Summary

Tax strategy is not a one-time decision—it should adapt as income, assets, family circumstances, and career paths change. From early employment to retirement and estate planning, evolving tax strategies help manage risk, reduce surprises, and align financial decisions with long-term goals while remaining compliant with U.S. tax laws.

Introduction: Tax Strategy Is a Living Process, Not a Static Plan

Many Americans approach taxes as an annual compliance exercise: gather documents, file returns, move on. While filing accurately matters, this mindset often overlooks a more important reality—your tax strategy should change as your financial life changes.

Income grows, careers shift, families expand, investments diversify, and retirement approaches. Each stage introduces new opportunities, constraints, and risks. A tax approach that worked at 25 may be inefficient—or even harmful—at 45 or 65.

Tax strategy isn’t about aggressive maneuvers or loopholes. At its best, it’s a thoughtful framework for aligning financial decisions with the tax rules that apply to your current situation. Understanding when and why strategy should evolve can help reduce unnecessary tax exposure, support long-term planning, and avoid costly missteps.

What Is a Tax Strategy—And Why It’s More Than Filing a Return

Tax filing is backward-looking. Tax strategy is forward-looking.

A sound tax strategy considers how today’s decisions affect future tax outcomes. This includes income timing, investment placement, retirement contributions, business structure, charitable planning, and estate considerations.

In practical terms, tax strategy answers questions such as:

- Should income be accelerated or deferred?

- Which accounts should hold which types of investments?

- How will future tax brackets affect today’s decisions?

- What tax rules apply to upcoming life changes?

Without adjusting strategy as circumstances evolve, people often default to habits that no longer fit their financial reality.

Early Career: Building Habits That Scale With Income

For many Americans in the early stages of their careers, tax strategy is relatively simple. Income may come from a single employer, assets are limited, and deductions are straightforward.

Still, this phase matters more than it seems.

Contributing to tax-advantaged accounts like employer-sponsored retirement plans or Roth IRAs can establish long-term benefits. Early-career tax decisions often focus on:

- Choosing between Roth and traditional retirement contributions

- Understanding marginal tax rates

- Managing student loan interest deductions

- Establishing basic recordkeeping habits

At lower income levels, Roth contributions may be more attractive because current tax rates are modest. As income grows, this calculation often changes.

According to data from the Bureau of Labor Statistics, median earnings tend to rise significantly between ages 25 and 45. That growth alone can push taxpayers into higher marginal brackets, altering the value of deductions versus tax-free growth.

Mid-Career Growth: When Complexity Enters the Picture

As income increases and financial lives become more layered, tax strategy becomes more consequential.

This is often the stage where people encounter:

- Multiple income sources (bonuses, side businesses, equity compensation)

- Homeownership and mortgage-related deductions

- Children and education planning

- Investment portfolios outside retirement accounts

A common mistake during this phase is failing to coordinate financial decisions across accounts. For example, holding tax-inefficient investments in taxable accounts while underutilizing tax-advantaged space can quietly erode after-tax returns.

This is also when proactive tax planning can reduce surprises. Strategic withholding adjustments, estimated tax payments, and income smoothing become increasingly important as variability grows.

Family Changes: How Marriage, Children, and Divorce Affect Tax Planning

Few events alter tax strategy more abruptly than family changes.

Marriage can shift filing status, affect deductions, and change marginal rates. In some cases, combined income pushes couples into higher brackets; in others, disparities create tax efficiencies.

Children introduce credits, dependent care considerations, education savings planning, and long-term estate implications. Decisions about 529 plans, childcare credits, and healthcare accounts often overlap with broader tax strategy.

Divorce introduces its own complexities, including:

- Filing status changes

- Asset division and tax basis issues

- Alimony and support tax treatment

- Retirement account transfers

Failing to revisit tax strategy during these transitions can lead to unintended consequences that persist for years.

Business Ownership and Self-Employment: Strategy Becomes Essential

Once income is no longer limited to a W-2 paycheck, tax strategy moves from optional to essential.

Business owners and self-employed individuals must consider:

- Entity structure (sole proprietorship, LLC, S corporation)

- Payroll versus distributions

- Qualified Business Income (QBI) deductions

- Retirement plan options designed for self-employed individuals

- Cash flow management for tax payments

According to the Internal Revenue Service, small businesses account for the majority of audit adjustments related to underpayment and classification errors—not because of intentional wrongdoing, but because of complexity.

Strategic planning can help balance compliance, cash flow, and long-term sustainability.

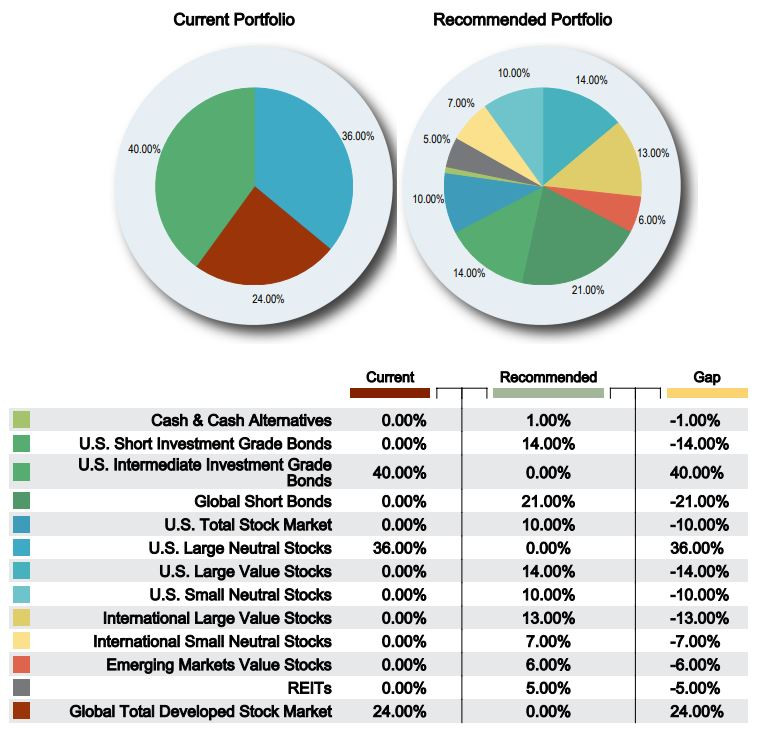

Investing Years: Asset Location Matters as Much as Asset Allocation

As portfolios grow, taxes can quietly become one of the largest drags on returns.

Tax strategy during peak investing years often focuses on asset location—deciding which investments belong in which accounts. Interest-generating assets, actively traded funds, and taxable income producers may be better suited to tax-deferred accounts, while long-term growth assets may belong in taxable accounts where favorable capital gains treatment applies.

Other considerations include:

- Capital gains harvesting

- Loss harvesting during market downturns

- Managing exposure to net investment income tax

- Coordinating charitable giving with appreciated assets

These strategies require coordination and periodic reassessment as markets and personal circumstances evolve.

Pre-Retirement: Planning for the Transition, Not Just the Destination

The years leading up to retirement are often overlooked in tax planning, yet they offer some of the most valuable strategic opportunities.

Income may temporarily decline, creating windows for:

- Roth conversions at lower tax rates

- Strategic realization of capital gains

- Adjusting withdrawal sequencing plans

Decisions made in this phase influence not only retirement income but also Medicare premiums, Social Security taxation, and long-term cash flow.

Without a coordinated approach, retirees may face higher lifetime taxes despite having sufficient assets.

Retirement: Tax Strategy Doesn’t End When Work Stops

Retirement introduces a different tax landscape rather than eliminating taxes altogether.

Income sources may include Social Security, pensions, required minimum distributions (RMDs), investment income, and part-time earnings. Each interacts differently with the tax code.

Key strategic considerations include:

- Withdrawal order from taxable, tax-deferred, and tax-free accounts

- Managing RMD timing and amounts

- Understanding Social Security taxation thresholds

- Coordinating charitable giving through qualified charitable distributions

A static approach during retirement can lead to unnecessary bracket creep and higher healthcare-related costs.

Estate Planning and Legacy Considerations

Later-stage tax strategy often intersects with estate and legacy planning.

While federal estate taxes affect a small percentage of households, income tax consequences for heirs are far more common. Decisions around gifting, beneficiary designations, and asset titling influence not only estate settlement but also ongoing tax efficiency for the next generation.

Strategic planning in this phase emphasizes clarity, coordination, and simplicity—often more valuable than complexity.

Why Static Tax Planning Often Fails

Tax laws change, but more importantly, people change.

A static tax plan assumes consistent income, goals, and risk tolerance. Real life rarely cooperates. Career changes, health events, market cycles, and family needs all require flexibility.

Regular reviews—especially after major life events—help ensure that tax strategy remains aligned with reality rather than outdated assumptions.

Frequently Asked Questions

How often should I review my tax strategy?

At least annually, and anytime a major life or income change occurs.

Is tax strategy only for high-income earners?

No. While complexity increases with income, strategic decisions matter at all levels.

Do tax strategies increase audit risk?

Well-documented, compliant strategies generally reduce risk by improving accuracy and planning.

What’s the difference between tax planning and tax avoidance?

Tax planning uses existing laws responsibly; avoidance often implies aggressive or questionable tactics.

When should I involve a tax professional?

When income becomes variable, assets grow, or life events introduce complexity.

Does retirement simplify taxes?

Often no—income sources diversify, requiring careful coordination.

Are Roth conversions always a good idea?

They depend on current versus future tax rates and cash flow.

How do state taxes affect strategy?

State rules can significantly alter outcomes and should be integrated into planning.

A Financial Life in Motion Requires a Tax Strategy That Moves With It

Tax strategy works best when it evolves alongside the person it serves. Financial lives are dynamic—marked by growth, transitions, and changing priorities. Treating tax planning as an ongoing process rather than a fixed decision allows individuals to respond thoughtfully to new realities while staying grounded in long-term goals.

Key Points to Keep in Perspective as Life Changes

- Tax efficiency depends on timing, structure, and coordination

- Life events often create planning opportunities as well as risks

- Static strategies can quietly undermine long-term outcomes

- Regular reviews help align tax decisions with real-world changes