Summary

Taxes can significantly shape long-term investment outcomes. Strategic tax planning—through asset location, tax-loss harvesting, retirement accounts, and capital-gain management—can improve after-tax returns and reduce unnecessary tax drag. For U.S. investors, understanding how taxes interact with portfolio decisions is essential for compounding wealth efficiently over decades and aligning investment strategies with long-term financial goals.

Why Taxes Matter More Than Most Investors Realize

Most investors focus on returns, risk, and diversification when building a portfolio. Yet one often overlooked factor—tax strategy—can quietly shape long-term outcomes just as much as investment selection.

Taxes create what financial planners call “tax drag,” the gradual reduction of portfolio growth caused by annual taxation on dividends, interest, and realized gains. Over decades, this drag compounds in the same way investment returns do.

Consider a simple example:

An investor earning 7% annually in a tax-efficient portfolio might retain nearly the full return. But if taxes reduce that return by even 1–2% per year, the long-term difference becomes substantial.

According to research from Vanguard, effective tax management can add up to 0.75% of additional annual return in some portfolios through improved asset location and tax-efficient strategies.

Over 30 years, that difference can translate into tens or hundreds of thousands of dollars depending on the portfolio size.

Tax strategy therefore isn’t about avoiding taxes entirely—it’s about managing when and how taxes occur so investments can compound more efficiently.

Understanding the Types of Investment Taxes

Before implementing tax strategies, investors need to understand the major categories of taxes that affect investment portfolios in the United States.

Capital Gains Taxes

Capital gains occur when investments are sold for more than their purchase price.

Two primary categories apply:

- Short-term capital gains – assets held under one year; taxed as ordinary income

- Long-term capital gains – assets held more than one year; taxed at reduced rates

For most Americans, long-term capital gains fall into three federal brackets:

- 0%

- 15%

- 20%

Holding investments longer can therefore significantly reduce the tax burden.

Dividend Taxes

Dividends paid by stocks are typically taxed in two ways:

- Qualified dividends (eligible for capital gains rates)

- Ordinary dividends (taxed as regular income)

Many index funds generate primarily qualified dividends, making them more tax-efficient than certain actively managed funds.

Interest Income

Interest from bonds and savings products is usually taxed as ordinary income, which can make fixed-income investments less tax-efficient in taxable accounts.

State Taxes

Many states impose additional taxes on investment income. For investors in higher-tax states such as California or New York, tax planning becomes even more important.

The Concept of Tax-Efficient Investing

Tax-efficient investing focuses on maximizing after-tax returns rather than pre-tax returns.

Two portfolios might generate the same gross returns, but the one with lower tax drag will accumulate more wealth.

Key principles include:

- Deferring taxes as long as possible

- Favoring investments with lower turnover

- Using tax-advantaged accounts strategically

- Managing capital gains realization

- Offsetting gains with losses when appropriate

In practice, these principles shape decisions about where assets are held, when they are sold, and how portfolios are rebalanced.

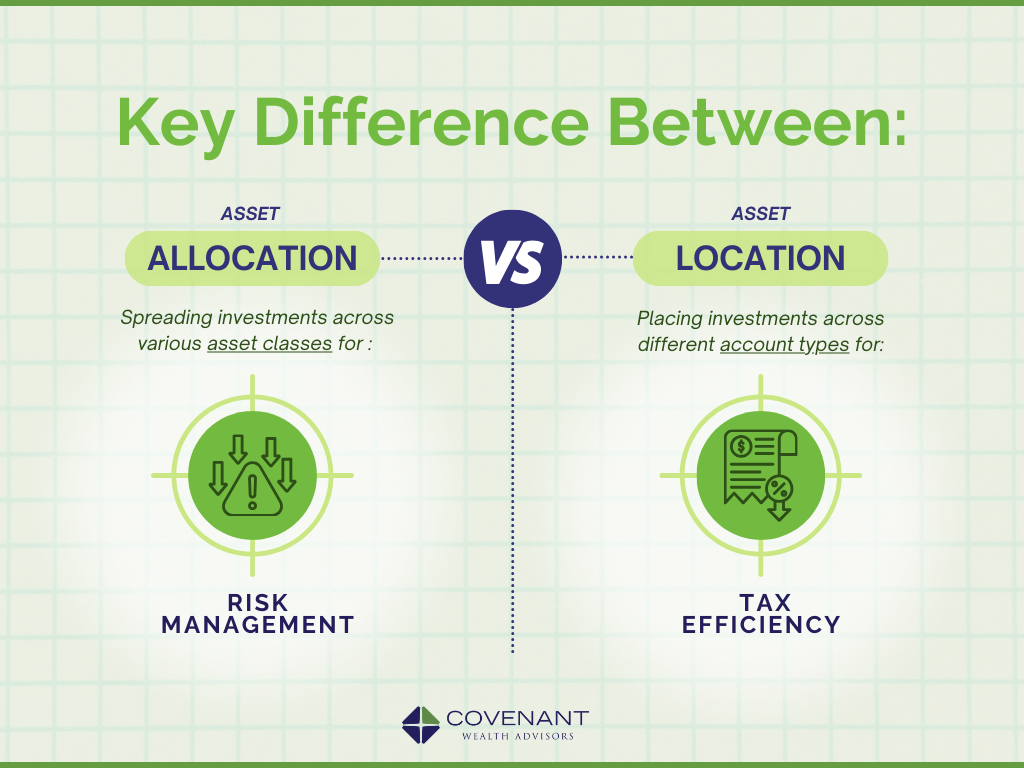

Asset Location: A Powerful but Overlooked Strategy

Most investors focus on asset allocation—how much money goes into stocks, bonds, and other assets.

Asset location, however, determines where those assets are held from a tax perspective.

Different accounts have different tax rules:

- Taxable brokerage accounts

- Traditional retirement accounts (401(k), IRA)

- Roth accounts

Each account type creates different tax implications.

Example of Smart Asset Location

Imagine an investor with three assets:

- U.S. stock index fund

- Corporate bond fund

- Real estate investment trust (REIT)

A tax-efficient arrangement might look like:

- Taxable account: U.S. stock index fund (tax efficient)

- Traditional IRA/401(k): bond funds (interest taxed as income)

- Roth IRA: higher-growth assets or REITs

Why this works:

- Tax-inefficient assets sit inside tax-deferred accounts

- Tax-efficient assets remain in taxable accounts

Research from Morningstar shows proper asset location can increase portfolio efficiency by several tenths of a percent annually, which compounds significantly over time.

Tax-Loss Harvesting: Turning Losses into Strategy

Tax-loss harvesting is one of the most widely used tax strategies in investing.

The concept is straightforward: when an investment declines in value, investors may sell it to realize the loss, which can then offset gains elsewhere.

Losses can be used to:

- Offset realized capital gains

- Offset up to $3,000 of ordinary income per year

- Carry forward to future tax years

Example

Suppose an investor sells a stock with a $10,000 gain.

If another investment shows a $6,000 loss, selling it reduces the taxable gain to $4,000.

However, tax-loss harvesting must follow IRS rules, including the wash sale rule, which prevents investors from repurchasing the same security within 30 days.

Many robo-advisors now automate tax-loss harvesting, but long-term investors can also apply it manually during market downturns.

Managing Capital Gains Over Time

Long-term investing naturally creates large unrealized gains.

Strategic management of those gains can reduce tax burdens.

Common approaches include:

- Holding assets for more than one year

- Spreading sales across multiple tax years

- Harvesting gains during low-income years

- Donating appreciated assets to charity

- Passing assets through estate transfers

For example, retirees often realize gains during years when their taxable income falls into the 0% long-term capital gains bracket, which can eliminate federal tax on those gains.

This strategy is sometimes called “income smoothing.”

Retirement Accounts and Tax Planning

Retirement accounts are one of the most powerful tax tools available to investors.

These accounts create tax deferral or tax-free growth, both of which dramatically affect compounding.

Major Account Types

Traditional 401(k) and IRA

- Contributions often tax-deductible

- Investments grow tax-deferred

- Withdrawals taxed as income

Roth IRA and Roth 401(k)

- Contributions made with after-tax dollars

- Growth is tax-free

- Qualified withdrawals are tax-free

Many investors combine both types to create tax diversification, giving flexibility when withdrawing money in retirement.

Example

An investor retiring with both account types can:

- Withdraw from taxable accounts in low-income years

- Use Roth withdrawals to avoid pushing income into higher tax brackets

- Delay traditional withdrawals when possible

Strategic withdrawal planning can significantly reduce lifetime taxes.

Tax Efficiency of Different Investment Vehicles

Not all investments are equally tax-friendly.

Some naturally generate fewer taxable events.

Generally More Tax-Efficient

- Index funds

- Exchange-traded funds (ETFs)

- Municipal bonds

- Buy-and-hold equity strategies

Generally Less Tax-Efficient

- Actively managed mutual funds

- High-turnover strategies

- REIT distributions

- High-yield bond funds

ETFs in particular tend to be tax-efficient due to their creation/redemption mechanism, which often avoids triggering capital gains distributions.

This structural advantage has contributed to the rapid growth of ETFs in U.S. investment portfolios.

Estate Planning and Step-Up in Basis

Another long-term tax advantage involves estate planning rules.

Under current U.S. law, many inherited investments receive a step-up in cost basis.

This means the cost basis resets to the asset’s market value at the time of inheritance.

Example:

- Original purchase price: $50,000

- Value at inheritance: $200,000

The heir’s basis becomes $200,000, eliminating tax on the $150,000 gain.

Because of this rule, many investors avoid selling highly appreciated assets late in life unless necessary.

Tax laws can change, however, so estate strategies should be revisited periodically.

The Importance of Coordinating Taxes and Investment Strategy

Effective tax planning rarely happens in isolation.

Instead, it sits at the intersection of:

- Portfolio management

- Retirement planning

- Income strategy

- Estate planning

Professional advisors often refer to this integrated approach as tax-aware investing.

Rather than reacting to taxes after the fact, investors proactively design portfolios with tax efficiency in mind.

For long-term investors, this mindset can mean:

- Fewer unnecessary tax events

- More consistent compounding

- Greater flexibility during retirement

Even modest improvements in after-tax returns can dramatically reshape outcomes across decades of investing.

Frequently Asked Questions

What is tax-efficient investing?

Tax-efficient investing focuses on maximizing after-tax returns by reducing unnecessary tax costs through strategies such as asset location, tax-loss harvesting, and using tax-advantaged accounts.

How much can tax strategy improve returns?

Research from Vanguard suggests tax-efficient strategies may improve portfolio outcomes by up to 0.75% annually, depending on portfolio structure and tax bracket.

What is tax drag?

Tax drag refers to the reduction in investment returns caused by taxes on dividends, interest, and realized capital gains.

Are ETFs more tax-efficient than mutual funds?

Often yes. ETFs typically generate fewer capital gains distributions due to their unique creation and redemption mechanism.

What is the wash sale rule?

The IRS wash sale rule prevents investors from claiming a loss if they repurchase the same or substantially identical security within 30 days before or after the sale.

Should high-dividend stocks be in retirement accounts?

Often yes, because dividends may be taxed as income. Holding them in tax-advantaged accounts can reduce tax drag.

What is tax-loss harvesting?

Tax-loss harvesting involves selling investments at a loss to offset gains elsewhere in the portfolio and reduce taxes.

Do long-term investors still need tax planning?

Yes. Even buy-and-hold investors benefit from asset location, retirement accounts, and careful gain realization.

What is the step-up in basis?

The step-up in basis resets an inherited asset’s cost basis to its market value at the time of inheritance, often eliminating past capital gains taxes.

When should investors consult a tax professional?

Complex situations—such as large portfolios, multiple income sources, or retirement withdrawal planning—often benefit from professional tax guidance.

Building Wealth with Tax Awareness

Successful long-term investing isn’t only about choosing the right assets—it’s about keeping more of what those assets earn.

Taxes are one of the few variables investors can partially control.

By incorporating tax strategy into portfolio decisions—through asset location, tax-loss harvesting, retirement planning, and thoughtful capital-gain management—investors can reduce tax drag and allow compounding to work more efficiently over decades.

Even modest tax improvements can translate into substantial wealth accumulation over time.

Key Ideas at a Glance

- Taxes can significantly impact long-term investment returns

- Asset location helps place investments in the most tax-efficient accounts

- Tax-loss harvesting can offset gains and reduce taxable income

- Long-term holding periods reduce capital gains taxes

- Retirement accounts provide powerful tax advantages

- ETFs and index funds are often more tax-efficient than actively managed funds

- Estate rules like step-up in basis affect long-term tax planning

- Integrating taxes into investment decisions improves after-tax outcomes