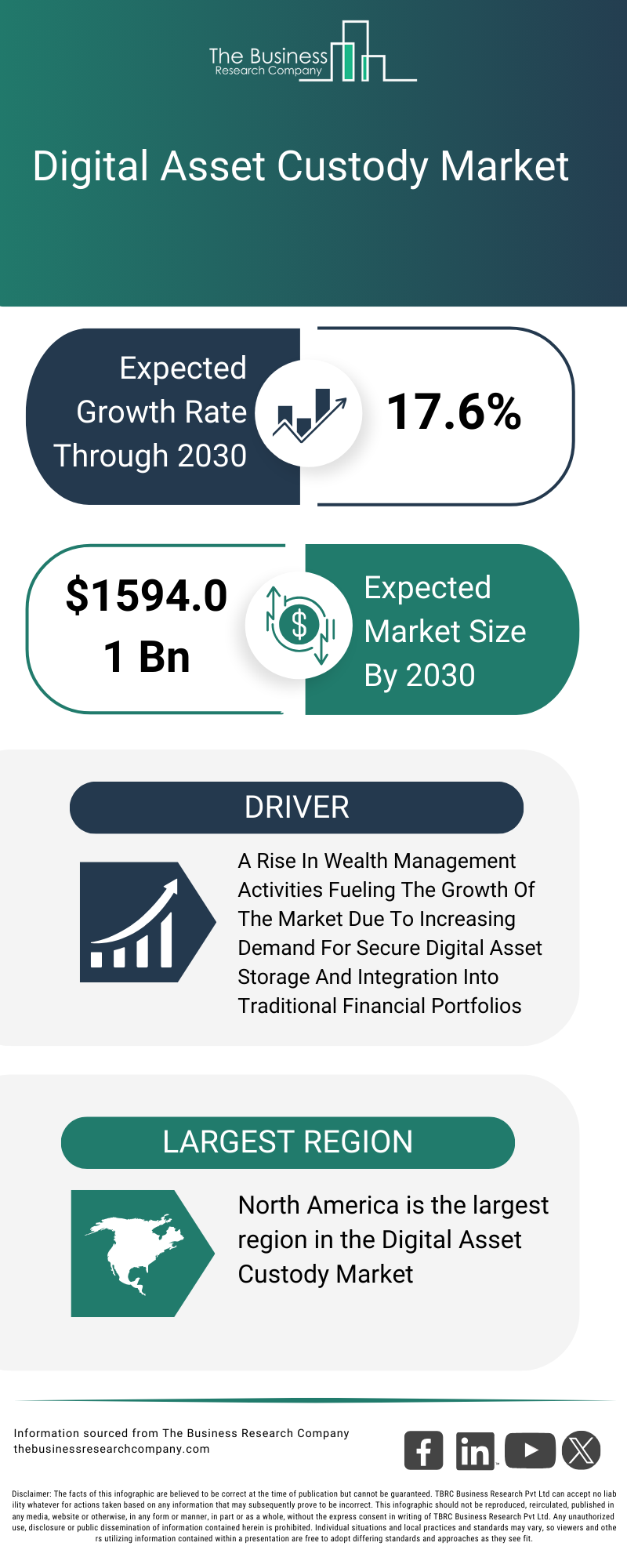

Digital asset custody has become a critical infrastructure layer for institutional participation in crypto markets. As regulatory scrutiny increases and assets like Bitcoin ETFs gain traction, banks, asset managers, and pension funds are prioritizing secure storage, compliance, insurance coverage, and operational resilience. Understanding custody models, risk controls, and regulatory expectations is essential before allocating capital to digital assets.

Why Digital Asset Custody Is Now a Strategic Priority

When institutions consider entering the crypto market, their first question is rarely about price forecasts. It is about custody.

Unlike traditional securities held through centralized depositories such as the Depository Trust & Clearing Corporation, digital assets rely on cryptographic private keys. Whoever controls the private key controls the asset. There is no reversal mechanism if a key is lost or compromised.

This fundamental difference shifts risk from intermediaries to infrastructure. For institutional investors—pension funds, endowments, insurance companies, registered investment advisers—that risk must be professionally managed.

The rapid growth of regulated products, including spot Bitcoin ETFs approved by the U.S. Securities and Exchange Commission in 2024, has further elevated custody as a board-level concern. Institutions are not simply buying crypto; they are demanding institutional-grade safeguards.

What Is Digital Asset Custody?

Digital asset custody refers to the secure storage and management of cryptographic keys that provide access to blockchain-based assets such as:

- Cryptocurrencies (e.g., Bitcoin, Ethereum)

- Tokenized securities

- Stablecoins

- Tokenized real-world assets

- Digital fund shares

Unlike retail self-custody—where an individual controls keys via hardware wallets—institutions typically rely on qualified custodians that meet regulatory and operational standards.

At its core, digital custody is about three things:

- Key protection

- Transaction authorization controls

- Regulatory compliance

But the operational depth behind those pillars is significant.

Why Institutions Cannot “Just Use a Wallet”

Retail investors often store crypto on exchanges or hardware devices. Institutional capital cannot operate that way.

Consider a $2 billion endowment evaluating a 2% allocation to Bitcoin. That $40 million exposure cannot sit in a consumer-grade wallet or lightly regulated exchange account. The institution must answer:

- Who has signing authority?

- What happens if a key holder leaves?

- Is there insurance?

- Does the custodian meet regulatory standards?

- How are assets segregated?

Boards, compliance officers, and auditors require documented control frameworks. Without them, allocations simply do not happen.

The Custody Models Institutions Evaluate

1. Self-Custody (Direct Control)

In self-custody, an institution directly manages private keys using cold storage and internal governance controls.

While this provides maximum control, it requires:

- Dedicated cybersecurity teams

- Secure physical storage facilities

- Redundant key management systems

- 24/7 monitoring capabilities

For most traditional asset managers, building this infrastructure internally is cost-prohibitive and operationally risky.

2. Third-Party Qualified Custodians

Most institutions prefer regulated third-party custodians. These firms specialize in safeguarding digital assets and typically operate under state or federal oversight.

Major players in this space include:

- Coinbase Custody

- Anchorage Digital

- BitGo

These providers offer:

- Cold storage infrastructure

- Multi-signature authorization

- SOC 1 and SOC 2 audits

- Insurance policies

- Regulatory registration

For institutions, using a qualified custodian also supports compliance with SEC custody rules for registered investment advisers.

3. Hybrid and Sub-Custody Models

Large banks increasingly offer digital asset services via partnerships. For example, global custodians may use specialized crypto firms as sub-custodians while maintaining client relationships directly.

This layered structure resembles traditional finance models but introduces additional due diligence considerations around counterparty risk.

What Institutions Actually Look For

Institutional entry is not driven by marketing materials. It is driven by risk committees and fiduciary obligations.

Here is what typically appears on an institutional due diligence checklist:

Security Architecture

- Cold storage with geographically distributed key shards

- Multi-party computation (MPC) or multi-signature authorization

- Hardware security modules (HSMs)

- Strict access control and segregation of duties

Institutions want to see documented evidence—not claims.

Regulatory Status

A custodian’s regulatory posture is often decisive.

Key considerations include:

- State trust charter or federal banking license

- Compliance with SEC custody requirements

- Anti-money laundering (AML) controls

- Know-your-customer (KYC) procedures

For example, Office of the Comptroller of the Currency guidance has clarified how nationally chartered banks may provide crypto custody services. This has increased comfort among conservative allocators.

Insurance Coverage

Insurance remains a complex topic.

Institutions typically ask:

- Is coverage crime-based or cyber-based?

- Does it cover insider threats?

- Is it full value or capped?

- Is coverage primary or excess?

While many custodians advertise insurance, coverage limits may not match large institutional allocations. This gap is often negotiated directly.

Operational Resilience

Institutions expect:

- 24/7 support

- Disaster recovery plans

- Business continuity testing

- Independent audits

Given the 24-hour nature of crypto markets, operational readiness must exceed traditional 9-to-5 finance norms.

Asset Segregation

Institutional clients typically require segregated wallets, not pooled omnibus structures. Segregation reduces legal ambiguity in bankruptcy scenarios.

This became a central issue after the collapse of FTX, where asset commingling exposed systemic weaknesses. Post-2022, segregation has become non-negotiable for many allocators.

The Role of Regulation in Shaping Custody Standards

U.S. regulation has materially shaped institutional custody adoption.

The SEC’s enforcement actions clarified that many digital assets may qualify as securities under existing frameworks. As a result, custodians must structure offerings carefully.

Meanwhile, bank regulators have provided evolving guidance around digital asset safekeeping. This regulatory dialogue has created:

- Higher entry barriers

- Clearer compliance pathways

- Stronger internal controls

For institutions, regulatory clarity reduces reputational risk.

Practical Example: A Pension Fund Allocation Scenario

Imagine a mid-sized public pension fund exploring a 1% digital asset allocation.

Before any trade occurs, the investment committee must:

- Approve custody provider selection

- Review SOC audit reports

- Confirm insurance terms

- Validate internal signatory policies

- Coordinate with external auditors

This process may take 6–12 months. The price of Bitcoin during that time is secondary to operational readiness.

Custody is not an afterthought—it is the gating mechanism.

How Custody Impacts ETFs and Funds

Many investors gained exposure to Bitcoin through ETFs rather than direct ownership. Spot ETFs rely on institutional custodians to safeguard underlying assets.

For example, ETF sponsors often partner with specialized custodians to hold Bitcoin in cold storage on behalf of shareholders. Without trusted custody infrastructure, ETF approvals would not have occurred.

This demonstrates how custody is foundational—not peripheral—to market expansion.

Common Questions Institutions Ask Before Entering Crypto

Below are frequently searched and frequently asked institutional questions:

1. Is digital asset custody regulated in the United States?

Yes, depending on structure. Custodians may operate under state trust charters, federal banking oversight, or SEC registration requirements.

2. What is a qualified custodian?

Under SEC rules, a qualified custodian is typically a bank, broker-dealer, or trust company authorized to hold client assets.

3. How are private keys protected?

Through cold storage, hardware security modules, multi-party computation, and layered authorization controls.

4. Is digital asset custody insured?

Often partially. Insurance coverage varies and may not cover full asset value.

5. What happens if a custodian goes bankrupt?

Asset segregation and trust structures are critical. Institutions require clarity on bankruptcy treatment before onboarding.

6. Can banks provide crypto custody?

Yes, subject to regulatory guidance and supervisory approval.

7. Is self-custody safer for institutions?

Generally not. Operational risk and governance complexity make third-party custody more practical.

8. How long does institutional onboarding take?

Typically several months due to compliance reviews and committee approvals.

9. Are custody fees high?

Fees vary but often range between 10–50 basis points annually, depending on services and scale.

Risks Institutions Still Monitor

Despite improvements, risks remain:

- Regulatory changes

- Cybersecurity threats

- Insider risk

- Technology obsolescence

- Cross-border compliance complexity

Institutional entry does not eliminate risk—it professionalizes its management.

Where Digital Asset Custody Is Headed

Custody is evolving toward:

- Tokenized asset support

- On-chain settlement integration

- Real-time reporting

- Collateral mobility across blockchain networks

As tokenization expands into real estate, private credit, and fund shares, custody providers must support more than cryptocurrencies.

The institutions entering today are building infrastructure for a broader digital asset ecosystem.

The Institutional Turning Point

Digital asset markets have matured beyond speculative retail trading. Institutional participation now depends less on price volatility and more on governance frameworks.

Custody sits at the center of that transition.

When institutions evaluate digital assets, they are not asking whether blockchain will survive. They are asking whether operational safeguards meet fiduciary standards.

That shift marks the market’s structural evolution.

Key Insights at a Glance

Security architecture matters more than marketing claims

Digital asset custody is foundational to institutional crypto adoption

Qualified custodians must meet strict regulatory and audit standards

Insurance coverage varies and requires careful review

Asset segregation is now essential

Institutional onboarding can take months due to compliance

Custody infrastructure enables ETFs and tokenized asset growth

Regulation has raised standards but increased clarity