Housing experts overwhelmingly believe a full-blown U.S. housing market crash in 2025 is unlikely. What’s more probable is a soft landing: modest home price declines or plateauing, slowing sales, and persistent affordability challenges due to elevated mortgage rates. Evidence shows the market is cooling — not collapsing.

Americans are asking one big question in 2025: “Is the U.S. housing market headed for a crash?”

For many, the word “crash” brings up memories of the 2008 housing crisis — a time of plunging prices, mass foreclosures, and severe financial pain. But is history about to repeat itself? Or are we in a fundamentally different situation today?

The short answer: while the housing market is undeniably cooling, the majority of experts agree that a 2008-style collapse is highly unlikely. Instead, what we’re more likely to see is a period of stabilization, modest corrections in certain regions, and ongoing affordability struggles.

This long-form article will walk you through everything you need to know about the U.S. housing market in 2025:

- How today’s conditions compare with 2008

- The latest economic indicators and forecasts

- Regional differences across the country

- Why a crash is unlikely, but corrections are possible

- What it all means for buyers, sellers, and investors

- Practical takeaways and expert-backed advice

- 10+ FAQs addressing the most pressing questions Americans have right now

Let’s dive in.

What Does a “Crash” Really Mean & Why 2025 Is Different

Before we examine forecasts, it’s critical to clarify what people mean by a housing market crash. Generally, a crash implies:

- National home prices fall 20% or more within a year or two

- Widespread foreclosures that push down values further

- Severe wealth destruction affecting homeowners, investors, and financial institutions

That was the story in 2008. But today’s situation has key differences.

| Feature | 2008 Crash (Great Recession) | 2025 Context |

|---|---|---|

| Origin | Loose lending, subprime mortgages, speculation-driven bubble | Stricter lending standards, robust homeowner equity |

| Mortgage Rates | Many adjustable loans reset, triggering defaults | High but stable (6–7%), discouraging speculation |

| Inventory Levels | Oversupply, overbuilding in many metros | Rising in some states, but still constrained overall |

| Foreclosure Risk | Very high due to risky loans and little equity | Currently low; most owners have strong equity |

Put simply, the 2025 market isn’t built on the same shaky foundation. While affordability is stretched and some areas are overheated, conditions are not aligned with a systemic collapse.

Key Economic Indicators Shaping the 2025 Market

The housing market doesn’t exist in isolation — it’s driven by broader economic forces. Let’s explore the numbers shaping 2025.

1. Mortgage Rates

- NAR (National Association of Realtors) forecasts average 30-year fixed mortgage rates around 6% in 2025.

- This is high compared to the pre-pandemic era (3–4%) but lower than late 2023 when rates briefly touched 8%.

- High rates suppress demand but also prevent reckless borrowing.

Takeaway: Rates will likely keep demand subdued but not collapse the market.

2. Home Price Trends

- Zillow projects a 1.7% decline between March 2025 and March 2026.

- National home values currently average $363,505, up only 0.2% year-over-year — essentially flat.

- Some regions are seeing slight declines already, while others remain stable.

Takeaway: Expect flat growth or mild declines, not a freefall.

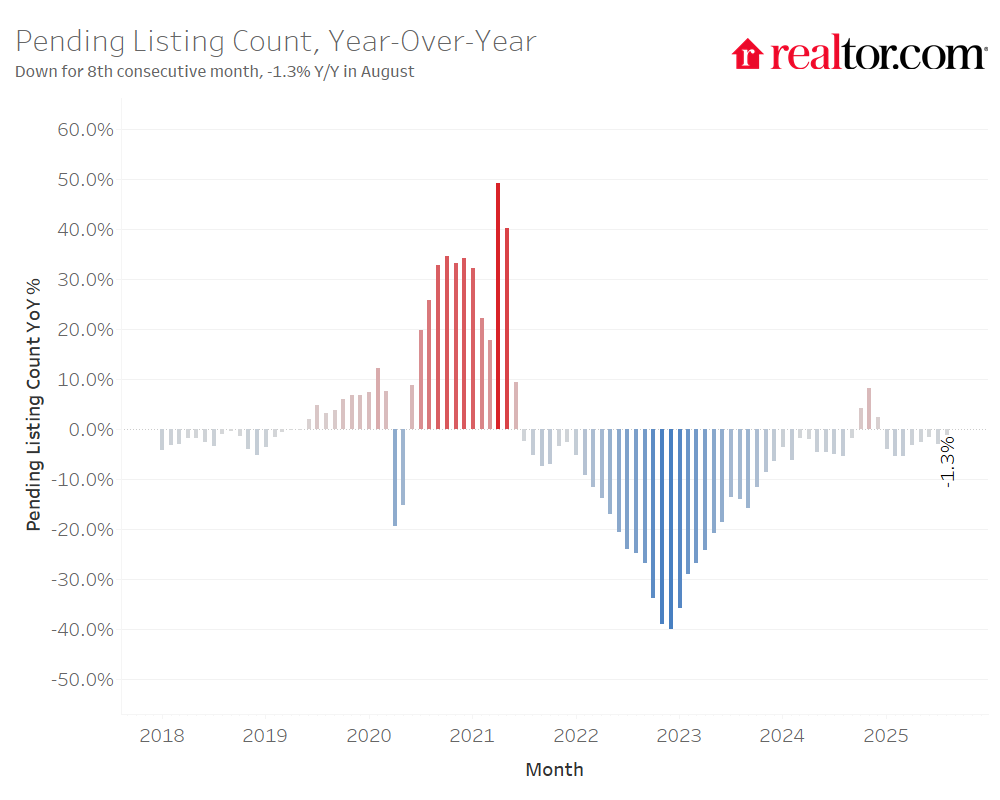

3. Supply & Inventory

- Existing home sales in 2024 hit the lowest levels since the 1990s.

- Inventory has risen in markets like Texas and Florida, giving buyers more leverage.

- However, in many regions, supply remains below long-term averages.

Takeaway: More balance is returning, but there’s no nationwide glut.

4. Affordability & Demand

- High home prices and mortgage rates mean monthly payments are unaffordable for many households.

- Wage growth has helped somewhat, but not enough to offset costs.

- Many potential buyers are choosing to wait or rent instead of purchasing.

Takeaway: Affordability remains the biggest challenge for the housing market.

5. Expert Forecasts

- JP Morgan: ~3% price growth at most in 2025.

- Zillow: 1.7% decline nationally.

- Multiple forecasting agencies: 1.5–2% growth on average.

- Some metros could see 5–10% declines, but these are localized.

Takeaway: Most forecasts agree on flat to slightly negative growth.

Regions Most at Risk in 2025

Not all markets are equal. While a nationwide crash seems unlikely, some regions could face sharper corrections.

- Florida & Texas: Pandemic-era boom states now face oversupply and affordability issues.

- Louisiana: Zillow projects 5–10% declines in some metros.

- Luxury markets: High-priced homes are more sensitive to interest rates.

- Single-industry towns: Local economic downturns could trigger price drops.

In contrast, areas with strong job markets, population growth, and limited supply (e.g., parts of the Midwest) are expected to remain resilient.

Why a Full-Blown Crash Is Unlikely

Here’s why most experts dismiss a 2008-style collapse in 2025:

- High homeowner equity: Millions of Americans owe far less than their homes are worth.

- Stricter lending standards: Borrowers today have stronger credit profiles.

- Low foreclosure rates: Defaults remain historically low.

- Regulation & oversight: Post-2008 reforms protect against risky practices.

- Moderate supply: Unlike 2007, we don’t have rampant overbuilding.

In short: the fundamentals are stronger today than during the last crash.

Possible Scenarios for 2025

| Scenario | Description | Likely Impacts |

|---|---|---|

| Soft slowdown | Prices flat or slightly negative | Buyers gain leverage, sellers adjust expectations |

| Localized corrections | Some metros see 5–10% drops | Regional disparities grow wider |

| Stagflation effect | High inflation, slow growth, high rates | Buying delayed, renters squeezed |

| Recession trigger | Job losses or external shock | Larger declines, but not guaranteed |

FAQs About the 2025 Housing Market

Here are real questions Americans are asking — answered with data and examples.

Q1: Will home prices fall in 2025?

Most experts say prices will either flatten or fall slightly (0–2%). Local declines of 5–10% are possible in overheated markets.

Q2: Is a 2008-style crash coming?

Highly unlikely. Unlike 2008, today’s market is not built on subprime lending or speculation.

Q3: How do mortgage rates impact crash risk?

High rates reduce affordability but also limit risky lending. If rates drop too quickly, demand could spike — preventing a crash.

Q4: Are foreclosures about to surge?

No. Foreclosures remain low because most owners have equity and fixed-rate loans.

Q5: Which regions are most at risk?

Florida, Texas, and Louisiana are flagged as more vulnerable. The Midwest is considered safer.

Q6: How big a problem is affordability?

It’s the biggest constraint. Even with stable prices, many households cannot afford current mortgage payments.

Q7: Could new home construction cause oversupply?

In some local markets, yes. But nationally, the U.S. is still underbuilt, especially for affordable housing.

Q8: Could the Federal Reserve trigger a crash?

Only if they tighten policy aggressively. Current signals suggest a cautious approach.

Q9: Should buyers wait to purchase?

If you can afford comfortably, it may be worth buying. Waiting for a crash could mean waiting indefinitely.

Q10: Is 2025 a bad time to sell?

Not necessarily — but sellers should expect longer times on market and lower offers.

Q11: What are the best data sources to watch?

- NAR reports

- Zillow’s Home Value Index

- FHFA Price Index

- HUD housing starts data

Practical Advice & Takeaways

- For Buyers: Don’t overstretch financially. Focus on fundamentals like job market strength and location.

- For Sellers: Be realistic. The days of bidding wars are largely gone.

- For Investors: Look for undervalued regions with strong growth potential.

- For Homeowners: Don’t panic — equity is still high, and nationwide crash risks are low.

Conclusion

All signs point to this: the U.S. housing market in 2025 is cooling, not crashing.

While affordability challenges, high rates, and regional declines will persist, the systemic risks of 2008 are absent. Homeowners with equity are protected, lenders remain cautious, and supply is moderate.

Expect flat prices, regional corrections, and affordability struggles rather than a dramatic collapse.

For anyone involved in real estate — buyers, sellers, or investors — the key is to stay informed, focus on local fundamentals, and manage expectations.