Summary

Professionals in their highest earning years face unique tax challenges—from managing higher marginal tax rates to optimizing retirement savings, investments, and deductions. Understanding strategic tax planning can significantly reduce lifetime tax burdens. This guide explains practical tax considerations for high-income professionals, including retirement planning, tax-efficient investing, business deductions, and estate planning strategies relevant to U.S. taxpayers.

Key Tax Considerations for Professionals in Peak Earning Years

For many professionals, the years between roughly ages 35 and 55 represent the period of highest income growth. Promotions, equity compensation, profitable businesses, and peak productivity often coincide during this stage.

While higher income provides financial opportunity, it also introduces more complex tax exposure. Federal marginal rates increase, investment income becomes taxable, and additional taxes—such as the Net Investment Income Tax (NIIT)—may apply.

According to the IRS, the top federal income tax bracket currently reaches 37%, and professionals earning well into six figures can quickly find themselves paying substantial taxes without proactive planning.

Understanding the key tax considerations during peak earning years allows professionals to:

- Reduce lifetime tax liability

- Optimize retirement savings

- Preserve investment returns

- Improve long-term wealth accumulation

This article explores the tax planning strategies that experienced financial advisors frequently recommend to high-income professionals in the United States.

Why Peak Earning Years Require Strategic Tax Planning

During early career stages, tax planning is relatively simple. Income is lower, deductions are straightforward, and investment portfolios are still developing.

Peak earning years change the equation.

Several factors contribute to increased tax complexity:

- Higher marginal income tax brackets

- Multiple income streams (salary, investments, business income)

- Stock compensation or bonuses

- Greater exposure to capital gains taxes

- Increased eligibility for phase-outs and surtaxes

For example, a physician earning $450,000 annually may face federal income tax, state income tax, Medicare surtaxes, and taxes on investment income. Without careful planning, the combined tax burden can exceed 40–45% of income depending on location.

Strategic tax planning helps professionals keep more of what they earn while complying fully with U.S. tax laws.

Maximizing Retirement Contributions for Immediate Tax Relief

One of the most effective ways to reduce taxable income during peak earning years is maximizing tax-advantaged retirement contributions.

Many professionals underestimate how powerful these accounts can be when used consistently.

Common options include:

- 401(k) or 403(b) plans

- Backdoor Roth IRA strategies

- Health Savings Accounts (HSAs)

- Defined benefit or cash balance plans for business owners

In 2024, the IRS allows employees to contribute up to $23,000 annually to a 401(k), with additional catch-up contributions available for those age 50 and older.

A professional earning $350,000 who contributes the maximum amount can reduce taxable income by tens of thousands of dollars each year.

Additional strategies include:

- Employer matching contributions

- Mega backdoor Roth conversions

- Deferred compensation plans

For self-employed professionals, retirement planning opportunities can be even larger. A cash balance pension plan, for example, may allow contributions exceeding $100,000 annually, significantly reducing taxable income.

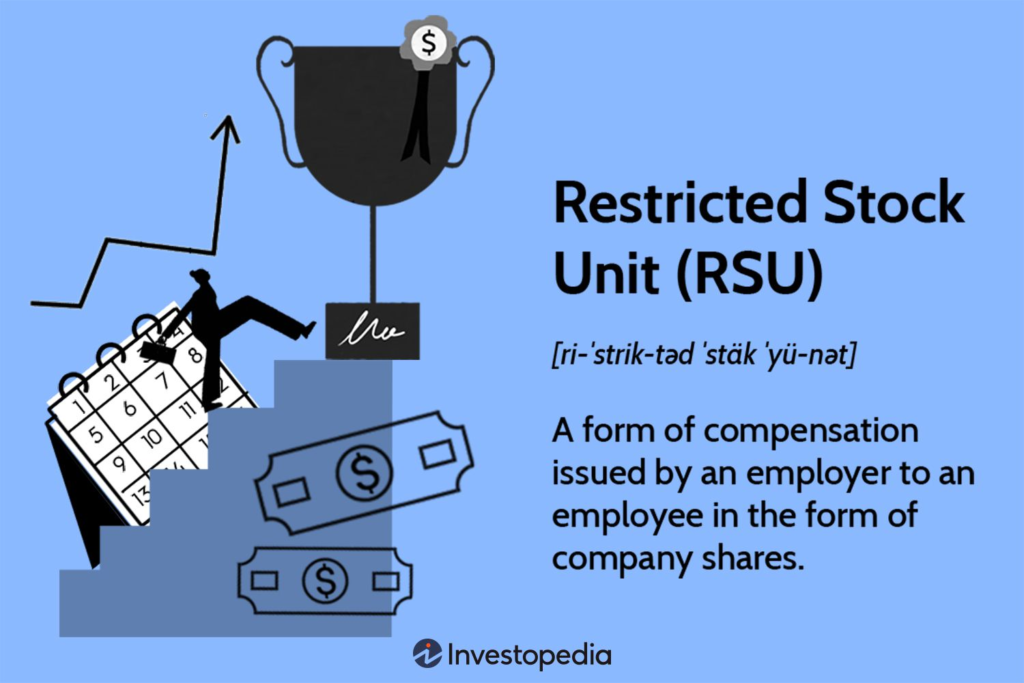

Managing Equity Compensation and Stock Options

Many professionals—particularly in technology, finance, and startups—receive compensation in the form of equity.

Common types include:

- Restricted Stock Units (RSUs)

- Incentive Stock Options (ISOs)

- Non-Qualified Stock Options (NSOs)

- Employee Stock Purchase Plans (ESPPs)

Each has different tax implications.

For example:

RSUs are taxed as ordinary income when they vest.

ISOs may qualify for capital gains treatment if holding requirements are met.

NSOs are typically taxed at exercise.

A senior engineer receiving $150,000 in RSUs annually may experience significant income spikes when shares vest. Without planning, this can push total income into higher tax brackets.

Professionals often use strategies such as:

- Timing option exercises strategically

- Selling shares to cover taxes immediately

- Diversifying concentrated stock positions

- Planning around Alternative Minimum Tax (AMT)

Working with a tax advisor is particularly valuable when equity compensation represents a large portion of income.

Understanding the Net Investment Income Tax (NIIT)

High-income professionals frequently encounter the Net Investment Income Tax, a 3.8% surtax applied to certain investment income.

This tax generally applies when modified adjusted gross income exceeds:

- $200,000 for single filers

- $250,000 for married couples filing jointly

Income subject to NIIT includes:

- Capital gains

- Dividends

- Interest income

- Rental income

- Passive business income

For example, a married couple earning $300,000 in wages and realizing $100,000 in capital gains could owe an additional $3,800 in NIIT.

Tax planning techniques may include:

- Tax-loss harvesting

- Municipal bond allocations

- Strategic timing of asset sales

- Charitable giving strategies

Managing investment taxes becomes increasingly important as portfolios grow.

Tax-Efficient Investing Strategies

Investment decisions can significantly affect tax outcomes.

While many investors focus solely on returns, experienced professionals also evaluate after-tax performance.

Tax-efficient investing often involves:

- Placing tax-inefficient assets in retirement accounts

- Holding broad index funds in taxable accounts

- Minimizing unnecessary trading

- Harvesting losses during market downturns

For example, actively traded mutual funds may generate annual capital gains distributions even if the investor does not sell shares. Index funds and ETFs typically produce fewer taxable events.

Financial planners often refer to this as asset location strategy—placing investments in accounts where they receive the most favorable tax treatment.

Charitable Giving as a Tax Strategy

Charitable giving can provide both philanthropic impact and meaningful tax benefits.

Professionals who donate regularly may benefit from structured giving strategies.

Popular options include:

- Donor-Advised Funds (DAFs)

- Qualified Charitable Distributions (QCDs)

- Charitable remainder trusts

A donor-advised fund allows a taxpayer to contribute assets—such as appreciated stock—and receive an immediate tax deduction, while distributing donations to charities over time.

For instance, donating $50,000 in appreciated stock instead of cash can avoid capital gains tax while providing a full charitable deduction.

This strategy is particularly useful during years with unusually high income.

Business Owners: Deduction and Entity Planning

Professionals who operate businesses—consultants, physicians, attorneys, or entrepreneurs—have additional tax planning opportunities.

Key considerations include:

- Choosing the right business entity

- Maximizing business deductions

- Taking advantage of the Qualified Business Income (QBI) deduction

- Managing payroll versus distributions

The QBI deduction may allow eligible businesses to deduct up to 20% of qualified income, although eligibility depends on income levels and profession type.

Business owners can also deduct expenses such as:

- Office rent

- Equipment purchases

- Professional services

- Health insurance premiums

However, documentation and compliance are essential to avoid audit issues.

Planning for Capital Gains and Asset Sales

Peak earning years often coincide with major financial events:

- Selling a business

- Liquidating investment properties

- Exercising stock options

- Rebalancing portfolios

Each of these events can trigger significant capital gains taxes.

The long-term capital gains tax rate typically ranges from:

- 0%

- 15%

- 20%

High earners may also pay the 3.8% NIIT, raising the effective rate.

Planning ahead can reduce the tax impact. Strategies may include:

- Spreading sales across multiple years

- Using charitable contributions of appreciated assets

- Leveraging opportunity zone investments

- Offset gains with capital losses

A well-timed strategy can save tens of thousands of dollars in taxes.

Estate and Gift Tax Planning During High-Income Years

Peak earning years are also an ideal time to consider long-term wealth transfer strategies.

The federal estate tax exemption is historically high—over $13 million per individual—but current law could reduce this threshold in the coming years.

Professionals with growing wealth may benefit from:

- Annual gift exclusions

- Irrevocable trusts

- Family limited partnerships

- Strategic wealth transfers

Early planning can reduce future estate taxes while preserving family wealth.

Working with Tax and Financial Professionals

Tax planning at higher income levels often requires coordinated advice.

Many professionals benefit from working with:

- Certified Public Accountants (CPAs)

- Financial planners

- Tax attorneys

- Estate planning specialists

The goal is not simply filing an annual return but designing a long-term tax strategy.

Coordinated planning can align investments, retirement savings, charitable giving, and estate planning into a unified financial strategy.

Frequently Asked Questions

What income level requires advanced tax planning?

Many professionals begin needing structured tax planning once income exceeds $200,000 to $300,000 annually, especially if multiple income sources exist.

What tax bracket do high-income professionals usually fall into?

The highest federal bracket is 37%, though effective rates vary based on deductions, credits, and state taxes.

Are Roth conversions useful during peak earning years?

They can be, but often make more sense during lower-income periods unless future tax rates are expected to rise significantly.

What is the biggest tax mistake high earners make?

Failing to plan throughout the year. Many only review taxes during filing season, when fewer strategies remain available.

How does the Net Investment Income Tax work?

It adds a 3.8% tax on certain investment income when income exceeds specific thresholds.

Should professionals prioritize tax reduction or investment growth?

Both matter. Tax efficiency enhances long-term investment returns without increasing risk.

Can charitable donations reduce high-income taxes significantly?

Yes, particularly when donating appreciated assets or using donor-advised funds.

Are tax strategies different for business owners?

Yes. Business owners have additional deductions, retirement plan options, and entity planning strategies.

When should professionals start estate planning?

Ideally during peak earning years, when wealth accumulation accelerates.

How often should tax strategies be reviewed?

At least annually, and ideally whenever major financial events occur.

Building a Tax Strategy That Supports Long-Term Wealth

Peak earning years present tremendous opportunities—not only to generate income but to build lasting financial security.

However, without careful tax planning, professionals may lose a substantial portion of their earnings to avoidable taxes.

By maximizing retirement accounts, investing tax-efficiently, planning for capital gains, and coordinating with experienced advisors, professionals can transform high income into long-term wealth.

The most effective strategies focus on lifetime tax optimization, not simply minimizing taxes in a single year.

Key Lessons for High-Income Professionals

- Peak earning years often bring the highest tax exposure

- Retirement contributions remain one of the most powerful tax tools

- Equity compensation requires careful planning

- Investment taxes can significantly reduce returns

- Charitable strategies can provide both tax and philanthropic benefits

- Business owners have additional tax planning opportunities

- Estate planning becomes increasingly important as wealth grows