Summary

Industrial development in secondary U.S. cities is accelerating as companies search for lower costs, stronger labor markets, and better logistics access than crowded major metros. Regions like Columbus, Greenville, and Tulsa are attracting manufacturing, distribution, and technology investment. For businesses, investors, and local governments, these cities offer scalable infrastructure, supportive policy environments, and room for long-term industrial growth.

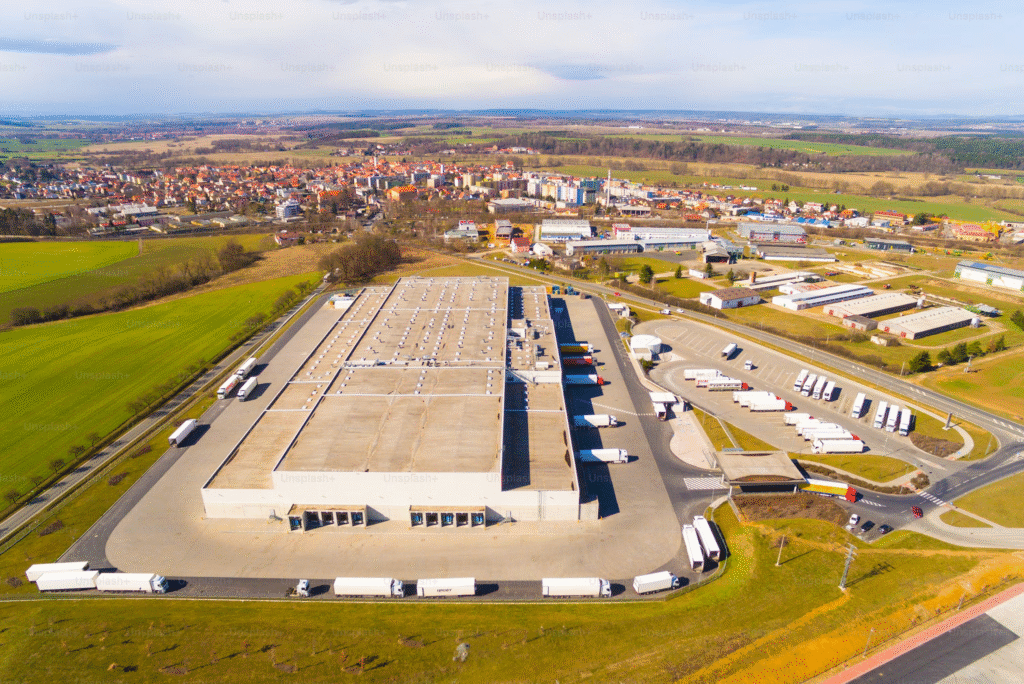

The Shift Away from Major Metro Industrial Hubs

For decades, American industrial development clustered around the nation’s largest metropolitan areas—Los Angeles, Chicago, Houston, and New York. These cities offered ports, rail access, large labor pools, and financial capital. However, over the past fifteen years, a quiet shift has been unfolding across the United States.

Companies are increasingly turning to secondary cities—mid-sized metropolitan areas typically ranging from 250,000 to 1.5 million residents—for new industrial investments. These locations offer strategic advantages that are becoming more valuable in the modern economy.

The change is not accidental. Rising land costs, congestion, regulatory complexity, and labor competition in major metros have made expansion there more challenging. At the same time, infrastructure improvements, interstate logistics networks, and regional economic development strategies have made smaller cities far more competitive.

Industrial real estate analysts and site-selection consultants increasingly describe these cities as the “next frontier of U.S. manufacturing and logistics growth.”

What Defines a Secondary Industrial City?

A secondary city is not simply a smaller market. Many have strong regional influence and highly specialized industrial economies.

Typical characteristics include:

- Population between 250,000 and 1.5 million

- Strategic location near interstate or rail corridors

- Lower industrial land costs

- Competitive tax incentives for employers

- Access to technical workforce pipelines

- Less congestion and faster permitting

Examples of frequently cited secondary industrial cities include:

- Columbus, Ohio

- Greenville, South Carolina

- Tulsa, Oklahoma

- Des Moines, Iowa

- Boise, Idaho

- Chattanooga, Tennessee

- Reno, Nevada

These cities are often located within one-day truck delivery of major population centers, a critical factor for modern supply chains.

Why Industrial Companies Are Choosing Secondary Cities

Several structural trends are driving the relocation of industrial investment toward these markets.

1. Lower Land and Development Costs

Industrial developers consistently cite land pricing as one of the biggest advantages of secondary cities.

Industrial land in major markets such as Southern California or Northern New Jersey can exceed $1–3 million per acre. In contrast, comparable industrial land in mid-sized cities may range from $50,000 to $250,000 per acre depending on location.

This cost difference allows companies to:

- Build larger distribution centers

- Design flexible manufacturing campuses

- Reserve land for future expansion

For long-term industrial projects, the savings can be substantial.

2. Access to Stable Labor Markets

Labor shortages are a major concern in many large industrial hubs. Secondary cities often offer a more stable workforce with lower turnover.

Several factors contribute to this advantage:

- Lower cost of living attracts workers

- Strong community college technical programs

- Less competition from other employers

- High retention rates

For example, workforce participation in many midwestern and southern secondary cities remains higher than in several major coastal metros.

Industrial employers also report that employee commute times are significantly shorter, improving attendance and productivity.

3. Strategic Logistics Positioning

Modern distribution networks prioritize speed and geographic coverage.

Secondary cities frequently sit at the crossroads of interstate transportation corridors. This allows companies to reach major markets efficiently without operating directly inside them.

Examples include:

- Columbus, Ohio – within a one-day drive of 60% of the U.S. population

- Memphis, Tennessee – major rail, air cargo, and interstate hub

- Kansas City, Missouri – central freight and rail interchange

Logistics planners often refer to these regions as “inland distribution hubs.”

4. Faster Permitting and Development Timelines

Large metropolitan areas often face long zoning approvals and environmental review processes. Secondary cities tend to offer faster development timelines.

Many municipalities actively compete for industrial investment by providing:

- Dedicated economic development teams

- Pre-approved industrial zoning districts

- Infrastructure-ready business parks

- Tax increment financing or incentives

These policies can reduce development timelines by six months to two years compared with larger urban markets.

Industrial Sectors Expanding in Secondary Cities

Industrial development in these regions is not limited to traditional manufacturing. Several modern sectors are driving investment.

Advanced Manufacturing

Secondary cities have become major locations for advanced manufacturing, particularly in:

- Automotive components

- Aerospace parts

- robotics manufacturing

- semiconductor supply chains

Southern cities such as Greenville and Huntsville have become major aerospace and automotive production centers due to workforce training programs and state incentives.

Logistics and Distribution

E-commerce growth has dramatically expanded demand for distribution space.

Warehouse and fulfillment centers now require:

- Large footprints

- highway connectivity

- proximity to regional population centers

Secondary cities often provide the perfect combination of affordable land and transportation access.

For example, distribution clusters have rapidly grown around cities such as:

- Indianapolis

- Louisville

- Reno

These markets allow companies to ship goods quickly while avoiding the congestion of coastal ports.

Food Processing and Agricultural Manufacturing

Midwestern and southern secondary cities also attract food processing facilities due to proximity to agricultural production.

Companies benefit from:

- Reduced transportation costs for raw materials

- access to cold-storage logistics

- rural workforce availability

Regions across Iowa, Nebraska, Arkansas, and Kansas continue to see strong investment in this sector.

Real-World Examples of Industrial Growth

The shift toward secondary cities is not theoretical—it is already visible in several high-profile development patterns across the United States.

Columbus, Ohio

Columbus has emerged as one of the fastest-growing industrial hubs in the Midwest.

Key advantages include:

- central geographic location

- strong logistics infrastructure

- multiple interstate connections

Recent semiconductor investment announcements have accelerated industrial construction and supplier ecosystems across the region.

Greenville–Spartanburg, South Carolina

This region has transformed into a major manufacturing corridor.

Industrial growth has been fueled by:

- automotive production clusters

- aerospace manufacturing

- international investment

The area also benefits from proximity to the Port of Charleston, allowing manufacturers to access global shipping routes.

Reno, Nevada

Reno has developed into a technology and logistics hub serving the West Coast.

Companies choose Reno because it offers:

- lower taxes than California

- access to Interstate 80

- proximity to the Bay Area

Large manufacturing and distribution facilities have expanded rapidly throughout the Reno–Tahoe Industrial Center.

Infrastructure Investments Supporting Growth

Secondary cities are increasingly investing in infrastructure to support industrial development.

Key improvements include:

- freight rail modernization

- expanded intermodal terminals

- highway upgrades

- regional airports supporting cargo

The Infrastructure Investment and Jobs Act has accelerated funding for many of these projects.

Public infrastructure improvements significantly reduce the risk for private industrial investors.

Challenges Secondary Cities Must Manage

Despite strong growth potential, secondary cities also face challenges as industrial expansion accelerates.

Workforce Development

Growing industrial clusters can create labor shortages if workforce training does not keep pace.

Cities must continue investing in:

- technical education programs

- trade apprenticeships

- workforce housing

Industrial Land Availability

Rapid development can quickly consume available industrial land.

Many cities are responding by:

- expanding industrial zoning districts

- building new logistics parks

- redeveloping underused industrial corridors

Infrastructure Strain

As freight traffic increases, transportation infrastructure must keep up.

Without careful planning, cities risk:

- traffic congestion

- supply chain delays

- higher logistics costs

Long-term regional planning is essential.

Opportunities for Investors and Developers

Industrial developers and institutional investors increasingly view secondary cities as attractive long-term opportunities.

Advantages include:

- higher industrial cap rates compared with coastal markets

- stronger land appreciation potential

- less competition for development sites

- growing tenant demand

Many investment firms now specifically target “Tier-2 industrial markets” as part of national portfolio strategies.

These markets also offer opportunities for:

- build-to-suit facilities

- logistics parks

- advanced manufacturing campuses

For investors willing to study local labor and infrastructure dynamics, secondary cities can provide strong risk-adjusted returns.

The Role of Local Governments and Economic Development Agencies

Economic development organizations play a major role in shaping industrial growth.

Successful cities typically focus on several strategies:

- creating shovel-ready industrial sites

- developing workforce training partnerships

- improving logistics infrastructure

- offering predictable regulatory processes

Collaboration between local governments, universities, and private developers is often the key to long-term success.

Cities that build these partnerships tend to attract more sustainable industrial investment.

Frequently Asked Questions

What is considered a secondary city in the U.S.?

A secondary city generally refers to a mid-sized metropolitan area with a population between roughly 250,000 and 1.5 million residents that serves as a regional economic hub but is not one of the largest U.S. metros.

Why are companies moving industrial facilities to smaller cities?

Companies seek lower land costs, faster development approvals, access to stable labor markets, and improved logistics positioning compared with major metropolitan areas.

Are secondary cities good locations for distribution centers?

Yes. Many secondary cities sit near interstate corridors and allow companies to reach major population centers within one or two days of truck travel.

Which industries are expanding the fastest in secondary cities?

Advanced manufacturing, logistics distribution, aerospace manufacturing, food processing, and supply-chain technology sectors are among the fastest-growing.

Do secondary cities offer tax incentives for manufacturers?

Many do. State and local governments frequently provide tax credits, infrastructure grants, workforce training support, and property tax abatements to attract industrial investment.

Are industrial real estate returns higher in smaller markets?

Industrial cap rates in secondary markets are often higher than in primary coastal cities, which can provide attractive returns for investors.

What workforce advantages do secondary cities provide?

Lower cost of living, lower turnover rates, and strong community college technical training programs often create stable industrial workforces.

How do logistics networks support these cities?

Interstate highways, rail intermodal terminals, and regional airports allow companies to ship goods efficiently across the country.

What risks exist when developing in secondary markets?

Potential risks include smaller labor pools, infrastructure limitations, and slower population growth compared with major metros.

Are secondary cities likely to continue growing industrially?

Most analysts believe so. Supply chain diversification, domestic manufacturing investment, and infrastructure improvements continue to support growth in these markets.

A New Geography of American Industry

Industrial development in the United States is entering a new phase defined not by a few dominant mega-cities, but by a network of capable regional centers. Secondary cities are proving that strong logistics positioning, workforce readiness, and thoughtful planning can rival traditional industrial hubs.

For businesses and investors willing to look beyond the largest metros, these cities offer space to grow, communities eager for investment, and the infrastructure needed for modern manufacturing and distribution.

Key Insights from the Secondary City Industrial Shift

- Industrial development is increasingly moving toward mid-sized regional cities

- Lower land and construction costs drive many corporate decisions

- Logistics access within one-day trucking distance is a major advantage

- Workforce stability and lower turnover attract manufacturers

- Infrastructure investment continues to strengthen secondary markets

- Industrial real estate investors are increasingly targeting Tier-2 cities