Summary

Year-end tax planning is about more than reducing this year’s bill. Revisiting core tax strategies before December 31 can help Americans manage cash flow, avoid surprises, and align taxes with long-term goals. This guide explains practical, legal strategies worth reviewing before the calendar closes.

Why Year-End Tax Strategy Reviews Matter More Than Most People Realize

For many Americans, tax planning starts and ends in March or April. By then, however, nearly all meaningful tax decisions have already been made. Income has been earned, deductions are largely fixed, and opportunities to reduce liability are limited.

Revisiting tax strategies before the end of each year allows for proactive decision-making. This is when timing still works in your favor. Actions taken before December 31 can influence your current-year tax outcome, shape future obligations, and help you avoid reactive choices made under filing pressure.

The importance of year-end planning grows as income becomes more complex. Raises, bonuses, investment activity, side income, business ownership, and life events all affect tax exposure in ways that often go unnoticed until it’s too late to adjust.

The Difference Between Tax Preparation and Tax Strategy

Tax preparation is backward-looking. It focuses on reporting what already happened and complying with the law. Tax strategy, by contrast, is forward-looking. It involves making informed decisions in advance to manage how income, deductions, and credits are recognized.

A useful way to think about it is this:

Tax preparation answers what you owe. Tax strategy helps determine why you owe it—and whether the outcome could have been different.

Year-end is one of the few windows where strategy and preparation overlap. Decisions made now can still meaningfully affect the numbers your tax preparer will later report.

Reviewing Income Timing: When Earning More Isn’t Always Neutral

Income timing is one of the most overlooked aspects of tax planning. For salaried employees, flexibility may be limited, but bonuses, commissions, stock compensation, freelance income, and business revenue often offer choices.

If income is higher than expected this year, accelerating deductions or deferring certain income may help manage marginal tax rates. Conversely, if income is unusually low, recognizing additional income before year-end can sometimes reduce long-term taxes.

Examples include:

- Freelancers choosing when to invoice clients

- Business owners deciding whether to delay or accelerate revenue recognition

- Employees evaluating deferred compensation elections

The goal is not to avoid income, but to align income with the most favorable tax periods whenever legally possible.

Capital Gains and Losses: A Strategic Review Opportunity

Investment activity often creates unexpected tax consequences. Selling appreciated assets triggers capital gains, while unrealized losses remain unused unless acted upon.

Before year-end, it’s worth reviewing taxable investment accounts to evaluate gains and losses. This review may uncover opportunities to offset gains with losses, rebalance portfolios tax-efficiently, or avoid unintended short-term capital gains.

Key considerations include:

- The difference between short-term and long-term capital gains

- How realized gains interact with other income

- The annual limit on deductible capital losses against ordinary income

According to IRS data, many taxpayers fail to use available capital losses effectively, leaving tax savings unrealized year after year.

Retirement Contributions: Deadlines Create Leverage

Retirement accounts remain one of the most reliable tools for tax efficiency. While some contributions can be made after year-end, others must be completed before December 31 to count for the current tax year.

Employer-sponsored plans like 401(k)s typically require contributions to be completed through payroll by year-end. Individual retirement accounts may offer more flexibility, but income thresholds and contribution limits still apply.

Year-end review questions include:

- Have maximum employer plan contributions been reached?

- Does current income affect eligibility for Roth or traditional IRA contributions?

- Would increasing contributions reduce adjusted gross income in a meaningful way?

According to the Investment Company Institute, many workers contribute well below annual limits despite having the capacity to save more, often due to lack of timely review.

Charitable Giving: Strategy Beyond Generosity

Charitable giving is personal, but its tax impact can be strategic. Year-end giving decisions should consider not just intent, but structure.

Some taxpayers benefit from bunching charitable contributions into a single year to exceed the standard deduction threshold. Others may benefit from donating appreciated assets instead of cash, potentially avoiding capital gains taxes while still receiving a deduction.

Important factors to revisit include:

- Whether itemizing deductions is beneficial this year

- Documentation requirements for charitable gifts

- The tax treatment of non-cash donations

The IRS continues to emphasize proper substantiation for charitable deductions, making thoughtful planning especially important.

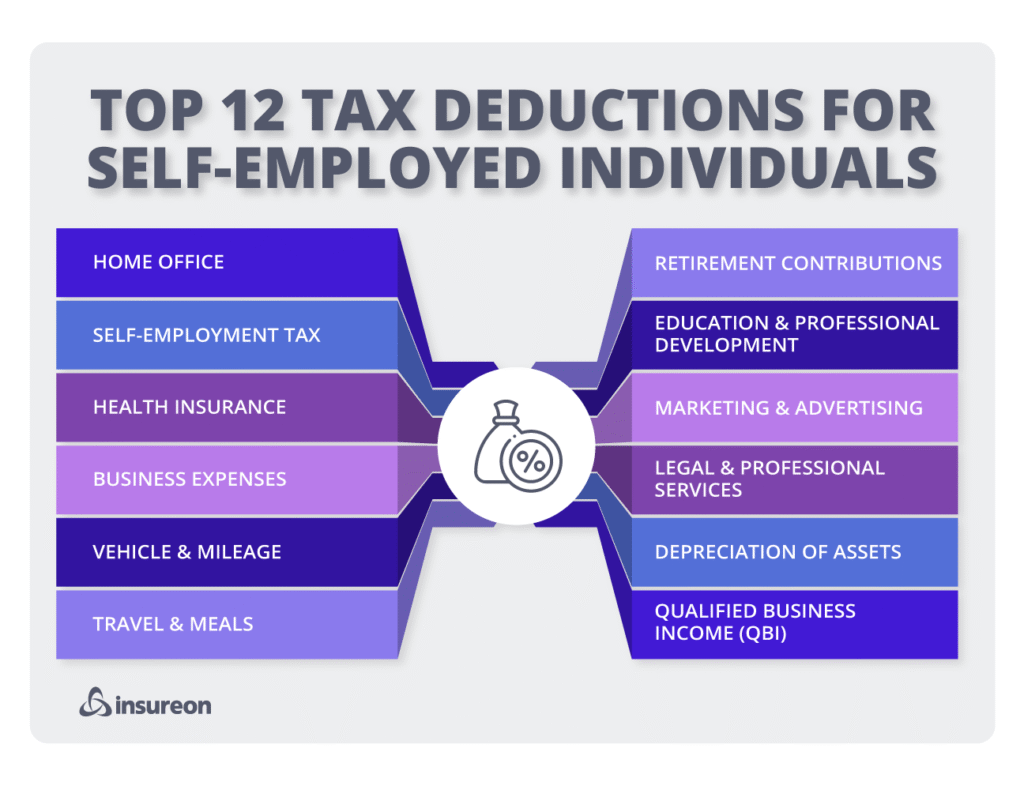

Business Owners and Self-Employed Filers: Extra Complexity, Extra Opportunity

For business owners and self-employed individuals, year-end tax strategy is especially consequential. Business income affects not only income tax but also self-employment tax, estimated payments, and potential deductions.

Common year-end considerations include:

- Timing of expenses and equipment purchases

- Retirement plan contributions for owner-only or small-group plans

- Reviewing estimated tax payments to avoid penalties

Even small timing decisions can have meaningful impacts when business income fluctuates year to year.

State and Local Tax Factors Often Missed Until Filing Season

Federal taxes tend to dominate planning conversations, but state and local taxes play a significant role in overall liability. Changes in residence, remote work arrangements, or property ownership can alter state tax exposure in ways that are easy to miss.

Year-end is a good time to confirm:

- Residency status for state tax purposes

- Withholding accuracy for multi-state income

- Property tax payments and timing

Misunderstandings around state taxation are a common source of unexpected tax bills.

Common Year-End Tax Mistakes—and How to Avoid Them

Despite good intentions, many taxpayers repeat avoidable errors each year. These mistakes often stem from waiting too long or focusing on only one part of the tax picture.

Frequent pitfalls include:

- Assuming withholding automatically matches tax liability

- Overlooking investment-related taxes

- Ignoring life changes that affect filing status or credits

A structured year-end review helps catch these issues while there is still time to adjust.

When Professional Guidance Makes the Biggest Difference

Not every taxpayer needs complex planning, but certain situations benefit significantly from professional input. High income, business ownership, investment complexity, or major life events all increase the value of expert guidance.

Consulting a qualified tax professional before year-end allows recommendations to be implemented, not just discussed after the fact. The IRS itself encourages proactive tax planning to reduce filing errors and payment issues.

Frequently Asked Questions

1. When should I start reviewing my taxes before year-end?

Ideally by early fall, allowing time to adjust withholding, contributions, or income timing.

2. Can I still reduce my taxes after December 31?

Some actions, like IRA contributions, may still apply, but most strategic options expire at year-end.

3. Does year-end planning only matter for high-income earners?

No. Even moderate-income households can benefit from better withholding and credit awareness.

4. How do bonuses affect year-end tax strategy?

Bonuses can push income into higher brackets, making timing and withholding reviews important.

5. Is tax-loss harvesting appropriate every year?

It depends on investment performance and broader tax circumstances, not just market losses.

6. Should I itemize deductions every year?

Not necessarily. The standard deduction may be more beneficial in many years.

7. How do life events affect year-end tax planning?

Marriage, divorce, children, or job changes can all alter tax obligations significantly.

8. Are estimated tax payments required for everyone?

They are typically required for self-employed individuals and those with significant non-wage income.

9. Does contributing more to retirement always lower taxes?

Often, but eligibility rules and future tax considerations matter.

A Smarter Way to Close the Tax Year

Year-end tax planning is not about aggressive tactics or loopholes. It is about alignment—between income, timing, goals, and compliance. Revisiting tax strategies before December 31 allows decisions to be intentional rather than reactive, helping taxpayers move into the new year with fewer surprises and greater financial clarity.

Key Points to Keep in Mind as the Year Wraps Up

- Tax strategy works best before income is finalized

- Timing decisions can be as important as amounts

- Retirement and investment reviews often yield overlooked savings

- State and business taxes deserve equal attention

- Early planning reduces stress during filing season