Summary

Retirement income isn’t determined only by how much you save—it’s shaped heavily by tax planning decisions made years before and during retirement. Strategic choices about account types, withdrawal timing, Social Security, and required distributions can dramatically affect how much income retirees keep after taxes. Understanding these decisions helps Americans build a more predictable, tax-efficient retirement income strategy.

Why Taxes Matter More in Retirement Than Many People Expect

For many Americans, retirement planning focuses almost entirely on building a large nest egg. But what ultimately determines financial security in retirement is not the account balance—it’s the after-tax income that balance produces.

Tax planning becomes critical because retirees often draw income from several sources simultaneously:

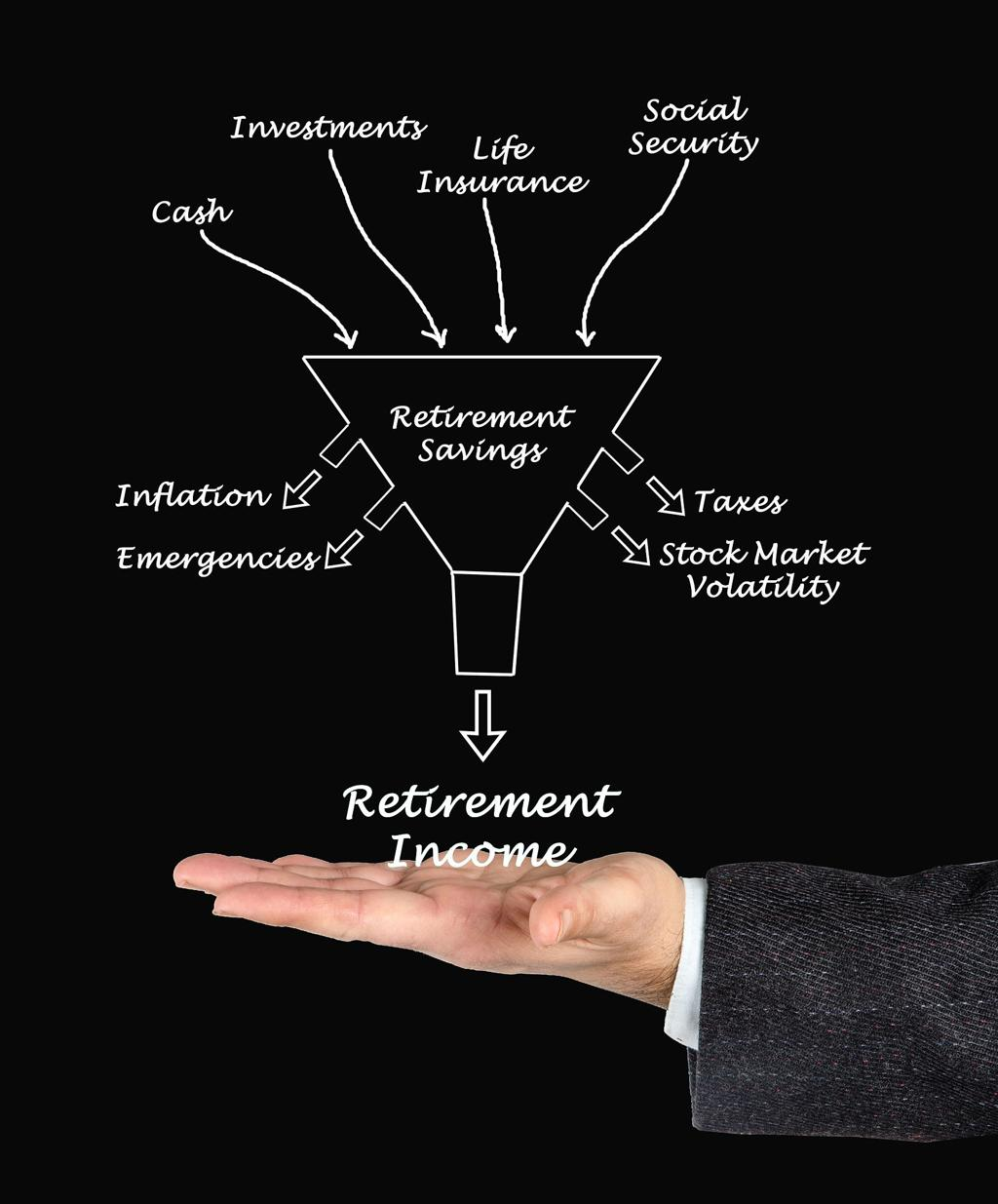

- Social Security benefits

- Traditional retirement accounts such as 401(k)s and IRAs

- Roth accounts

- Taxable brokerage accounts

- Pension income (if available)

Each of these income streams is taxed differently. Without thoughtful planning, retirees can unintentionally push themselves into higher tax brackets, increase the taxation of Social Security benefits, or trigger large required distributions later in life.

According to the Employee Benefit Research Institute, roughly 80% of retirees rely on Social Security for a significant portion of their income, while a growing share depend on withdrawals from tax-deferred retirement accounts. That combination creates tax complexity that many retirees underestimate.

Thoughtful tax planning can extend retirement savings significantly. In some cases, it can add years of financial stability simply by reducing unnecessary tax exposure.

Understanding the Three Tax Buckets of Retirement Income

Financial planners often describe retirement assets as belonging to three different tax buckets. Each bucket behaves differently when money is withdrawn.

1. Tax-Deferred Accounts

These include:

- Traditional 401(k)s

- Traditional IRAs

- 403(b) plans

Contributions typically reduce taxable income in the year they are made, but withdrawals are taxed as ordinary income.

These accounts are also subject to Required Minimum Distributions (RMDs) beginning at age 73 under current law.

2. Tax-Free Accounts

These include:

- Roth IRAs

- Roth 401(k)s (if rolled into Roth IRAs)

Contributions are made with after-tax dollars, but qualified withdrawals are tax-free.

Roth IRAs also have no lifetime RMDs, making them highly flexible for retirement planning.

3. Taxable Investment Accounts

Brokerage accounts fall into this category. They are taxed differently depending on the type of income generated:

- Dividends may receive preferential tax treatment

- Long-term capital gains are taxed at lower rates than ordinary income

- Losses can sometimes offset gains

A retirement strategy that balances withdrawals across these three buckets can significantly reduce lifetime tax liability.

The Hidden Impact of Withdrawal Timing

One of the most important tax decisions retirees face is when to begin withdrawing from different accounts.

Many people assume the default strategy is best: withdraw from tax-deferred accounts first and save Roth accounts for last. But in reality, that approach can sometimes lead to larger tax bills later.

Consider this example.

A retiree with a $1.2 million traditional IRA who delays withdrawals until required distributions begin may face large RMDs in their 70s. Those distributions can push taxable income higher, increasing:

- Federal income taxes

- Medicare premium surcharges (IRMAA)

- Taxes on Social Security benefits

Instead, some retirees choose to gradually withdraw from tax-deferred accounts during lower-income years between retirement and RMD age.

This strategy can help smooth tax brackets across decades rather than allowing them to spike later.

How Social Security Benefits Are Taxed

Many Americans are surprised to learn that Social Security benefits can be partially taxable.

Up to 85% of benefits may be taxed depending on a retiree’s combined income level.

Combined income includes:

- Adjusted gross income

- Non-taxable interest

- Half of Social Security benefits

For individuals:

- Income above $25,000 may trigger taxation

- Income above $34,000 can lead to up to 85% taxation

For married couples filing jointly:

- $32,000 and $44,000 are the key thresholds

Because withdrawals from traditional retirement accounts increase taxable income, they can indirectly cause more Social Security benefits to become taxable.

Strategic withdrawal planning can reduce this effect.

Roth Conversions: A Strategic Tax Planning Tool

A Roth conversion allows retirees or pre-retirees to move money from a traditional IRA into a Roth IRA.

The converted amount becomes taxable in the year of conversion, but future withdrawals are tax-free.

This strategy can be powerful in specific situations:

- Early retirement years with temporarily lower income

- Before Social Security begins

- Before required distributions start

- During market downturns when account values are lower

Example:

A retiree who converts $50,000 annually for several years while in a moderate tax bracket may reduce future RMDs and create a large tax-free income source later.

However, conversions must be carefully planned to avoid pushing income into significantly higher tax brackets.

The Overlooked Risk of Required Minimum Distributions

Required Minimum Distributions often become one of the largest tax surprises in retirement.

The IRS requires retirees to withdraw a specific percentage from tax-deferred retirement accounts each year starting at age 73.

These withdrawals are taxable regardless of whether the money is needed for living expenses.

Large RMDs can:

- Push retirees into higher tax brackets

- Increase taxation of Social Security

- Trigger higher Medicare premiums

Many retirees accumulate significant balances during decades of saving. Without early planning, RMDs can create tax pressure that lasts for the remainder of retirement.

Strategies to reduce this risk include:

- Roth conversions before RMD age

- Strategic early withdrawals

- Qualified charitable distributions (QCDs)

Coordinating Taxes with Medicare Premiums

Taxes don’t just affect income—they can also influence healthcare costs.

Medicare Part B and Part D premiums are tied to income through Income-Related Monthly Adjustment Amounts (IRMAA).

Higher income retirees pay significantly higher premiums.

For example, a couple with modified adjusted gross income above certain thresholds can see their monthly Medicare premiums increase substantially.

Large withdrawals, Roth conversions, or investment gains in a single year can unexpectedly trigger these surcharges.

Tax-aware retirement planning often includes managing income levels to avoid unnecessary IRMAA brackets.

Strategic Withdrawal Order: A Flexible Approach

Rather than following a rigid rule, many financial planners recommend a dynamic withdrawal strategy that adapts each year based on tax conditions.

A flexible approach may include:

- Using taxable accounts first in early retirement

- Filling lower tax brackets with moderate IRA withdrawals

- Performing partial Roth conversions

- Using Roth withdrawals later to avoid higher brackets

The goal is not simply minimizing taxes this year—but minimizing taxes across an entire retirement timeline.

Real-World Example of Tax-Efficient Retirement Planning

Consider a married couple retiring at age 62 with the following savings:

- $900,000 in traditional 401(k) accounts

- $200,000 in Roth IRAs

- $150,000 in a brokerage account

Without planning, they might wait until age 73 for withdrawals from the 401(k), triggering large RMDs.

Instead, a tax-aware strategy could look like this:

Ages 62–67

- Withdraw moderately from the 401(k)

- Perform small Roth conversions

- Use brokerage assets for supplemental income

Age 67

- Begin Social Security benefits

Age 73+

- RMDs are smaller due to earlier withdrawals and conversions

- Roth accounts provide tax-free income flexibility

Over decades, this approach can reduce total taxes and create a more stable income pattern.

Common Tax Planning Mistakes Retirees Make

Even well-prepared retirees can overlook important tax considerations.

Common mistakes include:

- Delaying all withdrawals until RMD age

- Ignoring Roth conversion opportunities

- Triggering large one-time taxable events

- Overlooking the tax impact of Social Security timing

- Failing to coordinate taxes with Medicare thresholds

Working with a tax-aware financial planner can help retirees avoid these pitfalls.

How Early Planning Improves Retirement Flexibility

The most powerful tax planning decisions often happen before retirement begins.

Building savings across multiple tax buckets creates flexibility later.

For example:

- Contributing to both traditional and Roth retirement accounts

- Maintaining a taxable brokerage account

- Understanding future tax bracket expectations

This diversified structure allows retirees to adjust income sources depending on tax circumstances each year.

In retirement planning, flexibility often becomes the most valuable asset.

Frequently Asked Questions

1. Why is tax planning important for retirement income?

Because different retirement income sources are taxed differently, strategic planning can reduce lifetime tax liability and increase after-tax income.

2. Are Roth withdrawals always tax-free?

Yes, if the account has been open for at least five years and the account holder is age 59½ or older.

3. What age do required minimum distributions begin?

Under current U.S. law, RMDs begin at age 73 for most retirees.

4. Can Social Security benefits be taxed?

Yes. Up to 85% of benefits may be taxable depending on combined income.

5. What is a Roth conversion?

It is the process of transferring funds from a traditional IRA or 401(k) into a Roth IRA, paying taxes now to avoid taxes later.

6. Do brokerage accounts help with retirement tax planning?

Yes. Capital gains are taxed differently from ordinary income, providing flexibility when managing taxable income levels.

7. Can taxes affect Medicare premiums?

Yes. Higher income can trigger IRMAA surcharges, increasing Medicare Part B and Part D premiums.

8. Should retirees withdraw from Roth or traditional accounts first?

It depends on individual tax circumstances. A blended, flexible strategy is often more tax-efficient.

9. Is it too late to do tax planning after retirement?

No. Strategic withdrawals, Roth conversions, and charitable distributions can still influence taxes during retirement.

10. How far ahead should tax planning begin?

Ideally 10–15 years before retirement, when income levels and contribution strategies can still be adjusted.

Designing a Tax-Efficient Retirement Paycheck

Retirement planning is often described as building a nest egg, but in practice it’s more like designing a paycheck that lasts decades.

Tax planning determines how efficiently that paycheck is delivered. Decisions about account types, withdrawal timing, Social Security coordination, and Roth strategies can dramatically shape the income retirees actually keep.

For many Americans, thoughtful tax planning can mean the difference between simply retiring—and retiring with financial confidence.

Key Retirement Tax Strategy Insights

- Retirement income is taxed differently depending on account type

- Strategic withdrawals can smooth tax brackets across decades

- Social Security benefits may be partially taxable

- Roth conversions can reduce future required distributions

- Medicare premiums can increase when income rises

- Early planning provides the most flexibility for tax-efficient income