Summary

Managing taxes with multiple income streams requires more than basic filing. This guide explains how U.S. taxpayers can coordinate withholding, estimated payments, deductions, and recordkeeping across W-2, 1099, investment, and business income. Learn practical strategies to reduce surprises, stay compliant, and make informed decisions as income complexity grows.

Understanding Why Multiple Income Sources Change the Tax Equation

Earning income from more than one source is increasingly common in the U.S. Salaries combined with freelance work, rental income, investment distributions, or small business revenue can create financial flexibility—but also tax complexity. Each income type is treated differently under the tax code, and when they intersect, the impact on your total tax liability can be significant.

The challenge is rarely about finding loopholes. Instead, it’s about coordination. When income streams aren’t managed together, taxpayers often under-withhold, miss deductions, or trigger unexpected taxes at filing time. According to data from the Internal Revenue Service, underpayment penalties are among the most common issues for taxpayers with mixed W-2 and 1099 income.

The goal of effective tax strategy is not just to minimize taxes, but to create predictability, avoid penalties, and align tax decisions with broader financial goals.

Common Types of Multiple Income Streams—and How They’re Taxed

Before building a strategy, it’s essential to understand how different income sources are taxed.

Employment (W-2) Income

Wages are subject to automatic withholding for federal income tax, Social Security, and Medicare. This withholding often gives taxpayers a false sense of security when additional income exists elsewhere.

Independent Contractor or Side Business Income (1099)

Freelance, consulting, and gig work are typically reported on Form 1099-NEC. No taxes are withheld, and the income is subject to self-employment tax, which covers both the employer and employee portions of Social Security and Medicare.

Investment Income

Dividends, interest, and capital gains may be taxed at ordinary income rates or preferential rates, depending on the holding period and investment type. Timing and asset placement matter here.

Rental and Pass-Through Income

Rental properties and pass-through business entities (such as LLCs or S corporations) introduce depreciation, passive activity rules, and more nuanced reporting requirements.

Each stream behaves differently, but they all converge on your total adjusted gross income (AGI), which affects deductions, credits, Medicare premiums, and phaseouts.

The Withholding Trap: Why Paychecks Alone Aren’t Enough

One of the most common mistakes is relying solely on W-2 withholding when additional income exists. Payroll systems don’t know about your side business or investments, so they withhold based only on your job.

A practical solution is to proactively adjust withholding using Form W-4 or make quarterly estimated tax payments. Many taxpayers prefer adjusting withholding because it feels simpler and avoids writing quarterly checks. Others prefer estimates for flexibility and clearer tracking.

The key is recalculating total expected income at least once a year—and ideally midyear—to avoid a shortfall.

Estimated Taxes: When and How to Use Them Properly

If you earn income without withholding, the IRS generally expects quarterly estimated payments. These are due in April, June, September, and January.

Estimated taxes are especially important when:

- Side income exceeds a few thousand dollars

- Investment gains fluctuate significantly

- Rental or business income varies seasonally

A commonly used safe harbor is paying either 90% of the current year’s tax liability or 100% (110% for higher earners) of the prior year’s tax. This approach reduces penalty risk even if income fluctuates.

Coordinating Deductions Across Income Streams

Multiple income sources often unlock more deductions—but only if tracked carefully.

Self-employed taxpayers may deduct ordinary and necessary business expenses, including:

- Home office costs (when qualified)

- Business mileage or vehicle expenses

- Software, education, and professional services

Meanwhile, investment and rental income may allow depreciation, interest deductions, and operating expenses. The challenge is ensuring expenses are properly allocated and documented, especially when assets serve dual purposes.

Poor documentation is one of the most common reasons deductions fail under audit scrutiny.

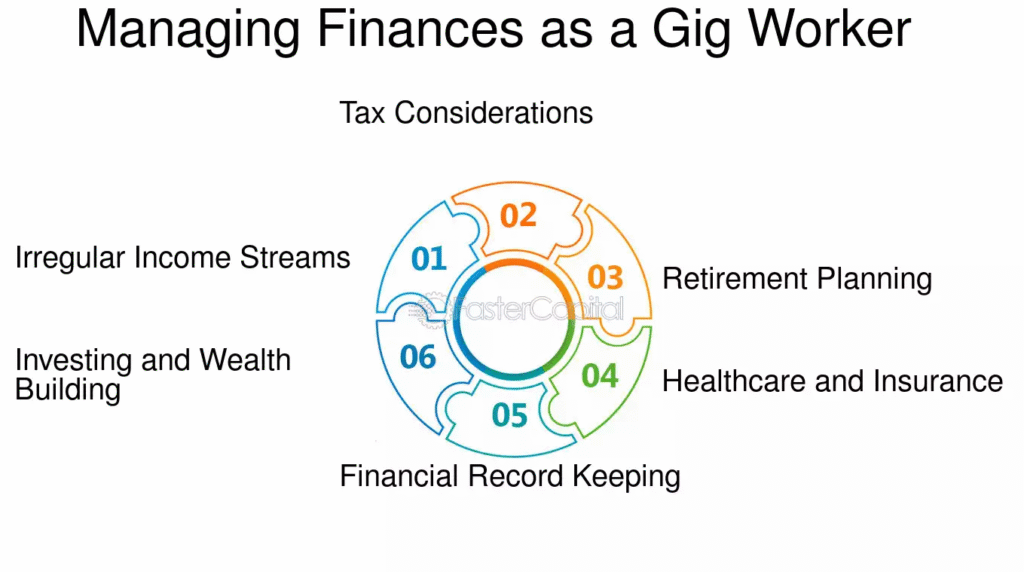

Retirement Contributions as a Strategic Tool

Retirement accounts are one of the most effective—and underused—tools for managing taxes across income streams.

People with side income may qualify for:

- Solo 401(k) plans

- SEP IRAs

- Traditional IRAs (subject to income limits)

These accounts can reduce taxable income while supporting long-term savings. According to the Bureau of Labor Statistics, households with diversified income sources are more likely to experience income volatility—making tax-deferred savings even more valuable.

Strategic contributions can also help manage AGI thresholds tied to credits and deductions.

The Importance of Timing Income and Expenses

Timing matters more when income is variable. Accelerating expenses or deferring income—within legal limits—can smooth taxable income across years.

Examples include:

- Invoicing timing for freelance work

- Capital gain realization planning

- Equipment purchases for business deductions

These decisions are most effective when made before year-end, not during tax filing season.

Recordkeeping Systems That Actually Work

Multiple income streams require more than a shoebox of receipts. A reliable system reduces errors and stress.

Effective systems typically include:

- Separate bank accounts for business income

- Monthly reconciliation of income and expenses

- Digital storage for receipts and statements

Good records don’t just support deductions—they enable better decision-making throughout the year.

When Professional Guidance Makes Sense

As income complexity increases, the value of professional tax advice often outweighs the cost. This is especially true when:

- Income exceeds six figures

- Business structures are involved

- State and local tax issues arise

- Investment activity increases

A qualified tax professional can help model scenarios, identify overlooked risks, and ensure compliance across all income streams.

Frequently Asked Questions

Do I need to pay estimated taxes if I already have a W-2 job?

Yes, if additional income isn’t covered by withholding and results in a tax balance due.

How much side income triggers estimated tax requirements?

There’s no fixed threshold, but owing $1,000 or more at filing usually triggers the requirement.

Can I deduct losses from one income source against another?

Sometimes. Passive activity and at-risk rules may limit how losses offset other income.

Is self-employment tax separate from income tax?

Yes. It covers Social Security and Medicare and is calculated in addition to income tax.

Should I form an LLC for tax reasons alone?

Not necessarily. Entity choice should consider liability, administrative burden, and tax impact together.

How do investment gains affect my overall tax rate?

They increase AGI and may push other income into higher brackets or reduce deductions.

What records should I keep for multiple income sources?

Income statements, expense receipts, mileage logs, bank statements, and tax forms.

Can tax software handle multiple income streams?

Yes, but accuracy depends on proper data entry and understanding of tax rules.

When should I talk to a tax professional?

When income sources increase, fluctuate significantly, or involve business or real estate activity.

Navigating Complexity Without Overpaying

Managing taxes across multiple income sources is less about aggressive tactics and more about coordination, foresight, and discipline. When income streams are viewed together rather than in isolation, tax planning becomes a proactive process instead of a reactive one. The payoff is fewer surprises, better cash flow management, and decisions that support both compliance and long-term financial stability.

Key Points to Keep in Perspective

- Multiple income streams interact at the AGI level

- Withholding often needs adjustment

- Estimated taxes prevent penalties

- Timing and documentation matter

- Professional advice scales with complexity