Summary

Before filing taxes, financial planners often recommend reviewing key financial decisions that can influence deductions, credits, and long-term tax efficiency. From maximizing retirement contributions to documenting deductions and managing investment gains, these steps can help Americans file more accurately and strategically. Taking time to review these areas before submitting your return may reduce surprises and improve overall tax planning.

Why Pre-Filing Tax Planning Matters

For many Americans, tax season begins when forms arrive in the mail or documents appear in online portals. But financial planners often approach it differently. They view the weeks before filing as a final opportunity to review decisions that affect both the current tax return and long-term financial planning.

According to the IRS, more than 168 million individual tax returns are filed each year in the United States. Yet many taxpayers submit returns without revisiting potential deductions, contribution limits, or tax-efficient strategies.

Financial planners emphasize that tax filing should not be treated as a purely administrative task. Instead, it can serve as a checkpoint for reviewing financial habits, verifying documentation, and making last-minute adjustments that remain allowable under tax rules.

The most effective pre-filing moves typically fall into several categories:

- Retirement contribution adjustments

- Deduction verification and documentation

- Investment tax management

- Health savings planning

- Income and withholding review

While not every strategy applies to every household, reviewing these areas before filing can make a meaningful difference.

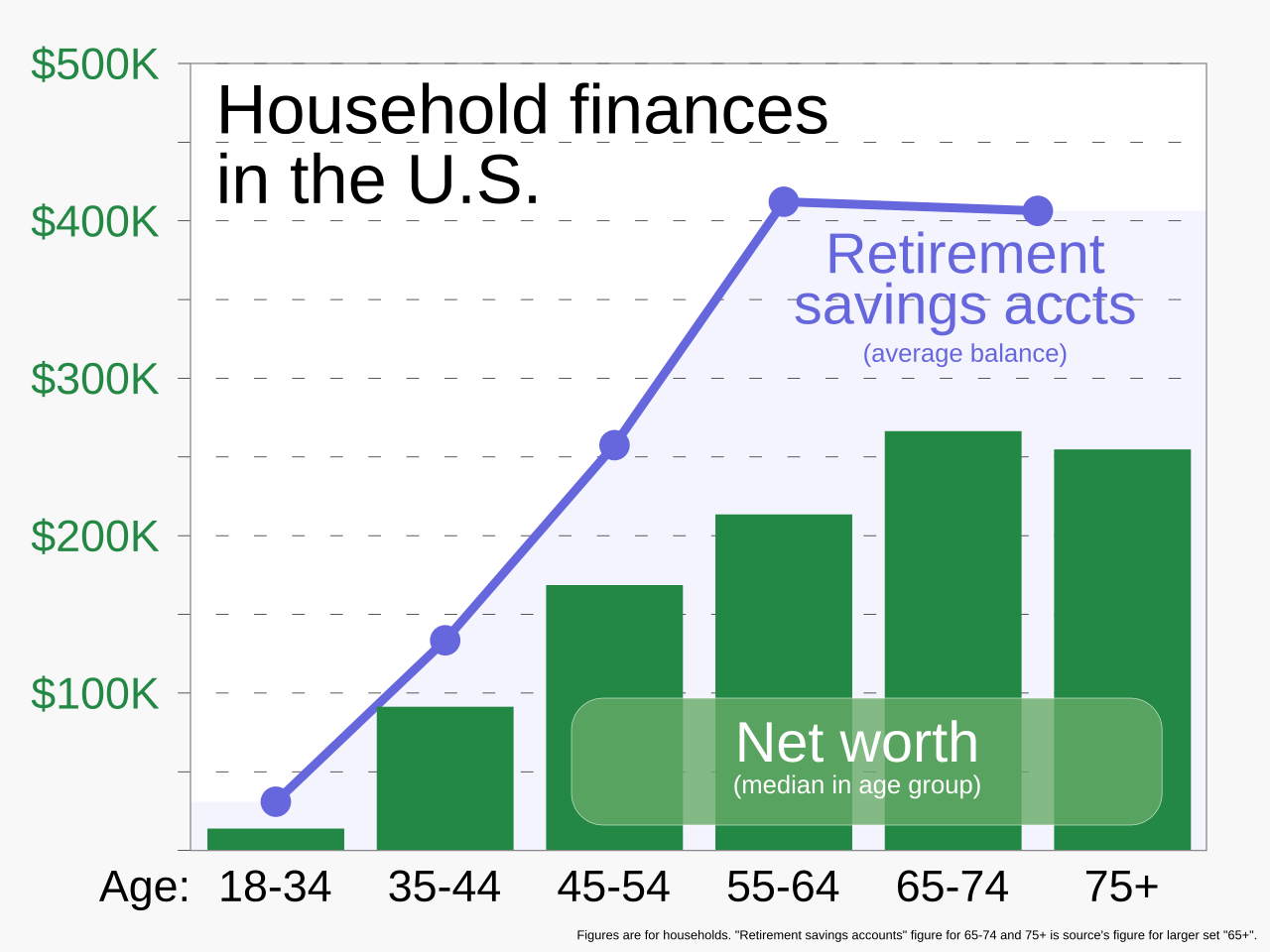

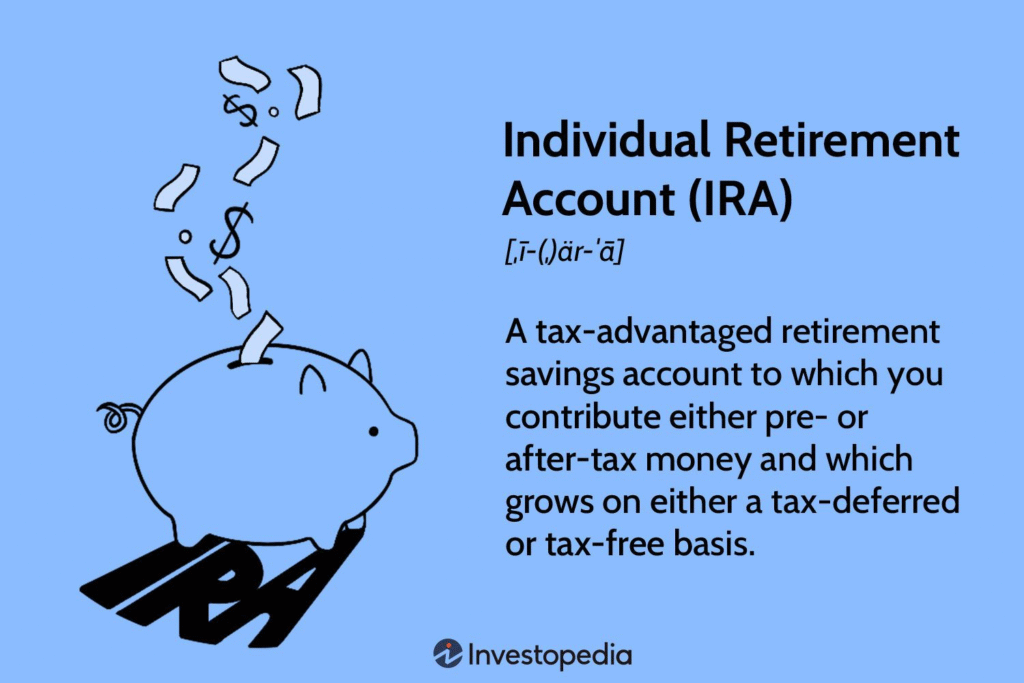

1. Confirm Retirement Contributions and Eligibility

Retirement contributions are one of the most commonly reviewed areas before filing taxes. Financial planners often encourage clients to confirm whether they have fully used eligible contribution opportunities.

For many Americans, contributions to certain retirement accounts can still be made up until the tax filing deadline, usually April 15.

Common accounts planners review include:

- Traditional IRA contributions

- Roth IRA eligibility

- Self-employed retirement plans such as SEP IRAs

- Catch-up contributions for individuals age 50 and older

In 2024 and 2025, the IRA contribution limit is $7,000, or $8,000 for those age 50+, according to IRS guidelines.

For example, a married couple filing jointly may discover that one spouse still qualifies for a deductible traditional IRA contribution. Even a modest last-minute contribution could slightly reduce taxable income.

Financial planners often encourage households to review retirement contributions annually because the tax benefits accumulate over time, not just in a single filing year.

2. Revisit Deduction Opportunities

Many taxpayers rely on standard deductions, but planners still recommend verifying whether itemizing might provide greater value.

The standard deduction for 2024 is:

- $14,600 for single filers

- $29,200 for married couples filing jointly

However, households with certain expenses may benefit from itemizing.

Common deductions worth reviewing include:

- State and local taxes (subject to current limits)

- Mortgage interest

- Charitable donations

- Medical expenses exceeding IRS thresholds

Financial planners frequently recommend gathering supporting documentation before filing rather than reconstructing it later during an audit or amendment.

For instance, charitable giving records often require written confirmation from the organization, especially for donations exceeding $250.

Keeping organized records can simplify filing and strengthen documentation if questions arise later.

3. Review Capital Gains and Investment Activity

Investment accounts can introduce additional complexity at tax time. Financial planners often review brokerage statements carefully to understand how capital gains or losses may affect the return.

According to data from Morningstar and IRS reports, many investors underestimate the tax impact of:

- Mutual fund distributions

- Short-term trading gains

- Dividend income

A planner might review whether losses harvested earlier in the year properly offset gains.

For example, if an investor sold one stock at a gain but another at a loss, the loss may reduce the taxable gain depending on timing and classification.

Common investment considerations include:

- Short-term vs. long-term capital gains rates

- Dividend tax treatment

- Carryforward capital losses from previous years

These details can affect the final tax calculation and are often worth reviewing before submitting a return.

4. Evaluate Health Savings Account (HSA) Contributions

Health Savings Accounts remain one of the few tax-advantaged tools offering triple tax benefits:

- Contributions may be tax-deductible

- Investment growth is tax-deferred

- Qualified withdrawals are tax-free

Many financial planners check whether clients have fully utilized their HSA contribution limits.

For 2024:

- Individual coverage limit: $4,150

- Family coverage limit: $8,300

Those age 55 or older may add a $1,000 catch-up contribution.

Because HSA contributions can often be made until the tax filing deadline, reviewing eligibility before filing may create a final opportunity to improve tax efficiency.

5. Verify Tax Credits

Tax credits reduce taxes dollar for dollar, making them particularly valuable. Financial planners often review eligibility for credits that households may overlook.

Some of the most commonly reviewed credits include:

- Child Tax Credit

- American Opportunity Credit for education expenses

- Lifetime Learning Credit

- Saver’s Credit for retirement contributions

For example, the Saver’s Credit can apply to individuals with moderate incomes who contribute to retirement accounts, but many eligible taxpayers are unaware of it.

Financial planners frequently revisit credit eligibility during the filing process to ensure no opportunities are missed.

6. Double-Check Income Documents

Before filing, planners often confirm that all income statements are accounted for.

Common tax forms include:

- W-2 forms from employers

- 1099-NEC or 1099-MISC for freelance work

- 1099-DIV and 1099-INT from financial institutions

- 1099-B from brokerage accounts

Missing documents are one of the most common reasons the IRS issues notices after returns are filed.

Because financial institutions also send copies to the IRS, discrepancies can trigger automated matching alerts.

Taking time to confirm that all documents are included can reduce the likelihood of follow-up letters or amended returns.

7. Review Withholding and Estimated Payments

Even after preparing a return, financial planners often review whether withholding levels were appropriate during the year.

If the return results in a large refund or significant balance due, it may signal that adjustments should be made for the upcoming tax year.

For instance:

- A large refund may mean excessive withholding from paychecks

- A balance due may indicate insufficient withholding or estimated payments

Adjusting withholding using Form W-4 can help households better align tax payments with actual liability.

This step does not change the current return but can improve financial planning for the next year.

8. Organize Records for Future Tax Years

Experienced planners often treat tax season as an opportunity to improve recordkeeping habits.

Common records worth organizing include:

- Donation receipts

- Investment statements

- Medical expense documentation

- Property tax payments

- Education expense records

Well-organized records simplify future filings and make financial planning discussions more productive.

Some planners recommend maintaining a digital “tax folder” that stores all documents related to each tax year.

Frequently Asked Questions

When is the latest I can contribute to an IRA for tax purposes?

Typically, IRA contributions can be made until the tax filing deadline, usually April 15 of the following year.

Should I file early or wait until closer to the deadline?

Filing early can reduce the risk of identity theft and allow more time to address issues if errors appear.

Is itemizing deductions still common?

Since the standard deduction increased significantly under recent tax law changes, fewer taxpayers itemize. However, it can still be beneficial in certain situations.

Can charitable donations reduce my taxes?

Yes, if you itemize deductions and have proper documentation from the charitable organization.

What if I receive a tax form after filing?

You may need to file an amended return using Form 1040-X if the form affects your taxable income.

Do capital losses help reduce taxes?

Capital losses can offset capital gains and may reduce taxable income within IRS limits.

How can I avoid a large tax bill next year?

Review withholding levels or estimated tax payments and adjust them based on current income.

Are HSAs still useful even if I’m healthy?

Many planners recommend HSAs because they combine tax benefits with long-term savings flexibility.

Should I consult a tax professional before filing?

Households with investments, self-employment income, or major financial changes may benefit from professional review.

What documents should I keep after filing?

Experts typically recommend keeping tax returns and supporting records for at least three years.

A Planner’s Perspective on the Final Pre-Filing Checklist

Financial planners rarely treat tax filing as a single-day event. Instead, they approach it as part of a broader financial review that connects income, investments, retirement planning, and long-term goals.

Before submitting a return, they often revisit key questions:

- Have all eligible contributions been made?

- Are deductions and credits properly documented?

- Do investment transactions align with tax strategy?

- Are withholding levels appropriate for the coming year?

These small reviews may not dramatically change every tax return, but they help households build more consistent financial habits over time.

Key Insights Worth Remembering

- Review retirement contribution opportunities before filing

- Confirm eligibility for tax credits and deductions

- Verify all income documents are included

- Evaluate investment gains and losses

- Consider HSA contributions if eligible

- Adjust withholding for the upcoming year

- Maintain organized tax records for future filings