Summary

Selling an investment can trigger significant tax consequences. Investors often review tax strategies before selling assets to manage capital gains, offset losses, and time transactions efficiently. From tax-loss harvesting to holding period considerations, thoughtful planning can influence the final after-tax return. This guide explains common strategies investors consider and the questions many Americans ask before selling investments.

Why Tax Planning Matters Before Selling Investments

Selling an asset is rarely just a financial decision—it’s also a tax event. When investors sell stocks, mutual funds, real estate, or other appreciated assets, the profit may be subject to capital gains tax. Depending on income level and holding period, those taxes can materially reduce net returns.

According to the Internal Revenue Service (IRS), long-term capital gains rates in the United States are typically 0%, 15%, or 20%, depending on taxable income. High-income households may also pay an additional 3.8% Net Investment Income Tax (NIIT).

For many investors, the difference between a well-timed sale and an unplanned transaction can be substantial. Reviewing tax strategies before selling helps answer practical questions such as:

- How much tax will this sale trigger?

- Is this the right year to realize gains?

- Are there losses that could offset the gain?

- Would waiting change the tax rate?

Professional investors and financial planners often analyze these questions well before executing a trade.

Understanding Capital Gains: The Starting Point

Before exploring strategies, it helps to understand how capital gains taxes work.

A capital gain occurs when an asset is sold for more than its purchase price. The tax treatment depends on how long the asset was held.

Short-term capital gains

- Asset held one year or less

- Taxed at ordinary income tax rates (which can exceed 30%)

Long-term capital gains

- Asset held longer than one year

- Taxed at preferential rates (0%, 15%, or 20%)

Because the tax difference can be significant, many investors carefully review the holding period before selling.

For example, an investor who sells a stock after 11 months may pay ordinary income tax. Waiting one additional month could qualify the gain for a lower long-term rate.

Strategy 1: Reviewing the Holding Period Before Selling

One of the simplest yet most overlooked tax strategies is checking the asset’s holding period.

If an investment is approaching the one-year mark, delaying the sale can potentially lower the tax rate on gains.

Consider this example:

A software engineer in California sells stock with a $40,000 gain after holding it for 11 months. Because it’s short-term, the gain is taxed at her marginal income tax rate.

If she waits another month, the gain becomes long-term and could be taxed at 15% instead of over 30%, depending on income level.

In many cases, simply reviewing the holding period before executing a sale can materially affect the after-tax outcome.

Strategy 2: Using Tax-Loss Harvesting

Tax-loss harvesting involves selling investments that have declined in value to offset taxable gains elsewhere in the portfolio.

Investors often review their portfolios before realizing gains to identify potential losses that could reduce the tax impact.

Common scenarios include:

- Selling a losing stock to offset gains from a profitable investment

- Rebalancing a portfolio while capturing tax losses

- Using losses to offset gains from real estate or mutual fund distributions

Important rules apply. The wash-sale rule prohibits claiming a loss if the same or substantially identical investment is repurchased within 30 days.

Despite these restrictions, tax-loss harvesting is widely used in portfolio management because it allows investors to:

- Offset capital gains

- Deduct up to $3,000 of excess losses against ordinary income annually

- Carry forward unused losses to future tax years

Strategy 3: Timing Asset Sales Across Tax Years

The calendar year can influence taxes as much as the investment itself.

Investors sometimes delay or accelerate asset sales depending on their broader financial picture.

For example, selling in a year with lower income may place the investor in a lower capital gains bracket.

Situations where timing may matter include:

- Retirement year

- Temporary career break

- Business income fluctuation

- Large charitable deductions in the same year

A retiree, for instance, may intentionally sell appreciated assets in the early years of retirement when taxable income is relatively low.

This strategy can sometimes allow gains to be taxed at the 0% long-term capital gains rate.

Strategy 4: Offsetting Gains with Carryforward Losses

Many investors forget about capital losses from prior years.

If losses exceeded gains in the past, the remaining losses can often be carried forward indefinitely and applied to future gains.

This can meaningfully reduce taxes when selling assets later.

Example:

An investor recorded $20,000 in losses during a market downturn three years ago but used only $5,000 to offset gains.

The remaining $15,000 loss carryforward could be applied when selling appreciated assets today.

Investors often review their tax history before selling to determine whether unused losses exist.

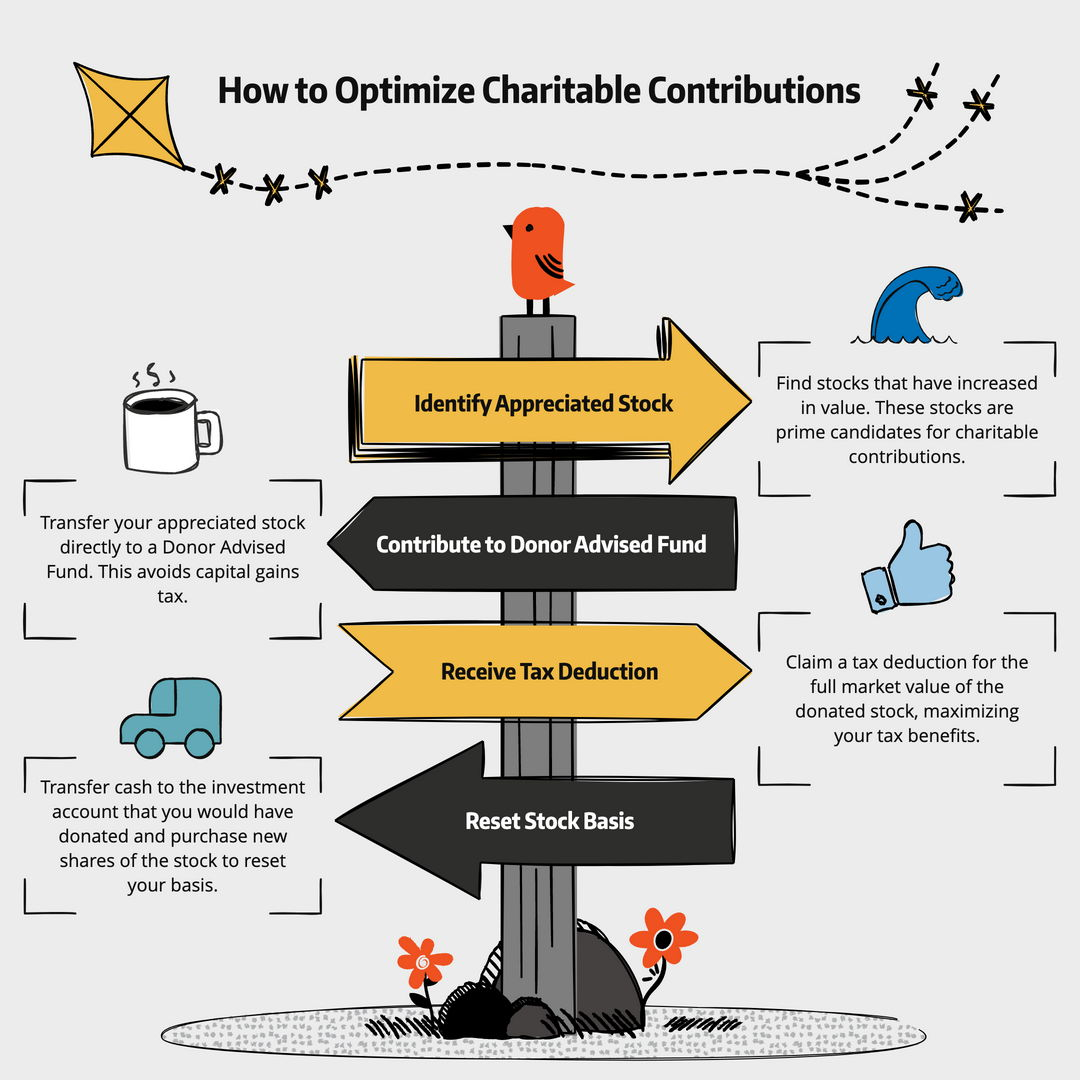

Strategy 5: Donating Appreciated Assets

Charitable giving can also be part of a tax-efficient selling strategy.

Instead of selling appreciated stock and donating cash, some investors choose to donate the stock directly.

This approach may allow them to:

- Avoid paying capital gains tax on the appreciation

- Receive a charitable deduction for the full market value (if eligible)

Example:

An investor bought shares worth $5,000, which later grew to $25,000.

If sold, the $20,000 gain would trigger capital gains tax. But donating the shares to a qualified charity may eliminate that tax while generating a deduction.

This strategy is commonly used by investors who support charitable causes and hold long-term appreciated securities.

Strategy 6: Reviewing State Taxes

Federal capital gains taxes are only part of the equation.

Many states also tax investment gains.

Some states tax capital gains at ordinary income rates, while others have no state income tax at all.

For example:

- California taxes capital gains as ordinary income.

- Florida and Texas have no state income tax.

For investors considering relocation, the timing of a major asset sale relative to residency status can influence overall taxes.

Because state rules vary widely, investors often review residency and tax implications before executing large transactions.

Strategy 7: Managing Mutual Fund and ETF Distributions

Mutual funds sometimes distribute capital gains even if investors did not sell shares.

These distributions typically occur near year-end and can create unexpected tax liabilities.

Investors reviewing asset sales may also examine:

- Upcoming mutual fund distributions

- Tax efficiency of specific funds

- Whether switching to more tax-efficient vehicles such as ETFs makes sense

Many experienced investors consider these distribution schedules before deciding when to sell.

Strategy 8: Considering Retirement Accounts vs Taxable Accounts

Where an investment is held also matters.

Assets inside tax-advantaged accounts such as IRAs or 401(k)s generally do not trigger capital gains taxes when sold within the account.

By contrast, selling assets in taxable brokerage accounts does.

Investors reviewing a sale often ask:

- Can rebalancing occur within retirement accounts instead?

- Should gains be realized in tax-advantaged accounts first?

- Would shifting asset placement reduce future taxes?

Asset location strategies can sometimes help reduce taxable events over time.

Frequently Asked Questions

What taxes do you pay when selling investments?

Most investors pay capital gains tax on profits when selling investments. The rate depends on the holding period and taxable income. Short-term gains are taxed as ordinary income, while long-term gains are typically taxed at 0%, 15%, or 20%.

How can investors reduce capital gains taxes legally?

Common strategies include tax-loss harvesting, holding assets for more than one year, using loss carryforwards, donating appreciated assets, and timing sales in lower-income years.

Is it better to sell investments at the end of the year?

Not always. Some investors sell late in the year to offset gains with losses, but others wait until the following year depending on income levels and tax planning considerations.

What is tax-loss harvesting?

Tax-loss harvesting involves selling investments at a loss to offset gains elsewhere in the portfolio. This can reduce taxable capital gains.

How long should you hold an investment to avoid short-term capital gains?

More than one year. Assets held longer than one year qualify for long-term capital gains tax rates, which are typically lower.

Can capital losses offset ordinary income?

Yes. Up to $3,000 per year of excess capital losses can offset ordinary income, with additional losses carried forward.

Do retirees pay capital gains tax?

Yes, but depending on taxable income, some retirees may qualify for the 0% long-term capital gains tax bracket.

Are mutual fund distributions taxable?

Yes. Capital gain distributions from mutual funds are typically taxable in the year they are received if held in taxable accounts.

Should investors sell assets inside retirement accounts first?

Selling assets within retirement accounts generally does not trigger capital gains taxes, but withdrawals from traditional retirement accounts may be taxed as income.

Do state taxes apply to investment gains?

Many states tax capital gains, often as ordinary income. A few states have no state income tax.

Looking Beyond the Sale: Planning for the After-Tax Return

Investors often focus on market timing or asset selection, but the after-tax outcome ultimately determines how much wealth is retained.

Reviewing tax strategies before selling assets allows investors to evaluate timing, offset gains with losses, and consider broader financial circumstances. While no strategy eliminates taxes entirely, thoughtful planning can help investors manage tax exposure in a way that aligns with long-term financial goals.

In practice, experienced investors treat taxes as part of the investment decision itself—reviewing them alongside market conditions, portfolio allocation, and future income expectations.

Key Points Investors Often Keep in Mind

- Capital gains taxes depend on holding period and income level

- Long-term gains typically receive lower tax rates

- Tax-loss harvesting can offset investment gains

- Loss carryforwards may reduce future tax liabilities

- Timing sales across tax years can affect tax brackets

- Donating appreciated assets may reduce taxable gains

- Mutual fund distributions can create unexpected taxes

- Asset location between taxable and retirement accounts matters