Summary

Capital gains taxes can significantly affect long-term investment returns. Financial advisors often recommend structured strategies—such as holding assets longer, tax-loss harvesting, and coordinating gains with income levels—to manage tax exposure responsibly. Capital gains optimization is not about avoiding taxes but planning when and how gains occur so investors keep more of their returns while staying aligned with U.S. tax regulations.

Understanding Capital Gains Optimization

Capital gains optimization refers to the strategies investors use to manage when and how they realize investment gains in order to reduce unnecessary tax exposure. Financial advisors consistently emphasize that taxes are one of the largest “silent costs” investors face.

According to research published by the Vanguard Advisor’s Alpha framework, tax-efficient investment strategies can add roughly 0.75% of additional annual value to a portfolio over time. While that number may seem modest in a single year, over decades it can translate into meaningful wealth preservation.

Capital gains taxes apply when investors sell assets—such as stocks, mutual funds, or real estate—for more than their purchase price. The IRS divides gains into two primary categories:

- Short-term capital gains (assets held less than one year), taxed at ordinary income rates

- Long-term capital gains (assets held longer than one year), taxed at lower rates, typically 0%, 15%, or 20%

Financial advisors focus heavily on managing the timing and structure of these gains.

Rather than trying to eliminate taxes entirely—which is unrealistic—most advisors frame capital gains optimization as strategic timing and coordination with broader financial planning.

Why Capital Gains Planning Matters More Than Many Investors Expect

Taxes are rarely the first factor investors think about when evaluating investment decisions. Yet advisors often point out that poor tax planning can quietly erode portfolio returns.

Consider a simple example.

An investor sells a stock after eight months with a $20,000 gain. Because the holding period is under one year, the profit may be taxed at ordinary income rates—potentially as high as 37% federally, depending on income.

If that same investor waited four additional months to cross the one-year mark, the gain might instead fall into the 15% long-term capital gains bracket.

That timing difference alone could mean several thousand dollars in tax savings.

Financial advisors frequently stress that tax efficiency should be integrated into portfolio decisions—not treated as an afterthought during tax season.

The Core Strategies Advisors Use to Optimize Capital Gains

While every investor’s situation differs, financial advisors generally rely on a small group of well-tested strategies to manage capital gains effectively.

Holding Investments Long Enough to Qualify for Long-Term Rates

One of the most widely recommended strategies is simply extending the holding period.

The difference between short-term and long-term capital gains rates can be substantial. For high earners, the difference may exceed 20 percentage points.

Advisors often help clients review their portfolios near the one-year holding mark to determine whether selling immediately—or waiting a little longer—would create a better tax outcome.

Tax-Loss Harvesting

Tax-loss harvesting involves selling investments that have declined in value to offset gains realized elsewhere in the portfolio.

For example:

- An investor sells Stock A with a $15,000 gain

- They also sell Stock B with a $10,000 loss

The loss can offset part of the gain, leaving $5,000 of taxable profit.

If losses exceed gains, investors can deduct up to $3,000 against ordinary income each year, carrying remaining losses forward.

Many advisors view tax-loss harvesting as one of the most effective tools for managing long-term tax exposure.

Coordinating Gains With Lower-Income Years

Financial advisors frequently encourage clients to think beyond a single tax year.

Certain life events can temporarily reduce income, such as:

- Early retirement

- A career break

- Transitioning between jobs

- Starting a business

During lower-income years, investors may fall into a lower capital gains tax bracket.

In fact, some taxpayers qualify for the 0% long-term capital gains rate, depending on income thresholds. Advisors sometimes recommend realizing gains strategically during those years.

Using Tax-Advantaged Accounts Strategically

Tax-efficient asset placement can significantly reduce capital gains exposure.

Financial advisors often recommend placing investments that generate frequent taxable events—such as actively traded funds—inside tax-advantaged accounts like:

- 401(k) plans

- Traditional IRAs

- Roth IRAs

Meanwhile, long-term, tax-efficient assets may be held in taxable brokerage accounts.

This approach helps minimize annual taxable gains.

Managing Capital Gains in Retirement

Retirement planning introduces new opportunities for capital gains optimization.

Once retirees stop earning a regular paycheck, their taxable income often drops significantly.

Financial advisors sometimes use this period to:

- Realize gains at lower tax rates

- Rebalance portfolios tax-efficiently

- Transition assets into more conservative allocations

For retirees, thoughtful capital gains planning can reduce the tax burden across decades of retirement.

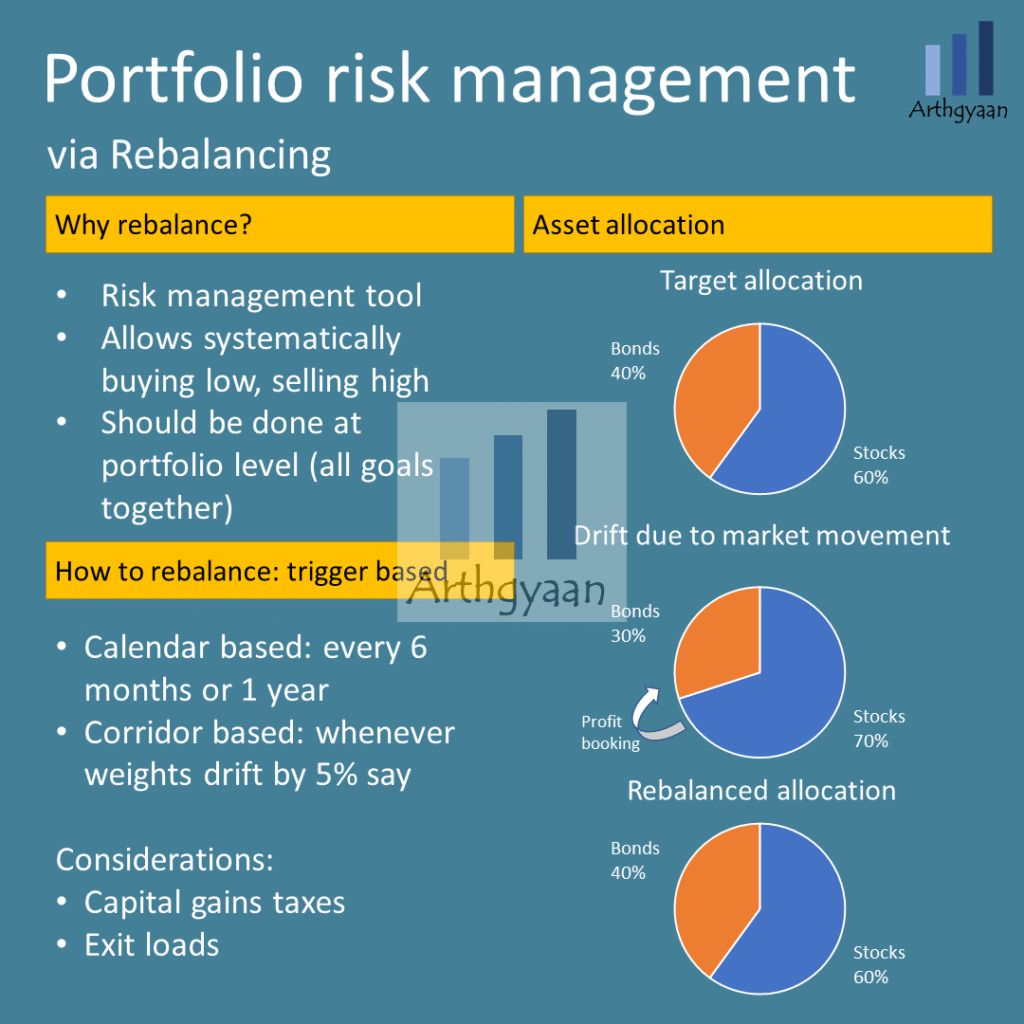

The Role of Portfolio Rebalancing

Rebalancing is essential to maintaining a diversified portfolio, but it can also trigger taxable gains.

Financial advisors frequently balance two priorities:

- Maintaining proper asset allocation

- Minimizing unnecessary tax consequences

Rather than selling large positions all at once, advisors may spread rebalancing transactions across multiple years.

They may also prioritize selling positions with smaller gains first.

How Capital Gains Strategies Fit Into a Broader Financial Plan

Advisors rarely view capital gains optimization in isolation.

Instead, it intersects with other financial planning considerations such as:

- retirement income planning

- estate planning

- charitable giving

- business exit strategies

For example, donating appreciated stock to a qualified charity allows investors to avoid capital gains taxes while receiving a charitable deduction.

Similarly, investors who pass assets to heirs often benefit from the step-up in cost basis, which resets the asset’s taxable value at the time of inheritance.

These broader planning tools often play an important role in long-term tax efficiency.

Common Mistakes Advisors See Investors Make

Financial advisors frequently observe patterns that lead to unnecessary capital gains taxes.

Some of the most common issues include:

- Selling assets impulsively without considering tax consequences

- Ignoring the difference between short- and long-term gains

- Failing to harvest losses during market downturns

- Rebalancing portfolios without tax planning

- Overlooking opportunities in lower-income years

Many advisors encourage investors to review portfolios with tax implications in mind at least once or twice annually, particularly toward the end of the calendar year.

Frequently Asked Questions

What is capital gains optimization?

Capital gains optimization refers to strategies used to manage when investment gains are realized so that taxes are minimized within legal and regulatory guidelines.

What is the current long-term capital gains tax rate?

In the United States, long-term capital gains are typically taxed at 0%, 15%, or 20%, depending on income levels.

How long must you hold an asset to qualify for long-term capital gains?

An investment must be held longer than one year to qualify for long-term capital gains tax rates.

What is tax-loss harvesting?

Tax-loss harvesting is the practice of selling losing investments to offset gains elsewhere in a portfolio, reducing the overall taxable gain.

Can capital losses reduce ordinary income?

Yes. If losses exceed gains, investors can deduct up to $3,000 per year against ordinary income.

Do retirement accounts generate capital gains taxes?

Generally, gains inside tax-advantaged accounts such as 401(k)s and IRAs are not taxed until withdrawals occur.

What is the wash-sale rule?

The IRS wash-sale rule prevents investors from claiming a loss if they repurchase the same or substantially identical investment within 30 days.

Are capital gains taxes different for real estate?

Yes. Real estate may qualify for special rules, including the primary residence exclusion, which can allow individuals to exclude up to $250,000 ($500,000 for married couples) in gains.

When is the best time to review capital gains strategies?

Many advisors recommend reviewing potential gains and losses toward the end of the tax year, though ongoing monitoring throughout the year is beneficial.

Should investors make decisions based solely on taxes?

Most advisors say no. Investment decisions should prioritize long-term financial goals first, with tax efficiency serving as a supporting factor.

The Advisor’s Perspective on Long-Term Tax Efficiency

Financial advisors consistently remind investors that capital gains optimization is less about short-term tactics and more about disciplined long-term planning. Timing, portfolio structure, and tax awareness can collectively preserve a meaningful portion of investment returns.

For many investors, thoughtful coordination between investment decisions and tax planning becomes a quiet but powerful driver of long-term financial outcomes.

Key Insights Investors Often Overlook

- Capital gains taxes depend heavily on holding periods

- Tax-loss harvesting can reduce taxable investment gains

- Lower-income years may offer opportunities for strategic gains

- Portfolio rebalancing should be coordinated with tax planning

- Retirement accounts can reduce exposure to taxable gains

- Long-term planning typically matters more than short-term tactics