Summary

Choosing between Roth and Traditional retirement accounts becomes far more important as retirement approaches. Tax timing, required minimum distributions, income shifts, and Medicare implications can significantly affect retirement income. Understanding how each option impacts taxes, withdrawals, and long-term flexibility helps near-retirees avoid costly mistakes and build a more predictable retirement income strategy.

For many Americans in their 20s or 30s, the Roth vs. Traditional retirement account decision often feels abstract. Contributions go into a 401(k) or IRA automatically, and retirement seems decades away. But once retirement moves from a distant concept to a concrete timeline—within 10 to 15 years—the choice between Roth and Traditional accounts becomes far more consequential.

At that stage, taxes, withdrawal rules, and income planning can significantly affect how much money retirees actually get to spend. The same retirement savings balance can produce very different after-tax income depending on whether the funds sit in Roth or Traditional accounts.

According to the Employee Benefit Research Institute, tax considerations become one of the most important financial planning factors for households within a decade of retirement. Understanding the Roth vs. Traditional trade-offs can help retirees manage taxes, preserve Social Security benefits, and reduce required withdrawals that could push them into higher tax brackets.

Understanding the Core Difference

The fundamental difference between Roth and Traditional accounts lies in when taxes are paid.

Traditional retirement accounts provide a tax deduction upfront but require taxes on withdrawals later. Roth accounts reverse that arrangement: contributions are made with after-tax dollars, but qualified withdrawals are tax-free.

While this seems simple, the long-term implications are complex—especially for individuals approaching retirement.

Traditional accounts:

- Contributions are typically tax-deductible

- Investments grow tax-deferred

- Withdrawals in retirement are taxed as ordinary income

- Required minimum distributions (RMDs) start at age 73

Roth accounts:

- Contributions are made with after-tax dollars

- Growth is tax-free if rules are met

- Withdrawals in retirement are tax-free

- No required minimum distributions for Roth IRAs

When retirement is decades away, the difference may feel theoretical. As retirement gets closer, however, these rules begin to shape real financial decisions.

Why Taxes Become a Bigger Issue Near Retirement

During peak working years, many Americans focus primarily on maximizing contributions. But as retirement approaches, attention often shifts toward managing taxes during withdrawals.

Income sources in retirement may include:

- Social Security benefits

- Traditional IRA or 401(k) withdrawals

- Pension income

- Investment income from taxable accounts

Traditional retirement withdrawals are treated as ordinary income, which can affect tax brackets and even trigger taxes on Social Security benefits.

The Social Security Administration notes that up to 85% of Social Security benefits may become taxable depending on total income. Large withdrawals from Traditional accounts can push retirees over those thresholds.

Roth withdrawals, by contrast, generally do not count toward taxable income calculations. This can provide retirees with greater flexibility when managing yearly income.

Required Minimum Distributions Change the Equation

One of the most overlooked reasons the Roth vs. Traditional debate becomes critical near retirement involves required minimum distributions (RMDs).

Traditional retirement accounts require mandatory withdrawals starting at age 73. These withdrawals are taxable and based on life expectancy tables.

For retirees with large balances, RMDs can create unexpected tax burdens.

Example:

Imagine a retiree with $1.2 million in a Traditional IRA. At age 73, the required minimum distribution may exceed $45,000 annually, depending on IRS life expectancy tables.

That withdrawal:

- Is fully taxable

- Could increase Medicare premiums

- May push the retiree into a higher tax bracket

Roth IRAs, however, do not require minimum distributions during the original owner’s lifetime. This makes them valuable for long-term tax planning.

Income Flexibility Becomes More Valuable

One of the biggest advantages of Roth accounts near retirement is income control.

Retirees can mix withdrawals from taxable, tax-deferred, and tax-free accounts to manage their yearly tax situation.

For example:

A couple retiring at age 65 might aim to keep taxable income below a certain threshold to minimize taxes or avoid higher Medicare premiums.

If all retirement savings are in Traditional accounts, every withdrawal increases taxable income.

But if a portion of savings is in Roth accounts, retirees can draw tax-free income when needed.

This flexibility can help with:

- Avoiding higher tax brackets

- Managing capital gains taxes

- Controlling Medicare income thresholds

- Preserving Social Security benefits

Roth Conversions Become a Strategic Tool

As retirement approaches, many households explore Roth conversions—moving money from Traditional accounts into Roth accounts.

This process involves paying taxes today in exchange for tax-free withdrawals later.

The strategy can be especially useful during lower-income years, such as the gap between retirement and when Social Security begins.

Example:

A worker retires at 62 but delays Social Security until age 70.

Between ages 62 and 70, taxable income may be relatively low. This period can create an opportunity to convert portions of a Traditional IRA to a Roth while staying within a manageable tax bracket.

Financial planners often refer to this as a “tax bracket management” strategy.

Medicare Premiums Are Affected by Income

Another factor that becomes important closer to retirement is Medicare’s income-related monthly adjustment amount (IRMAA).

Medicare premiums increase when retirees’ modified adjusted gross income exceeds certain thresholds.

Traditional withdrawals increase income for IRMAA calculations, while Roth withdrawals generally do not.

In 2025, IRMAA thresholds begin around $103,000 for individuals and $206,000 for married couples (adjusted annually).

Large Traditional withdrawals or RMDs can push retirees into higher premium tiers.

Strategic Roth usage can help retirees stay below these thresholds.

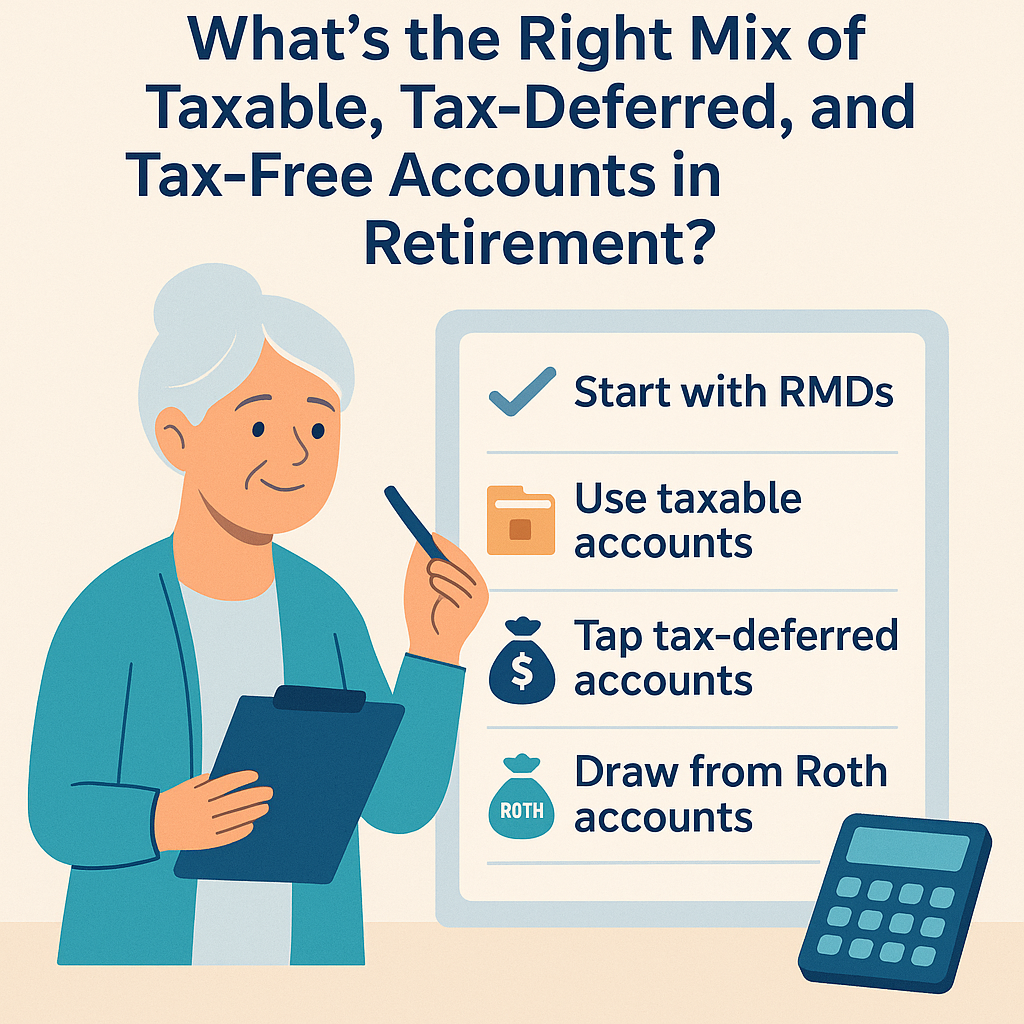

Tax Diversification Matters More Late in the Game

Just as investment diversification reduces risk, tax diversification can improve retirement income stability.

Having assets spread across multiple tax categories gives retirees more options.

Common categories include:

- Taxable brokerage accounts

- Traditional tax-deferred accounts

- Roth tax-free accounts

Many financial planners suggest maintaining a mix of these account types by the time retirement arrives.

This allows retirees to adjust withdrawals depending on market conditions and tax policies.

For example:

During years with high medical expenses, retirees might prefer Roth withdrawals to avoid increasing taxable income.

Legacy Planning Considerations

Another reason Roth accounts become more attractive near retirement involves estate planning.

Heirs who inherit Traditional retirement accounts must pay taxes on withdrawals.

Heirs who inherit Roth IRAs can typically withdraw funds tax-free (though distribution rules still apply).

Under the SECURE Act, most non-spouse heirs must withdraw inherited retirement accounts within 10 years.

If the account is Traditional, those withdrawals can create a significant tax burden.

Roth accounts may allow heirs to withdraw funds without triggering income taxes.

When Traditional Accounts Still Make Sense

Despite the advantages of Roth accounts in retirement planning, Traditional accounts remain valuable.

They can be especially useful for individuals currently in high tax brackets who expect lower income during retirement.

Situations where Traditional contributions may still be beneficial include:

- High-income earners seeking tax deductions today

- Workers expecting lower retirement income

- Individuals with significant Roth balances already

- Those planning strategic conversions later

The decision rarely involves choosing one account type exclusively. Most retirement strategies benefit from both.

Frequently Asked Questions

1. Is Roth always better than Traditional near retirement?

Not necessarily. Roth accounts provide tax-free withdrawals and no RMDs, but Traditional accounts may still be advantageous if current tax rates are higher than expected retirement rates.

2. What is the biggest advantage of Roth accounts in retirement?

The primary benefit is tax-free withdrawals, which provide flexibility when managing taxable income and avoiding higher tax brackets.

3. Can retirees convert Traditional IRAs to Roth?

Yes. This process is called a Roth conversion, and taxes must be paid on the converted amount.

4. What age is best for Roth conversions?

Many financial planners recommend considering conversions during lower-income years, often between retirement and the start of Social Security benefits.

5. Do Roth IRAs have required minimum distributions?

No. Roth IRAs do not require minimum withdrawals during the original account holder’s lifetime.

6. How do Roth withdrawals affect Social Security taxes?

Qualified Roth withdrawals generally do not count as taxable income, which may help reduce Social Security taxation.

7. Do Roth withdrawals affect Medicare premiums?

No. Roth withdrawals typically do not count toward income thresholds used to calculate Medicare IRMAA surcharges.

8. Can someone contribute to both Roth and Traditional accounts?

Yes. Many workers split contributions between both account types to create tax diversification.

9. Should retirees move everything into Roth accounts?

Usually not. A balanced mix of account types often provides the most flexibility for long-term tax planning.

10. How late is too late for Roth conversions?

Conversions can happen at almost any age, though large conversions later in retirement may create high tax bills.

The Retirement Window Where Tax Strategy Matters Most

The years just before and after retirement represent one of the most important tax-planning windows in a lifetime. Decisions made during this period can influence decades of retirement income.

Understanding the differences between Roth and Traditional accounts allows retirees to manage taxes, control income, and preserve financial flexibility.

Rather than viewing the Roth vs. Traditional debate as a simple choice, many near-retirees benefit from a strategy that uses both account types thoughtfully.

The closer retirement gets, the more these decisions move from theory to reality.

Key Planning Insights to Remember

- Roth withdrawals provide tax-free retirement income

- Traditional withdrawals increase taxable income

- Required minimum distributions can raise tax burdens

- Roth conversions may help manage future taxes

- Tax diversification improves retirement flexibility

- Medicare premiums depend on taxable income levels